Download

1 / 47

470 likes | 749 Vues

Presented by:- CA. Gopal S. Malpani NVM & Associates ‘Ramkunj’, Railway Station Road, New Osmanpura, Aurangabad -431005 E-mail :- gsmalpani@rediffmail.com Phone:- 0240-2326106 Mobile No:- 09823012346. CHANGES IN VAT AUDIT FORM 704. CA Gopal S. Malpani.

E N D

Presented by:-CA. Gopal S. MalpaniNVM & Associates‘Ramkunj’, Railway Station Road,New Osmanpura,Aurangabad -431005E-mail :-gsmalpani@rediffmail.comPhone:- 0240-2326106Mobile No:- 09823012346

CHANGES IN VAT AUDIT FORM 704 CA Gopal S. Malpani

The new version of E-704 is put on website on 2.11.2010.it is upgraded from 1.2.0.to 1.2.1. However, this new form/amendments are not notified as required under Rule 17A of MVAT Rules, 2005. CA Gopal S. Malpani

1) Instruction - Following new instructions have been added- Instructions Nos. 19, 24, 25 and 39 have been added. CA Gopal S. Malpani

(2) Introduction to Changes (A) Additions In Form 704 • Letter Of Submission • Annexure G • Annexure J-5 • Annexure J-6 CA Gopal S. Malpani

(B) Modification In Form 704 • In Part I • In Part II • In Schedules I To V • Annexure A To D • In Annexure E • In Annexure F • In Annexure J-1,J-2,J-3 And J-4 • No Modification In Schedule Vi And Annx. K • Tin & Period Will Display Automatically On All The Parts Of Audit Report. CA Gopal S. Malpani

(3) Gist Of Important Changes (3.1) Letter of Submission is added CA Gopal S. Malpani

Mainly Dealer’s Acceptance/Dissenting views with reasons have been asked in respect of specified 8 Categories. • It is to be filed physically only and it doesn’t get uploaded • Impact -1) If accepted by dealer – then in case of payment, dealer should make the payment. • If not accepted than he has to give the reason and depending upon the facts and circumstances of the case, further action may be taken by Department. • Auditor responsibility in respect of such letter. CA Gopal S. Malpani

(3.2) PART – I a) The version has been upgraded and now 1.2.1 is provided in place of 1.2.0.Version. b) This part is modified and following charges are made: Location of the Sales Tax office of place of business of the dealer has to mention. 42 locations are given. CA Gopal S. Malpani

PART -1 Point 2(A): TABLE-1 Sr. No.4 point “Verification of the Returns for the period under Audit From To “has been eliminated. The point was there in old form. Sr. No.5(a)(i): Returns verified under MVAT Act, 2002 – One more option of ‘Not Filed’ are added. Sr. No.5(a)(i):Returns verified under MVAT Act, 2002 – Only two options were there ‘All’ and ‘Available’. Sr. No.5(a)(ii) & 5(b): Options are – ‘Available’, ‘Not Applicable’, ‘Not Filed’. That is ‘Not Filed’ is added/ Change. Sr. No.5(a)(i): Returns verified under MVAT Act, 2002 – Only two options were there ‘All’, ‘Available’ and ‘Not Applicable’ CA Gopal S. Malpani

PART -1 Point 2(B) 1. Sr. Nos.2(B)(a)&(b)(Row Nos.37 to 44) • Schedule and Annexure as applicable to be ticked, • To Read it in totally and not in isolation CA Gopal S. Malpani

PART -1 Point 3: • Not only reasons for Negative Certificates, but also any additional information to be read along with Certificates is to be given. • Only the reasons for Negative Certificates are to be mention. CA Gopal S. Malpani

PART -1: TABLE-2: • Row No. 95 has been inserted.- Excess credit carried forward to next tax period. No. change is made in Table 3 i.e. it is pertaining to CST. To see implications. CA Gopal S. Malpani

PART -1: TABLE-3: • Sr. No. (v) (b) Amount of tax paid under CST Act including interest and RAO. RAO is newly added. • Sr. No. (v) (b) Amount of tax paid under CST Act including interest. CA Gopal S. Malpani

PART -1: TABLE-5: • Heading of table has been changed. • Effect of change on refund to be seen. CA Gopal S. Malpani

