Download

1 / 5

0 likes | 10 Vues

Securing a business line of credit can be a game-changer for small businesses looking to manage cash flow, cover unexpected expenses, and seize growth opportunities. As we enter 2024, several lenders stand out for offering competitive business lines of credit with favorable terms and conditions. Hereu2019s a look at the top five lenders to consider:<br><br>

E N D

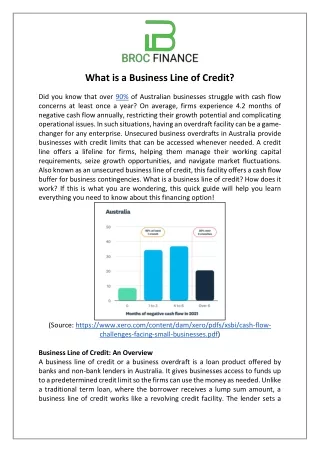

In the ever-evolving landscape of small business financing, a business line of credit stands out as a flexible and powerful tool. It provides the necessary liquidity to manage cash flow, cover unexpected expenses, and capitalize on growth opportunities. As we move into 2024, understanding how to secure a business line of credit is essential for business owners looking to maintain stability and drive success. This comprehensive guide will walk you through the steps, considerations, and benefits of obtaining a business line of credit. Understanding a Business Line of Credit A business line of credit is a revolving loan that provides access to a predetermined amount of funds. Unlike a traditional loan, which disburses a lump sum that is repaid over time, a line of credit allows businesses to draw and repay funds as needed, up to the credit limit. This structure offers flexibility and ensures that interest is only paid on the amount borrowed. Why Secure a Business Line of Credit? 1. Improved Cash Flow Management Fluctuating cash flow is a common challenge for small businesses. A line of credit can bridge gaps between receivables and payables, ensuring that operational expenses, payroll, and other obligations are met without interruption. 2. Emergency Preparedness Unexpected expenses, such as equipment repairs or sudden drops in revenue, can be detrimental to a business. Having a line of credit provides a financial safety net, enabling businesses to handle emergencies without significant disruption. 3. Funding Growth Opportunities When growth opportunities arise, quick access to funds is crucial. A business line of credit can finance marketing campaigns, new product launches, or expansion projects, allowing businesses to seize opportunities without delay. 4. Cost-Effective Borrowing Lines of credit generally offer lower interest rates than credit cards and other short-term financing options. Additionally, interest is only charged on the amount borrowed, making it a cost-effective solution for short-term financial needs. Steps to Secure a Business Line of Credit 1. Evaluate Your Business Needs

Before applying for a line of credit, assess your business’s financial situation and determine the purpose and amount of credit needed. Understanding your needs will help you choose the right type of credit and prepare a strong application. 2. Check Your Credit Score Both personal and business credit scores play a crucial role in the approval process. Lenders use these scores to assess your creditworthiness. A higher credit score increases your chances of approval and can result in better terms and lower interest rates. 3. Gather Financial Documentation Lenders will require detailed financial information to evaluate your application. Prepare the following documents: Business financial statements (balance sheet, income statement, cash flow statement) Tax returns (both personal and business) for the past two to three years Bank statements for the past six months Business plan with financial projections 4. Choose the Right Lender Research different lenders, including traditional banks, credit unions, and online lenders. Compare their terms, interest rates, fees, and eligibility requirements. Choosing the right lender can significantly impact the cost and accessibility of your line of credit. 5. Submit Your Application Once you’ve gathered your documents and selected a lender, complete the application process. Ensure that all information is accurate and complete to avoid delays. Be prepared to answer questions about your business’s financial health and how you intend to use the funds. 6. Review the Terms and Conditions If approved, carefully review the terms and conditions of the line of credit. Pay attention to the interest rate, repayment terms, fees, and any covenants or restrictions. Understanding the terms will help you manage the credit line effectively. Types of Business Lines of Credit 1. Secured Business Line of Credit

A secured line of credit requires collateral, such as real estate, inventory, or receivables. This reduces the lender’s risk and can result in higher credit limits and lower interest rates. However, the risk to the business is higher as the collateral is at stake. 2. Unsecured Business Line of Credit An unsecured line of credit does not require collateral. While easier to obtain, it typically comes with lower credit limits and higher interest rates. This option is suitable for businesses with strong credit scores and stable financial histories. 3. SBA Line of Credit The Small Business Administration (SBA) offers lines of credit through its CAPLines program, which includes: Seasonal Line of Credit: To finance seasonal increases in receivables and inventory. Contract Line of Credit: To finance direct labor and material costs for contracts. Builders Line of Credit: For construction or renovation projects. Working Capital Line of Credit: For general working capital needs. SBA lines of credit are partially guaranteed by the government, making them more accessible to small businesses. Managing Your Business Line of Credit 1. Use Funds Strategically Draw funds from your line of credit only when necessary and for purposes that will generate a return on investment. Avoid using it for discretionary spending to maintain financial health. 2. Monitor Your Credit Usage Keep track of how much you’ve borrowed and ensure that you’re making regular payments. Staying within the credit limit and avoiding maxing out the line will help maintain a good credit score and ensure continued access to funds. 3. Plan for Repayments Develop a repayment plan that aligns with your cash flow. Regularly repaying the borrowed amount not only reduces interest costs but also replenishes your available credit, providing a continuous financial cushion. 4. Maintain Financial Records

Keep detailed records of your draws, repayments, and the purpose of each transaction. This will help you manage your credit line effectively and provide necessary documentation for future credit applications. Benefits of a Business Line of Credit 1. Financial Flexibility The revolving nature of a line of credit provides ongoing access to funds. This flexibility is invaluable for managing day-to-day operations and responding to unexpected financial needs. 2. Improved Cash Flow With a line of credit, businesses can manage cash flow more effectively, ensuring that they have the funds needed to cover expenses even during periods of low revenue. 3. Credit Building Responsibly managing a line of credit can help build your business credit score. A higher credit score can lead to better financing options and terms in the future. 4. Cost Savings Compared to other short-term financing options, lines of credit typically offer lower interest rates. The ability to draw and repay funds as needed also minimizes interest costs. 5. Opportunity to Seize Growth Access to funds allows businesses to act quickly on growth opportunities, such as new market expansions, product launches, or strategic investments. Potential Drawbacks 1. Risk of Over-Borrowing The ease of access to funds can lead to over-borrowing and increased debt. It’s crucial to use the line of credit responsibly and avoid borrowing more than necessary. 2. Variable Interest Rates Many lines of credit have variable interest rates, which can increase over time and affect the cost of borrowing. Understanding and planning for potential rate changes is essential. 3. Potential Fees

Lines of credit may come with various fees, including annual fees, maintenance fees, and draw fees. Be aware of these costs and factor them into your financial planning. Conclusion Securing a business line of credit in 2024 can provide small businesses with the financial flexibility and stability needed to navigate challenges and seize opportunities. By understanding the benefits, carefully preparing your application, and choosing the right type of credit, you can leverage this powerful financing tool to support your business’s growth and success. Contact us 5starprocessing fo rmore information.