Download

1 / 28

280 likes | 527 Vues

The Employer Mandate and its Penalties. Hays Companies Spring, 2019. Disclaimer.

E N D

The Employer Mandate and its Penalties Hays Companies Spring, 2019

Disclaimer • This presentation is provided for general information purposes only and should not be considered legal or tax advice or legal or tax opinion on any specific facts or circumstances. Readers and participants are urged to consult their legal counsel and tax advisor concerning any legal or tax questions that may arise. Any tax advice contained in this communication (including any attachments) is not intended to be used, and cannot be used, for purposes of (i) avoiding penalties imposed under the U. S. Internal Revenue Code or (ii) promoting, marketing or recommending to another person any tax-related matter.

Employer Mandate Basics

Employer Mandate What is an ALE? • Applicable Large Employer (ALE) • 50 or more full-time and full-time equivalent employees (FTEs) • Based on the previous year’s average • All employees of a “controlled group” of entities are taken into account • Each control group member must then comply with the mandate on its own

Employer Mandate Which employees do we care about? • For purposes of the employer mandate, if the employee is the employer’s common-law employee, the employee must be analyzed for compliance with the employer mandate • Difficult types of employees to determine common-law status: • Temporary employees hired from a staffing agency • Union Employees • Employees that work for multiple, related entities

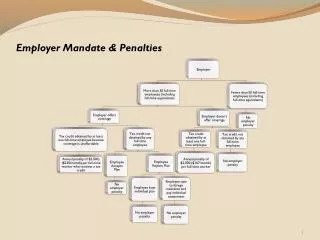

Employer Mandate What are the penalties? • Subsection (a) penalty 2018: $2,320 • $199.33 per month per full-time employee • This is the penalty if coverage is not offered to substantially all (95%) full-time employees and one full-time employee not offered coverage goes to the exchange and gets a subsidy • Subsection (b) penalty 2018: $3,480 • This is the penalty if the coverage is not affordable (9.56% in 2018, 9.86% in 2019), does not constitute MV, or a full-time employee is not offered coverage but the employer meets the 95% requirement • $290 per month per full-time employee

Employer Mandate A couple affordability notes: • The affordability safe harbor can be changed from year to year • W-2, rate-of-pay, and FPL • Rate-of-pay is most common because of its predictability • (Hourly rate) x 9.56% x 130 • Use of a safe harbor is not required • Not using a safe harbor doesn’t automatically result in a penalty • Wellness rewards impact affordability (except tobacco)

Employer Mandate How are penalties avoided? • If there are enough non full-time employees, measure non full-time employees in a look-back measurement period to determine full-time status • Use of the look-back method is not required (despite what the payroll vendor states) • If coverage is already offered to enough full-time employees to mitigate exposure to penalties to an acceptable level, continue business as usual

Employer Mandate What hours count towards full-time status? • An hour of service is credited each hour for which an employee is paid, or entitled to payment, for the performance of duties for the employer; and each hour for which an employee is paid, or entitled to payment, by the employer for a period of time during which no duties are performed due to vacation, holiday, illness, incapacity (including disability), layoff, jury duty, military duty, or leave of absence

Employer Mandate What’s a full-time employee? • A full-time employee is an employee who, based on the facts and circumstances surrounding the employee’s position and expected work schedule, is expected to work 130 hours per month (30 hours/week) during their employment • This is true even if the employee is only expected to work for a short period of time (with the possible exception of seasonal employees) • All other employees are measureable for full-time designation

Employer Mandate What’s a seasonal employee? • A seasonal employee is an employee who is hired into a position for which the customary annual employment is six months or less and their employment occurs at about the same time each year • Measurable even if they’re expected to work 130 hours or more during their period of employment • Interns usually fall within this bucket, but measuring just because of interns doesn’t always make sense • Likely to be under age 26

Employer Mandate What is the look-back method? • Measurement period: • A prior period to determine whether or not employees have met the hours of service thresholds of 130 hours per month (30 hours per week) • Initial measurement period for new variable hour employees • Standard measurement period for ongoing employees • Administrative period: • The period immediately after the measurement period and before the stability period (up to 90 calendar days) • Stability period • The period for which the employee’s status is set with regard to eligibility

Employer Mandate Two different measurement periods for new hires and ongoing employees? • Standard measurement period for ongoing employees • An ongoing employee is an employee who has been employed for at least one standard measurement period • Initial measurement period for new employees • This includes employees that have not had an hour of service for 13 weeks or more

2 months 12 months 12 months Measurement Period Admin. Period Stability Period 11/1/2019 – 12/31/2019 1/1/2020 - 12/31/2020 11/1/2018 - 10/31/2019 Standard Method for Ongoing Variable Hour Employees Common Structure for Calendar Year Plans The measurement period is 12 months long The administrative period is 2 months long The stability period follows the measurement/administrative period and matches the measurement period at 12 months long