Additional details regarding Registration number of Auditor’s firm has to be given.(Prop. as well as Partnership Firm) • Some Issues • Periodicity of Returns • Filling of TDS Return in 405 CA Gopal S. Malpani

At the end of PART – 1, Signature (Handwritten) of Chartered Accountant / Cost Accountant is to be given. At the end of PART – 1,Registration No. of Auditing Firm is to be given PART – 1: Mobile Nos. of the Auditors CA Gopal S. Malpani

(3.3) Part 2 • Renumbering and Realignment • Land line Number of the dealer is also asked now. • Activity Code: Minimum five digits activity code is to be written instead of four digits. CA Gopal S. Malpani

3.4 Schedule I to V • More Rows are added for providing Tax Rates wise break up • Rows is provided for adjustment of VAT Refund to next Tax period. CA Gopal S. Malpani

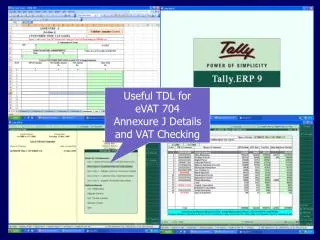

3.5 Annexure A to J • All Annexure are modified and following changes are made- • Annexure have to be filled in in descending order (value wise). However it is now stated that in respect of some • Annexure the Descending order may be removed. • In case of Annexure J-1 to J-4, if incorrect TIN No. is entered in any of these annexure then these annexure disclose the incorrect TIN in Red immediately. To see how to mitigate difficulty in case TIN is correct but not responded as correct on website. CA Gopal S. Malpani

CA Gopal S. Malpani a) Annexure A & B

Annexure are modified and following changes are made. • Column pertaining to date of filling of return is removed • Interest on late payment of tax will be calculated automatically. • Take care of entering Due date, in case last day is bank holiday. CA Gopal S. Malpani

b) Annexure E CA Gopal S. Malpani

Annexure is modified and fillowing changes are made • Section 1-Quantity has to be provided in case of petroleum products in liters. Actually it is applicable for Motor Spirit and not for Petroleum product. • Section 2-Description of Rule 54(a) to (k) has been provided • Section 3-Description of Rule 53 has been provided (Sub clause wise set off calculation has to be submitted) • Section 6-Amount of Total Set-off Available to the dealer has to be calculated as under: CA Gopal S. Malpani

Gross input Tax Less: Set Off (ITC) Not Admissible Less: Reduction in Setoff (ITC) = Balance available Setoff (ITC). Auditor should put some amount may be 0,against no setoff available in Rule 54 CA Gopal S. Malpani

c) Annexure F CA Gopal S. Malpani

Annexure is modified and following modifications have been made- • New Ratio is Added – Out of Maharashtra Purchases which are capitalized – it is only information asked for ? To find out logic behind this requirement, if any • One Column – Column of “Method of computation & Observations, if any” is deleted. To see impact. • One Ratio is Changed – Ratio of interstate stock transfer to Net Local Sales has been asked in place of ratio of Net local sales to inter – state stock transfer. CA Gopal S. Malpani

4) New Information have been asked for- CA Gopal S. Malpani

In all, 15 types of new information have been asked for- • In respect of opening and closing stock (Sr. Nos. 1 to 10) • Gross amount of sale of Fixed Assets (Sr. No.11) • Gross Receipts as defined in MVAT Rule 53(6) (Sr. No.12) • Turnover of sales as per Profit & loss (Sr. No.13) • Turnover of Purchases as per Profit & Loss (Sr. No.14) • Total of Non sales income. (Sr. No.15) CA Gopal S. Malpani

Some Issues • Meaning of Non Sales income (Ratio no.3) • Meaning of Non Sales Receipt/Non Sale income, • Meaning of Gross Receipts, Gross Turnover of sales. (Gross Receipt as per Rule 53(6) and other wise. • Turnover of sales and purchases as per P/L A/c. (What treatment to be given to excise amount, tax amount, scrap sales amount etc.) e) What treatment to be given to income received on account of interest, Subsidy, branch transfer etc. ? CA Gopal S. Malpani

d) Annexure G: this annexure is newly inserted in modified forms This annexure is asking details of declaration forms or certificates received. Details about form under CST Act like Form C,F,H, etc. to be mentioned. Total 999 rows are provided. Details of forms are to be mentioned in descending order (value wise) CA Gopal S. Malpani

