Download

1 / 48

590 likes | 1.03k Vues

Commutation of Pension and conditions for payment of Family Pension. Session Overview. A Central Government employee is permitted to commute a portion of his pension and receive a lump sum amount in lieu of surrender a portion of the pension. . Session Overview.

E N D

Commutation of Pension and conditions for payment of Family Pension RTI Jammu

Session Overview • A Central Government employee is permitted to commute a portion of his pension and receive a lump sum amount in lieu of surrender a portion of the pension. RTI Jammu

Session Overview • Besides, in the event of death of a Government Servant while in service or the death of a Central Government pensioner, his/her family is entitled to Family Pension. RTI Jammu

Session Overview • During this session we will discuss the procedure for commutation of pension and also discuss the conditions for payment of Family Pension and the amount of Family Pension admissible to Central Government employees or pensioners who die while in service or after retirement. RTI Jammu

Learning Objective • At the end of the session the trainees will be able to state the procedure for commutation of pension and also work out the family pension admissible to the family of a Central Government employee or pensioner who dies while in service or after retirement. RTI Jammu

Commutation of Pension • A new set of rules titled "Central Civil Services (Commutation of Pension) Rules, 1981" to regulate the commutation of Civil pensions granted under the provisions of the 'CCS (Pension) Rules, 1972', was notified with effect from Ist July, 1981. These rules provide for a portion of a Government servant's pension (and not family pension) being commuted for a lump sum payment. RTI Jammu

Commutation of Pension • In other words, a Government pensioner can surrender a portion of his monthly pension and in lieu get a lump sum payment. RTI Jammu

Commutation of Pension • A Government servant is entitled to commute for a lump sum payment a faction not exceeding 40% of his pension. Fraction of a rupee will be ignored for the purpose of commutation. (Rule 5) RTI Jammu

Commutation of Pension • A Government servant or the pensioner against whom departmental or judicial proceedings referred to in Rule 9 of CCS (Pension) Rules, 1972, are pending shall not be eligible to commute a fraction of his pension during the tendency of such proceedings. (Rule 4) RTI Jammu

Commutation of Pension • A Government servant or the pensioner against whom departmental or judicial proceedings referred to in Rule 9 of CCS (Pension) Rules, 1972, are pending shall not be eligible to commute a fraction of his pension during the tendency of such proceedings. (Rule 4) RTI Jammu

Commutation of Pension • The application for commutation should be made to Head of office in the prescribed form after the date of retirement. However, if the retirement is on superannuation, he may submit the application before the date of superannuation. (Rules 13 and 19). RTI Jammu

Commutation of Pension • The application should make a nomination in the prescribed form, along with his application for commutation, conferring on one or more persons the right to receive the commuted value of pension in case he dies without receiving the commuted value on or after the date on which the commutation became absolute. RTI Jammu

Commutation of Pension • Commutation without Medical Certificate: • (a) a superannuation pension under Rule 35. • (b) a retiring pension under Rule 36 • (c) a pension on absorption in or under a corporation or company or body in terms of Rule 37. • (d) a compensation pension on abolition of permanent pos under Rule 39 • (e) a pension in whole or in part on the finalization of the departmental or judicial proceedings referred to in Rule 9 and issue of final orders thereon. (Rule 12) RTI Jammu

Commutation of Pension • Commutation with Medical Certificate: • (a) Those who retire on invalid pension under Rule 38. • (b) Those who are compulsorily retired from service as penalty and granted pension under Rule 40. • (c) Those who are in receipt of Compassionate Allowance under Rule 41. • (d) The category of pensioner's referred to in Item (5) above, if they apply for commutation after one year from the date of their retirement. (Rule 18) RTI Jammu

Commutation of Pension • The amount of commuted value of pension as finally calculated should be rounded off to the next higher rupee. (GID (1), below Rule 8, Appx.1) RTI Jammu

Reduction in pension on account of commutation • The reduction in the amount of pension on account of commutation will be operative from the date of receipt of the commuted value of pension or at the end of three months after issue of authority by the Accounts Officer for payment of commuted value of pension, whichever is earlier. In the case of retirement on superannuation and the commuted value of pension becomes payable on the day following the date of retirement, the reduction will be operative from the inception of pension.(Rule 6) RTI Jammu

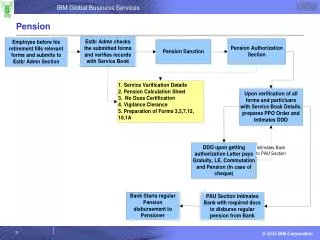

Procedure for Commutation of Pension • Cases where medical examination is not necessary: • The Government servant after retirement should submit his application for commutation in Form 1 to the Head of Office where he served last before retirement. The Head of Office should initial the application indicating the date of its receipt and process the same and forward it to the Accounts Officer who will issue payment authority after necessary checks. RTI Jammu

