Download

1 / 3

30 likes | 36 Vues

You can request the lender terminate your PMI as soon as you have that quantity of equity built up. The lending institution will look at your finance condition and payment history as part of the approval procedure when you request PMI cancellation. Your background can't show a 30-day or a lot more late repayment in the in 2014 or a 60-day or more late payment in the last 2 years.

E N D

They are managed as well as should pass examinations on even more subjects than brokers, though the expenses can vary relying on whether you pay costs or commission. You may not have what's called 'mortgage insurance' but your home mortgage might currently be covered must the worst occur. This is due to the fact that you might currently havelevel term life insurance.This pays a round figure if you pass away within an established term, eg, ₤ 300,000 if you pass away within 20 years. This money could not just to go in the direction of your dependants and also their living costs yet it can ALSO be utilized to settle your home loan. The 2nd includes either a house equity line of credit or a basic home equity finance. The second car loan covers the remaining total up to obtain the 20% deposit and generally has a greater price. Some individuals suggest that home mortgage life insurance assists the lending institution greater than your family members since the bank gets the cash if you pass away, not your recipients. While the payout can eliminate the economic stress and anxiety of paying a home mortgage, your household can still be entrusted to costs and other financial obligation they can't pay for. Yet the most effective alternative for preventing PMI without putting 20 percent down is to take out a government-backed funding that does not need it! Both VA and also USDA Rural Advancement car loans are readily available with little to no down payments without calling for PMI or various other recurring insurance coverage settlements. Another opportunity is to have the loan provider pay the mortgage insurance. Consider including some insurance. This insurance policy safeguards the lender in case the purchaser defaults on the car loan. When trying to safeguard a mortgage, it is always prudent to specifically ask if PMI will be needed, in addition to the complete expense of this insurance policy for your finance before you make a financing dedication. Anyone that has a home loan or is about to get a home finance needs to comprehend PMI, additionally called exclusive mortgage insurance, as well as how it's funded in a financing. It's equally essential to know what is consisted of in your escrow account, since escrow needs enhance your regular monthly home loan. repayments. Fully comprehending both topics will allow you to confirm you're only paying what's called for by the terms of your funding and also nothing even more. That is a good thing for you because it allows financial institutions to make car loans they otherwise may not have made. And also they have the ability to make them at lower rates than they would have supplied without mortgage insurance. With a piggyback mortgage, customers can utilize 2 finances instead of one (piggyback) to acquire a home. Store for a refi home mortgage today on Bankrate.com if refinancing will allow you drop PMI. You might come under this risky group if you have missed out on mortgage settlements, so make sure your settlements depend on date prior to asking your lending institution to drop mortgage insurance. Lenders might need a higher equity percentage if the residential or commercial property has been transformed to rental use. Conversely, you can talk to an independent financial adviser (IFA). IFAs cover life insurance, among other items, and might be able to see where it harmonizes your other protection and larger cash concerns. If you would certainly prefer face-to-face recommendations (most brokers have a tendency to be phone based), it's also a great idea. Finances made through the Veterans Management can be had without deposit as well as deal eye-catching prices for experts, impaired or active service participants. VA lendings do not call for mortgage insurance in itself, yet they do call for an instead substantial funding cost. This charge normally must be paid upfront but can be rolled into the funding as well as be made as component of the month-to-month settlement. Specific debtors are exempt from this fee, based upon their situations. The VA declares that this charge helps defray several of the costs associated with this program.

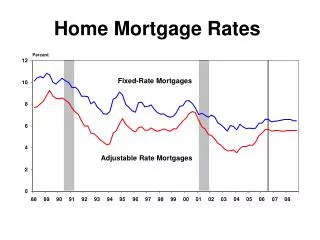

In a so-called "no-PMI loan," the lending institution really pays the PMI in return for billing a greater rate of interest on the home loan itself. This sometimes, but not constantly, can be less expensive than paying the PMI yourself. When a buyer adds much less than 20 percent to the down settlement on a home lending, private mortgage insurance is needed. Abandoning and also switching over might obtain you the same cover for a fraction of the cost. If you select to use a mix of first and also 2nd home loans, you are likely to have initial settlement cost savings. If you fail on your home financing, mortgage insurance repays the loan provider. When marketed by a business, it's called personal mortgage insurance, or PMI. As time passes, and also your home loan financial obligation reduces, the payment on death also reduces leaving your dependants with the money to pay the remainder of the mortgage. There are two kinds of life insurance policy that you can reach cover your home loan. Decreasing term life cover is the most usual type and pays what's entrusted to pay on your home mortgage. You can likewise take out level term, which pays out an established round figure if you die within a fixed term - this can be used to settle an interest-only home mortgage. Whatever plan you make a decision, make certain to shop around to locate the best plan for you. Home loan life insurance policy can the sensible option if what's essential it to pay off your mortgage and get a policy that would likewise pay your home mortgage if you end up being handicapped or lose your work. The advantage to purchasing home loan security insurance policy is that it might be less costly than life insurance policy and you might not be required to go through a medical exam. Even though your costs remain the exact same, the payout amount maintains reducing as you pay your mortgage off. Which costs typically is a lot greater than what you would certainly spend for term life insurance policy. If you are required to pay personal mortgage insurance, it normally comprises a portion of your regular monthly mortgage repayment, in addition to your principal, rate of interest, real estate mortgage insurance and tax calculator tax, and homeowners insurance policy. Similar to passion, property tax, as well as home owners insurance, repayment of your PMI does not develop equity in your home. The lenders that do this are still shielding their mortgage by charging a security cost to cover the home loan, yet it's not an insurance plan. By doing this, the lending institutions are staying clear of having to charge the appropriate government costs and fees such as GST or stamp obligation which are applicable on all types of insurance coverage. Cost savings in this scenario are handed down to the borrower by way of no federal government input tax obligations. The majority of the charges or costs applicable in this case are also substantially less expensive than the typical LMI that is billed by the lenders. Life insurance covers the worst-case circumstance, however it's additionally important to take into consideration how you could pay your bills or your home loan if you could not function because of disease or injury. It's a conforming lending for low- and also moderate-income residence customers that allows a deposit of 3% and does not require mortgage insurance. For instance, allow's say you got a residence with a worth of $100,000 as well as put a down payment of 10%, or $10,000, as well as got a $90,000 lending to pay the rest. Your LTV in this situation would be $90,000 separated by $100,000, or 90 percent. The longer you pay for your home loan, the lower your loan-to-value (LTV) will end up being. On federal government lendings, mortgage insurance is generally called for regardless of the LTV. Say you're getting a $200,000 home with a 30-year fixed-rate home mortgage. If you place 20% down as well as you have a 4% rate of interest, you'll pay $275,000 over the life time of the car loan. If you place 5% down, your rates of interest may be higher-- claim, 4.25%-- and you'll need to obtain a larger amount.

If you pass away, a household living in a residence with a mortgage that you pay-- a life insurance policy can give for them. Life insurance policy can pay your dependents cash as a round figure or as regular repayments if you pass away. If you're able to pay 20% in advance, you're also more probable to get accepted as well as you'll score much better rate of interest. A smaller obtained quantity as well as a reduced interest rate can easily shave 10s of thousands of bucks off your financing.