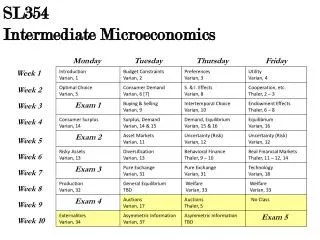

Intermediate Microeconomics

Intermediate Microeconomics. Monopoly. Pure Monopoly. A Monopolized market has only a single seller. Examples? XM radio? Microsoft? Walmart in a small town?. Monopolies. So what causes monopolies? Legal Constraints: e.g patents for new drugs Ownership of a fixed resource

Intermediate Microeconomics

E N D

Presentation Transcript

Intermediate Microeconomics Monopoly

Pure Monopoly • A Monopolized market has only a single seller. • Examples? • XM radio? • Microsoft? • Walmart in a small town?

Monopolies • So what causes monopolies? • Legal Constraints: • e.g patents for new drugs • Ownership of a fixed resource • e.g. toll highway, land in a given area. • Collusion • e.g. several producers act as one (OPEC) • Large economies of scale (natural monopolies) • e.g. land line phone service, utilities, Google? Microsoft?

Monopolies • Why are we concerned about Monopolies?

Implications of Monopoly • Key to Monopoly: Seller is not a price taker! • Specifically, since monopolist chooses market supply, it essentially picks a point on the market demand curve to operate on. • This means that for a monopolist, equilibrium price is a function of the quantity they supply, so they effectively get to choose both • i.e. choose where to operate on p(q) (“Inverse Demand Curve”) $ QD(p) or p(q) Q

Monopolist’s Problem • In perfect competition, a firm wanted to choose a quantity to maximize profits, given it is a “price taker”. max π(q) = R(q) – C(q) = pq – C(q) • To find profit maximizing q, we take derivative of π(q) and set it equal to zero, • This gives p - MC(q*) = 0 “First Order Condition” (FOC) • or equivalently, keep producing until MC(q*) = p • Like any firm, a monopolist wants to choose quantity to maximize profits, but by doing so effectively chooses price as well. max π(q) = R(q) – C(q) = p(q)q – C(q) So what will be profit maximization condition for the monopolist?

Monopolist’s Problem $ c(Q) R(Q) = p(Q)Q q π(Q)

Marginal Revenue for Monopolist • Profit max condition is always MR(q*) = MC(q*) (from FOC) • For firm in perfect competition, firm is a price taker so MR(q) = p for all q. • For monopolist: MR(q*) = [p’(q*)q* + p(q*)] • Since p(q) is the inverse of the market demand curve, we know p’(q) < 0. • Therefore, [p’(q)q + p(q)] < p(q), implying MR(q) < p(q) (i.e. marginal revenue from producing and selling another unit is less than price) • What is intuition? • Ex: Consider a Market Demand Curve: QD(p) = 400 – 5p • What is Equation for the Inverse Demand curve? • What is Equation for Marginal Revenue curve? • Graphically?

Monopolist Behavior • Consider a monopolist: • Cost function given by C(q) = q2 + 8q + 20 • Market Demand Curve of QD(p) = 400 – 5p. • What will be equilibrium price and quantity? • Graphically?

Profit Maximization and Demand Elasticity • Recall that R(q) = p(q)q • So MR(q) = p’(q) q + p(q) = p(q)[p’(q) q/p(q) + 1] • Recall ε(p) = Q’(p) p/Q(p) = slope of demand curve times price divided by quantity • So 1/ε = slope of inverse demand curve times quantity divided by price = p’(q) q/p(q) • So MR(q) = p(q)[1/ε + 1] • Recalling ε < 0, what does this tell us about output under a monopoly and demand elasticity, recognizing that Monopolist will choose q to equate MR(q) to MC(q)?

Profit Maximization and Demand Elasticity • We can actually learn even more from elasticity. • In competitive markets, firms produced until p = MC(q*) • Alternatively, monopolist supplies until MR(q*) = MC(q*), or until: p(q*)[1/ε + 1] = MC(q*) • Re-writing we get: p(q*) = MC(q*)ε /[ε +1] • So how does monopoly “mark-up” depend on elasticity of demand?

Monopoly and Efficiency • The key implication of a Pareto Efficient outcome is that all possible gains from trade are exhausted. • Will this be true in a monopolized market? • Consider first what it means for all gains from trade to be exhausted. • Output is produced as long as marginal cost of last unit is less than what a consumer is willing to pay for that unit. • How do we know this won’t be true under a profit maximizing monopolist? How would we see this graphically?

Taxing a Monopolist • What if government imposes a tax on monopolist equal to $t/unit sold. Will this somehow increase efficiency? • Consider again monopolist with MC(q) = 2Q + 8 that faces a demand curve such that MR(Q) = 80 – 2Q/5 • We know that without tax, Q = 30 and p = 74 • What will change with tax of t = $12? • Graphically?

Entry • If a monopolist is making all these economic profits, can this monopoly be maintained? • Entry constrained by law (patents, patronage/political favors) • Natural Monopoly - firm’s technology has economies-of-scale large enough for it to supply the whole market at a lower average cost than is possible with more than one firm in the market. • Essentially very high fixed costs of entry. • Examples?

Monopoly Policy • Under natural monopoly it is best for one firm to supply whole market. • To prevent inefficiencies of monopoly, there are a couple of strategies. • Have government run/regulate industry. • e.g. Utilities, postal service? • Break-up monopolist • Especially relevant when declining marginal cost structure due to high entry costs (e.g. software, drugs) • Block mergers that could allow monopolies to form in the first place. • Problems?