Procedure for Commutation of Pension • Cases requiring Medical Examinations: The Government servant or pensioner desiring to commute a fraction of his pension shall submit an application in the prescribed Form 2 to the Head of Office under whom he is serving. • (ii) The Head of Office on receipt of the application shall acknowledge it immediately and forward the application to the Accounts Officer for completing Part-IV of the application and retransmission to him. • The Accounts Officer after completing Part-IV of the application shall return the application to the Head of Office. • On receipt back, the Head of Office shall address the concerned Chief Medical Authority in Form 3 and forward to him (a) Form 2 with Part-IV duly completed in original; (b) two copies of the applicant's photograph of which one shall be an attested copy; (c)a copy of Form 4 with a spare copy of Part-II of that Form; and (d) report or statement or the applicant's case if he has been granted invalid pension. RTI Jammu

Procedure for Commutation of Pension • He shall also endorse a copy of the letter addressed to the Chief Medical Authority to the applicant and the Accounts Officer. • The Chief Medical Authority shall arrange for the medical examination of the applicant by the appropriate Medical Authority and also give intimation to the applicant to appear for the Medical Examination. • The Medical Authority after examination of the applicant shall, without delay, forward to the Accounts Officer his medical report. • The Accounts Officer, on receipt of the Medical Report shall, without delay, issue an order to the Pension Disbursing Authority concerned for the payment of the commuted value of the pension. RTI Jammu

Calculation of commuted value of pension • The lump sum payable to an applicant shall be calculated in accordance with the table of the values applicable to him on the date on which the commutation becomes absolute. The amount of commuted value should be rounded off to the next higher rupee. RTI Jammu

Commutation of provisional pension • A Government servant to whom, pending assessment of final pension, provisional pension has been sanctioned under Rule 64 of CCS (Pension) Rules, shall be eligible to commute a fraction of such provisional pension. RTI Jammu

Retrospective revision of final pension • An applicant who has commuted a fraction of his final pension and after commutation his pension has been revised and enhanced retrospectively as a result of Government's decision, the applicant shall be paid the difference between the commuted value determined with reference to the enhanced pension and the commuted value already authorized. RTI Jammu

Restoration of commuted portion of pension after 15 years • Commuted portion of pension shall be restored after completion of fifteen years from the date of retirement if the commutation is simultaneous with retirement. In other cases, the commuted portion of pension will be restored after fifteen years from the date of commutation. RTI Jammu

Death of the pensioner before receiving the commuted value • If a pensioner dies without receiving the commuted value on or after the date on which commutation became absolute, the commuted value shall be paid to his nominee(s). If there is no such nomination, the commuted value will be paid to the family members, it shall be paid to his 'heirs'. RTI Jammu

Commutation value to be entered in both halves of PPO • The date on which the payment of the commuted value of pension was made to the applicant or the commuted value was credited to the applicant's account shall be entered in both halves of the Pension Payment Order by the Disbursing Authority under intimation to the Accounts Officer who authorized the payment of commuted value of pension. RTI Jammu

Calculation of Dearness Relief payable to pensioners • Dearness Relief admissible to pensioners will be calculated on the original amount of pension even after commutation of a portion of the pension. RTI Jammu

Commutation amount not taxable under IT Act • Lump sum amount received on commutation of pension is not liable to be taxed under Income Tax Act. RTI Jammu

Family Pension • The 'Family Pension' 1964, Scheme gives a life pension to the widow/widower of the Government Servant. • The benefit of this scheme has been extended from 22.09.1977 also to Government Servant on pensionable establishments who retired/died before 31.12.1963 as also to those who were alive on 31.12.1963 but had opted out of this scheme; vide Rule 54 (1) RTI Jammu

To whom admissible • The family pension is admissible to the family of a deceased Government Servant, where he dies: • (a) after completion if not less than one year's continuous service or before completion of one year of continuous service if the deceased Government Servant immediately prior to his appointment was medically examined and declared fir for Government service; RTI Jammu

To whom admissible • after retirement from service and was in receipt of pension on the date of death. A Government Servant who retires from service before completing 10 years 'qualifying service is not entitled for the payment of pension; but is entitled to only Service Gratuity. If such a person dies after retirement his family will not be eligible for the grant of Family Pension, 1964. RTI Jammu

To whom admissible • Family Pension is not admissible to a person who is already in receipt of family pension or is eligible thereof under any other rules of the Central Government or a State Government and/or Public sector Undertaking/ Autonomous Body/Local Fund under the Central or State Government. However, such person may opt to receive RTI Jammu

Rate of Family Pension • In the case of Government Servant who retire from service or die while in service on or after 1st January, 1996, Family Pension, 1964, shall be calculated at a uniform rate of 30% of basic pay in all cases subject to a minimum of Rs 1,275 p.m and a maximum of Rs 9,000p.m. RTI Jammu

Higher scale of family pension • Where a Government Servant, who is not governed by the Workmen's Compensation Act 1923 dies while in service after having rendered not less than seven years continuous service the family pension payable to the family of the deceased Government Servant shall be equal to 50% of the pay last drawn by the Government Servant or twice the family pension admissible at normal rated, whichever is less RTI Jammu