Hired mid August Initial Measurement Period (6/01/19 - 5/31/20) Stability Period (7/1/20 - 6/30/21) Standard Measurement Period (11/1/19 - 10/31/20) Stability Period (1/1/21 - 12/31/21) Standard Measurement Period (11/1/20 - 10/31/21) 1/1/20… Overlap begins • New Variable Hour Employees • Initial measurement period (IMP) of 12 months starts 1st of the month following date of hire • Measure new employee’s hours of service during the IMP • Employee averages at least 130 hours of service per month during the measurement period • Offer coverage for the following stability period • Employee does not average at least 130 hours of service per month during the measurement period • Not required to offer coverage for the following stability period • However, employee may qualify for coverage during the ensuing on-going measurement period

Employer Mandate What about unpaid leaves while measuring? • Unpaid FMLA, USERRA and Jury Duty • Exclude special unpaid leave for determining hours of service (remove this period from the numerator and the denominator) • Or, treat the employee as credited with hours of service for any periods of special unpaid leave at a rate equal to the average weekly rate at which the employee was credited with hours of service during the weeks in the measurement period that are not part of a period of special unpaid leave (averaging method)

Employer Mandate What happens when an employee changes from a full-time position to a non full-time position? • The employer can use the 3-month rule, or • The employer can place the employee into the current stability period and give the employee the choice to drop their coverage because of a significant reduction in hours • If the change occurs within the time period of what would have been the initial measurement period, terminate coverage at the time of change and measure through the end of the initial measurement period

Employer Mandate What happens when an employee changes from a non full-time position to a full-time position? • Technically, under the Employer Mandate, the employer could hold the employee off of the plan until the completion of the next full measurement period • No one does this • ERISA plan document language will almost always require the employee to be offered coverage as a full-time employee (with or without a waiting period

Employer Mandate Penalties Two examples: • Example 1: Manager hires a “temporary” employee and doesn’t communicate the nature of the position to the home office. Employee was correctly reported as a full-time employee by their reporting system and triggered a penalty. • Example 2: Employer has a small part-time population they don’t offer coverage to, but it was their intent to mitigate their exposure to penalty taxes by using a look-back measurement period. One part-time employee triggered penalties for part of the year because they had an uptick in hours. Their reporting system reported the individual as full-time for those months and not in a limited non-assessment period. The employer did not have measurement language in their SPD and their system was unable to demonstrate that the employee was being tracked to determine eligibility. They are still waiting for the IRS’ determination on their position that the employee was in a limited non-assessment period, but there’s no guarantee that the penalty is waived.

Employer Mandate Penalties Watch out for acquisitions: • Example 1: Stock purchase of an Applicable Large Employer (ALE) by an ALE. They wanted the “new” employees to go through a waiting period. This would have opened the door to significant Subsection (a) penalty exposure. • Example 2: Asset purchase of an ALE almost finished when the question was asked about Employer Mandate exposure. Not only was coverage not offered for the past four years, reporting was not completed either. • Penalty is $250 for each return to which a failure relates, capped at $3,000,000 per calendar year.

Employer Mandate Penalties

226J Penalty Letter IRS began sending out penalty notices at the end of 2017 for the 2015 calendar year • Notice is called a 226J Letter • Followed by a 220J letter if the IRS does not receive a response or does not agree with the employer’s response to the 226J letter • Penalties are based, in part, on the information provided by the employer in their annual 1094-C and 1095-C reporting • 2016 notices are still being sent out

226J Penalty Letter The notice includes background information about the Employer Mandate and: • A Form 14765, which is an employee list listing by month, the employer’s assessable full-time employees and the indicator codes, if any, reported on lines 14 and 16 of each assessable full-time employee’s Form 1095-C; • A description of the actions the employer should take if it agrees or disagrees with the proposed employer shared responsibility payment; • A description of the actions the IRS will take if the ALE does not provide a timely response; and • A Form 14764, “ESRP Response”, which is the approved response form to Letter 226J

226J Penalty Letter Two most common mistakes leading to 226J letter: • Not indicating that MEC was offered for all 12 months • Reporting on individuals that were not reportable full-time employees • A full year of 1H on line 14, without a safe harbor code on line 16

226J Penalty Letter • What to do if you receive a 226J letter and you want to dispute the penalties: • Talk to your attorney • Review the ESRP Summary Table and Form 14765 to understand how the penalty was triggered • Gather all necessary information and documentation to back up your response • Draft a letter of explanation to go with your Form 14764 response (not required) • Make sure you respond on time (response due date on first page of 226J letter)

226J Penalty Letter • Things to keep in mind when responding to a 226J Letter: • Make sure you can support your work • It’s possible the individual that triggered a Subsection (a) penalty wouldn’t trigger a Subsection (b) penalty • Corrections on Form 14765 allow you to attach additional information • This is where active waivers are useful • If you missed someone, it’s possible that you will have to pay the penalty (or at least a portion) • Don’t wait, act now! You have 30 days to respond

Another Penalty A quick Letter 5699 mention… • If you receive one of these, it means the IRS thinks you either did not file your 1094C/1095Cs, or that you did so either late or incorrectly • Like all filing penalties, you get a chance to respond • Good faith standard applied to 2015 filings