Understanding International Monetary Exchange

740 likes | 854 Vues

Explore the complexities of international monetary exchange in the global economy, including the basics of money, monetary systems, and implications for policymakers. Delve into the historical evolution of money and its various functions in trade and finance.

Understanding International Monetary Exchange

E N D

Presentation Transcript

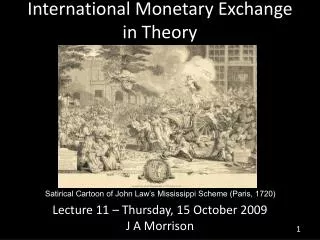

International Monetary Exchange in Theory Lecture 11 – Tuesday, 12 October 2010J A Morrison Satirical Cartoon of John Law’s Mississippi Scheme (Paris, 1720)

PS 0304 Int’l Pol Econ ✔ • Unit 1: Studying the Global Economy • Topic 1: Introductory • Topic 2: Perspectives on IPE • Topic 3: Explaining Foreign Economic Policy • Unit 2: Trading Goods & Services • Topic 4: Trade in Theory • Topic 5: Trade in Practice • Unit 3: The International Monetary System • Topic 6: The IMS in Theory • Topic 7: The IMS in Practice • Unit 4: Migration • Unit 5: Special Topics in IPE ✔

Lec 11: Money in Theory • Introductory: Money is Hard • The Basics of Monetary Exchange • The International Connection • Exchange Rate Politics

Lec 11: Money in Theory • Introductory: Money is Hard • The Basics of Monetary Exchange • The International Connection • Exchange Rate Politics

Before we launch into the specifics of international monetary exchange, let’s step back to consider international monetary exchange in the context of international trade.How does money compare to trade?

Simply put, money is hard…Money is hard for us—the academicians—to understand.And it is hard for policymakers to control.

Money is Hard for Us • Less familiar than trade • More abstract than trade & migration • Money has changed more over time • Variation in policies: fixed versus flexible • akin to change in trade policy: liberal versus managed • But money itself might be different: commodity currency is governed by different rules than is fiat currency

Money is Hard for Policymakers • More difficult to understand • Imprecise, blunt instruments • Money is more mobile more difficult to control • Severe market constraints: attacks, competition, counterfeiting, contagion, &c.

So, the international monetary system is more difficult for policymakers to manage than is trade.But, arguably, the stakes are higher…

Money Matters • The downside risk is greater • Collapse of trade: ouch! • Currency collapse catastrophic! • All interests are affected • Some groups rely relatively little on trade • Everyone uses money tighter coupling with macroeconomic effects • Damage is harder to repair • Violating a trade agreement causes upset • States spend decades trying to repair reputations after currency disorders

Here’s our plan…We’ll proceed as we did for trade: first theory, then empirics. Be prepared that money will be challenging. I’ll do my best to unpack the key terms and concepts. But you might have to turn things up a notch.

Lec 11: Money in Theory • Introductory: Money is Hard • The Basics of Monetary Exchange • The International Connection • Exchange Rate Politics

II. BASICS OF MONETARY EXCHANGE • Background on Money • Monetary Systems

It’s easy to understand why we trade goods & services: the benefits of specialization are readily apparent.Understanding the invention and use of money, however, is less immediately obvious.

(1) Medium of Exchange • Money resolves “double coincidence of wants problem” • What are the chances that you’ll encounter someone who has what you want and wants what you have? • Hint: < Finding True Love

Money evolves as a means to resolve this problem. Individuals accept a common good with certain characteristics (high value to bulk ratio, divisible, durable, uniform in quality) that becomes the common medium of exchange.

(2) Store of Value • Money allows individuals to convert perishables into more durable goods • This allows: • Storing value between transactions • Saving by hoarding cash

(3) Unit of Account • Money provides a standard relationship between various g&s in the economy • Using a standard unit simplifies accounting and transactions immensely

II. BASICS OF MONETARY EXCHANGE • Background on Money • Monetary Systems

Across history, nations have chosen a wide variety of materials to serve as money. The ancient Greeks used cattle, some Native Americans used wampum, and the early Chinese used cowry shells.Today, most countries use “paper” currency, which is usually made from cotton and/or linen.

For most of history, in most places, markets came to rely on specie--minted, precious metal coins.