Higher scale of family pension • This higher rate of family pension is payable from the date following the date of death of the Government Servant for a period of seven years or for the period up to date on which the deceased Government Servant would have attained the age of 65 years had he survived, whichever is earlier. RTI Jammu

Higher scale of family pension • Where a Government Servant who is governed by the workmen's Compensation Act, 1923, dies while in service after having rendered not less than seven years' continuous service, the family pension payable is equal to admissible at the normal rates, whichever is less and is payable from the date following the date of death of the Government Servant for a period of 7 years or up to the date on which he would have attained the age of 65 years if he had survived, whichever is earlier. RTI Jammu

Higher scale of family pension • After the expiry of the aforesaid initial period, the family pension payable shall be at the normal rates. RTI Jammu

Doubling and rounding off of family pension • The amount of family pension shall be fixed at monthly rates and be expressed in whole rupees, any fraction of a rupee being rounded off to the next higher rupee. In respect of family pension payable at higher rate under, the rounding off has to be done at the final stage, i.e., after doubling the family pension. RTI Jammu

Rounding off when divisible to more than one beneficiary • Where family pension is divisible to more than one beneficiary, the fraction of a rupee, if any, in each share should be rounded off to the next higher rupee; but the total of all the shares should not exceed the maximum amount of family pension, i.e., Rs 9,000 p.m in the case of enhanced rate of family pension. RTI Jammu

Definition of 'pay' for family pension • 'Pay' for this purpose means the emoluments as specified in Rule 33, i.e, the pay as defined in Rule 9(21) (a) (i) of the Fundamental Rules, non-practising allowance and stag nation increment, if any, which the person was drawing on the date of his death while in service or immediately before retirement. RTI Jammu

Retirement Gratuity • 1/4th of 'emoluments' for each completed six-monthly period of qualifying service, service, subject to maximum of 16 1/2 times the 'emoluments' and further subject to a maximum of Rs 3.5 lakhs. RTI Jammu

To whom family pension payable • The family pension is payable to the family of the deceased Government servant/ pensioner.' Family ' means- • (i) Wife (whether the marriage took place before or after retirement) in the case of male Government servant. • (ii) Husband (whether the marriage took place before or after retirement) in the case of female Government servant. • (iii) Unmarried son(s)/unmarried daughter(s) (born before or after retirement) who have not attained the age of 25 years. RTI Jammu

To whom family pension payable • (iv) Widowed daughters/Divorced daughters (born before or after retirement) without any age restriction. • Parents who were wholly dependent on the Government servant when he/she was alive, provided that the deceased Government servant had left behind neither a widow/widower nor an eligible son or daughter or a widowed/ divorced daughter and that the earnings of the parents is not more than Rs.2,550 per month. RTI Jammu

Period for which family pension is payable • (i) In the case of a widow or widower, up-to-date of death or re-marriage, whichever is earlier; • (ii) In the case of an unmarried son/unmarried daughter, until he/she attains the age of 25 years or up to date of his/her marriage or till the date from which he/she starts earning a sum of Rs 2,550 or more per month from employment in Government, private sector, self employment, etc., whichever is the earliest. RTI Jammu

Period for which family pension is payable • (iii) In the case of widowed (including widowed disabled)/divorced daughter(s) up to date of her re-marriage or till she starts earning a sum of Rs 2,550 or more per month from employment, etc., or death, whichever is the earliest. Such daughter shall not be required to come back to her parental home. • (iv) In the case of wholly dependent parent(s), till his/her death. RTI Jammu

Period for which family pension is payable • The family pension is payable to only one member of the family at a time except in cases where it is payable to more than one widow or where it is payable or twin children. • It is first payable to the widow/widower till the date of her/his death or remarriage, whichever is earlier and thereafter to the eligible children. • The eligible male/female children of deceased Government Servants/pensioners will be entitled to family pension in the order of their birth irrespective of their sex and the younger of them will not be eligible unless the elder above him/her becomes ineligible. • Wholly dependent parents will become eligible for family pension if the deceased Government Servant had left neither a widow/widower nor an eligible son or daughter or a widowed/divorced daughter and that the earning of the parents is not more than Rs 2,550 per month. RTI Jammu

Also payable to children from the void or voidable marriage • In view of the fact that section 16 of the Hindu Marriage Act, 1995, as amended by Hindu Marriage Laws Act states" Notwithstanding that a marriage is null and void under Section 11, any child of such marriage who would have been legitimate if the marriage had been valid, shall be legitimate, Family Pension will be payable to such children. RTI Jammu

Regulation of family pension in the case of twin children • In the case of eligible twin children, the family pension should be paid in equal shares. When one child ceases to be eligible, his/her share shall revert to the other child and when both of them child/twin children. RTI Jammu

Admissible to handicapped children even beyond the prescribed age-limit • If the son or daughter of a Government Servant is suffering from any disorder or disability of mind or is physically crippled or disable so ad to render him or her unable to earn a living even after attaining the prescribed age, family pension is payable for life subject to the following conditions. RTI Jammu