Issues: • What is the impact of differential amount between gross sales amount and amount for which declaration has been received? • Gross amount as per Invoice- Which are the components to be included e.g. CST, freight charges, installation etc. whether to be included? Impact of Goods Return. if intention to reconciliation with Schedule VI then it is very tedious job. To find out the exact value of sales invoices less goods return and ultimately to reconcile with GTO of sales in Schedule VI will be time consuming. CA Gopal S. Malpani

e) Annexure J (1) CA Gopal S. Malpani

Customer Wise VAT Sales Details-Annexure is modified and following new rows are added. • Row No. 1000 replaced with “Remaining local transaction total where tax is collected separately not covered above” • Row No. 1001 added for “Local Sales to non TIN holders” • Row No. 1002 is added for “Gross local sales where tax is not collected”. • Terms “Net Taxable amount”, “Gross Amount” & Other Local Taxable Sales” have been deleted. • Issues • Gross sales vis-à-vis Gross sales and net taxable sales. • About various types of sales made by various dealers e.g. PSI Sales, Composition Dealers’ sales, Impact of Rule 57(1) etc. CA Gopal S. Malpani

f) Annexure J(2) CA Gopal S. Malpani

Supplier wise VAT purchasesAnnexure is modified and following new rows are added. • Row No. 1000 replaced with “Remaining local transaction total where tax is paid separately not covered above” • Row No. 1001 added for “Local Purchases from non TIN holders” • Row No. 1002 added for “Gross local Purchases where tax is not paid separately” • Note is provided and defining the terms “Net taxable amount” and “Gross amount” CA Gopal S. Malpani

g) Annexure J(3) Customer wise Debit Note or Credit Note CA Gopal S. Malpani

Annexure is modified and following new rows are added. • Row No. 500 replaced with “Remaining local transaction total of Debit/credit Notes where tax is collected separately (not covered above)” • Row No.501 inserted for “Debit/Credit Note in case of local sale to Non TIN holders” • Row No. 502 inserted for “Gross local sales of Debit/Credit where tax is not collected separately” • To be careful on this point (502). Tax element should be shown separately. CA Gopal S. Malpani

h) Annexure J(4) Supplier wise Debit Notes or Credit Notes CA Gopal S. Malpani

Annexure is modified and following new rows are added. • Row No. 500 replaced with “remaining local transactions total of Debit/ Credit Notes where tax is collected saparately by supplier (not covered Above)” • Row No. 501 inserted for “Debit/ Credit Note in case of local purchases to Non TIN holders” • Row No. 502 inserted for “Gross local purchase of Debit/ Credit notes where tax is not collected separately” CA Gopal S. Malpani

i) Annexure J(5) Customer wise transactions of Direct Export and High Seas Sales under CST Act, 1956. CA Gopal S. Malpani

This Annexure has been newly inserted and following details are asked- • Customer Name • TIN of Customer (if any) • Transaction type, Export or High Seas Sales • Gross Total • Major Commodity CA Gopal S. Malpani

j) Annexure J(6): Supplier wise Transactions under CST Act 1956. CA Gopal S. Malpani

This Annexure has been newly inserted and following details are asked- • Customer Name • TIN of Customer (if any) • Transaction type, OMS purchase, Direct import, High Seas purchases, Purchase U/s.6(2) & Branch transfer • Any other cost of purchase. • Gross Total CA Gopal S. Malpani

k) Validation buttons • In all parts, Schedules & Annexure ‘Press for Validation’ key is kept at the bottom rather than at top. CA Gopal S. Malpani

4. Conclusion: The department has improved the form by: Removing some of the ambiguities in the audit report • Drafting a good looking format (as compared to earlier format) • Asking specific information what they expect in audit report • Collecting details in Annexure J which will help us in case of refunds or so called speedy refunds. However, it has created certain ambiguities mainly in reporting of sales/purchases and ratio. We hope that in future version of the form will be confusion free. CA Gopal S. Malpani