We can organize monetary systems according to the various values of the money…

The Values of Money • Intrinsic Value: market value of the currency’s constituent material when used for non-monetary purposes • E.g. gold coin sold as material for jewelry • Exchange Value: market value of the currency when used as currency in trade • E.g. gold coin used to purchase jewelry • Extrinsic/Nominal Value: “official” value and/or units • E.g. “1 shilling,” “1 dollar”

Monetary systems can be grouped along a continuum according to the gap between the intrinsic and the exchange values of the currency.

Seigniorage • Historical Origin: charge at mint to convert raw material into currency • Also called “brassage” or “coinage” • Modern Usage: “the excess of the nominal value of a currency over its cost of production” (Cohen, Future of Money, 18) • Implications: • Revenue source for state • Creates incentive to counterfeit—(the unauthorized creation of currency)

Seigniorage and Monetary Systems • Commodity Money • High seigniorage might be viewed as revenue source (e.g. 18th C France) • Low or no seigniorage would subsidize exports and encourage capital inflows (e.g. 18th C Britain) • Fiat Money • Seigniorage is necessarily high; seigniorage creates the difference of value between intrinsic and exchange values

The historical trend is clearly away from commodity money and toward fiat money. Policymakers generally prefer fiat money because (1) they gain increased revenue from seigniorage; and (2) the market imposes fewer constraints on monetary policy when using fiat money.But the power to “print” money is frequently abused. Some economists, like FA Hayek, appreciated the discipline imposed by commodity money systems.

Lec 11: Money in Theory • Introductory: Money is Hard • The Basics of Monetary Exchange • The International Connection • Exchange Rate Politics

III. THE INTERNATIONAL CONNECTION • The Nth Currency • Exchange Rate Regimes • The Balance of Payments

The same logic that impels the development of a common medium of exchange within economies impels the adoption of international media of exchange between economies.Such a currency is sometimes called the Nth Currency.

Gold & silver previously performed this role. After WWII, the US dollar was the preeminent Nth Currency. Today, the dollar faces competition from the Euro, the Yen, and the Renminbi.

“The United States would be mistaken to take for granted the dollar’s place as the world’s predominant reserve currency…Looking forward, there will increasingly be other options to the dollar.”-- World Bank President Robert B. Zoellick (26 Sept 2009)(Source: NYT 28 Sept 2009)

Why would foreign states move away from holding the dollar in reserve and using the dollar in international exchanges?

Because the dollar doesn’t perform the functions of money as well as it used to!

The Dollar’s Declining Role • Medium of Exchange • US share of total GATT/WTO Member GDP • 1948: ~65% • 2001: ~38% (Source: Barton, et al, p 13) • Store of Value • Market price of gold (per ounce) in $US • 1945: $35/ounce • 14 Oct 2009: $1063/ounce • 11 Oct 2010: $1348/ounce

III. THE INTERNATIONAL CONNECTION • The Nth Currency • Exchange Rate Regimes • The Balance of Payments

How do states determine their relationships to the Nth Currency, whatever it might be?

An exchange rate (ER) is the specific valuation between domestic currency and a foreign/international currency/commodity.

A state’s exchange rate regimeis the set of rules that determine the relationship (including valuation) between domestic currency and foreign currencies, the Nth currency, and/or key commodities.

(For now, we assume governments enjoy monetary sovereignty, the ability to control the market value of their currencies.)

How States Regulate the Value of the Currency • Intervention in Foreign Exchange (Forex) Market • Buy/sell reserves of domestic currency, foreign currency, and/or a key commodity to directly affect market prices • Adjust Quantity via Monetary Policy • Open Market Operations • Fractional Reserve Rate • Discount Rate (Interest Rate) • By Proclamation and/or Price Controls • “What was previously worth $1 shall now be worth $5.” • “Grain shall not be sold for less than $5 per bushel.” • “One Pound shall not be traded for more or less than $4.86.”

States can regulate the value of the currency vis-à-vis: • Foreign currency(ies) • Key commodity(ies) • The overall national price level Is it possible to fix a currency with respect to several things simultaneously?

Not usually.Different parts of the economy grow at different rates. Maintaining stability with respect to one precludes stability with respect to the others.

Pick a Price, Any Single Price • Assume Different Rates of Growth • World supply of gold: 2% • US GDP: 3% • British GDP: 1% • What should be rate of increase of US dollars? • Stable gold price: 2% • Stable overall price level: 3% • Stable ER vis-à-vis pound: 1% Stability can only be maintained along one dimension at a time

Exchange rate regimes exist along a continuum: to what extent does the state use its monetary sovereignty to maintain a stable exchange rate in the market?