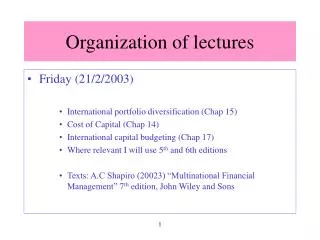

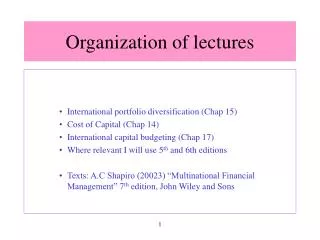

Organization of lectures

1.01k likes | 1.22k Vues

Organization of lectures. International portfolio diversification (Chap 15) Cost of Capital (Chap 14) International capital budgeting (Chap 17) Where relevant I will use 5 th and 6th editions Texts: A.C Shapiro (20023) “Multinational Financial Management” 7 th edition, John Wiley and Sons.

Organization of lectures

E N D

Presentation Transcript

Organization of lectures • International portfolio diversification (Chap 15) • Cost of Capital (Chap 14) • International capital budgeting (Chap 17) • Where relevant I will use 5th and 6th editions • Texts: A.C Shapiro (20023) “Multinational Financial Management” 7th edition, John Wiley and Sons 1

Organization of lectures Saturday • Working Capital Management (Chapter 19) • Financing Decisions (Short terms vs Long terms) (Chapter 19 and Chapter 18) • Managing the Multinational Financial System (Chapter 20) 2

Organization of lectures Saturday • Special topics • Forward market (Chapter 7) • Currency futures and options (Chapter 8) • Swaps/interest rate management (Chapter 9) 3

Organization of lectures Saturday • Revisions • Take home assignments • Final exams 4

LECTURE 5

International Portfolio Investment • Gist of lecture • International diversification provides better risk-return tradeoff • Higher return with less risk • Measures dollar return on foreign denominated securities 6

International Portfolio Investment • Why invest internationally?? • Are there any tangible benefits?? • It all started with the work of of Harry Markowitz ….. developed modern portfolio theory 7

PORTFOLIO DIVERSIFICATION • Simple illustration of portfolio diversification (case of 2-stock portfolio: see excel worksheet) • Ibm + gm; gm + alcoa; gm + ibm • US + UK; US + Spain (Problem 9 end of chap) • Expected return of individual vs portfolio • Standard deviation as measurement of risk • Concept of correlation/covariance 8

2-asset portfolio Rp = w1R1 + W1R2 Stdp = SQR RT {w12var1 + w22var2 + 2w1w2corr1,2std1std2} 9

Computing int investment • Ex rate value FC Value HC • T=0 eo FCo FCo*eo • T=1 e1 FC1 FC1*e1 • Return HC = FC1*e1 / FCo*eo - 1 • RHC = (1+RFC)(1+g) - 1 12

Problem 1 Chap 15: 7 eds • British gilt went from 102 to 106 pound • Coupon 9 pound • eo: $1.76/pound ; e1: $1.62/pound • RHC = (1+RFC)(1+g) – 1 • = (1+{[106-102+9]/102})(1+[1.62-1.76]/1.76) – 1 • = 3.79% 13

Problem 2 • RHC, Swiss • = (1-0.016)(1+0.08) – 1 • = 6.27% • RHC, France • =(1+0.018)(1+0.026) –1 • = 4.45% • Higher? France/Swiss 14

Problem 3 • RHC = ?? • RFC = (1+[11,200 • -9,000+60]/9000) • g = (1/120 – 1/145)/(1/145)) • Answer: 51.17% 15

Prob 4, 5, & extra • Prob 4: Answer = 51.4% (1+1.12)(1-0.286) -1 • Prob 5: Answer (a) = 8.5% compare to (1+11.17)(1-0.914) -1= 4.66% • (b) = (1+41.9)(1-0.95.9) –1 = 75.89% • extra: Answer = • Aus (38%) fran (40.4) italy (14.4) swe (53.6) • Bel (41.4) w ger (16.2) japan (45.9) swit (14.4) • Can (19.2) hol (28.5) spain (22.8) uk (7.2) 16

German bonds yields > US, indicate higher inflation rate; therefore euro must depreciate/US appreciate RHC = 6.5% RFC = 9.8% Invest $1 in german bonds at an exchange rate of euro 1.1372/$ Beginning wealth equals (in euros) = 1.1372 Ending wealth (in euros) = 1.1372(1.098) In US$ equals 1.1372(1.098)e1 (e1= $/euro) Set equals to investment in US bonds where ending wealth equals 1.065 e1 = $0.8529 (or 1.1724/euro) Prob 6: ex rate app/dep 17

Foreign market beta from US perspective • BFC = COV (RFC, RUS)/VARUS • = (Corr (RFC, RUS) * STDFC * STDUS) / VARUS • = Corr (RFC, RUS) * STDFC/ STDUS 18

Prob 10 (12 for 6ed) Bmex = (corrUS,Mex * Stdmex)/StdUS = (0.34 * 0.297)/0.127 = 0.8 Prob 8 BUK = (corrUS,UK * StdUK)/StdUS = (0.67 * 0.38)/0.22 = 1.16 Problem 8 and 10 19

Return in HC • RHC = RFC + Rg • STDHC = (VARFC + VARg + 2COVFC,g)1/2 • Problem 10 • STDHC = (VARFC + VARg + 2COVFC,g)1/2 • STDHC = (0.192 + 0.152 + 2*0.17*0.19*0.15)1/2 • = 0.27 < (0.19 + 0.15) = 0.34) 20

Cost of Capital • Gist of Lecture • A project’s cost of capital is a function of the riskiness of the project itself and not the risk of the firm undertaking the project • Even if foreign investments are riskier than domestic investments, that does not mean that COCFC > COC HC • Systematic risk is priced (CAPM) • Measurement of systematic risk: globally diversified portfolio vs domestically diversified portfolio 21

COST OF CAPITAL • Definition • Simple illustration • WACC • Project risk similar to parent • Project risk not similar to parent • Computing cost of equity capital • Computing cost of debt capital • Retained earnings?? • Illustration 22

Estimating cost of equity capital • Def: minimum rate of return to induce investors to buy/hold firm’s stock; designated as ke. • Rate used to capitalize equity portion of corporate cash flow. • Useful if project specific required return on equity similar to corporate norm. • 2 approaches • CAPM • Gordon Valuation Model 23

Issues in estimating cost of equity using CAPM • Market portfolio (Rm) • US/global market portfolio (not local) • Proxy company • Preferably domestic company where project is located (estimate beta) • Risk premium (Rm – Rf) • Preferably US risk premium 24

Problem 2 Chap 14: 7 edition • Using CAPM; rproject = 17.95% • Example using Gordon’s Model • COC in relation to P/E (or E-P) • No growth • Constant growth • Question 3; 7th edition 25

Cost of debt capital • other version e.g 7 edition = rf(1+c)(1-tf) +c (combining d and g) • c = e1 – eo/eo (c = +ve implies FC appreciation and c= -ve connotes depreciation) • After tax dollar cost of LC (FC) 1 year loan (shown on today’s lecture) = rf(1-d)(1-tf) – d [d = case of depreciation (d = eo – e1/eo)] and rf(1+g)(1-tf) + g [case of appreciation (g = e1 – eo/eo)] • After tax cost of HC (US) 1 year loan = rHC(1-tf) – dtf ( d can be replace by c and the usual interpretation applies (i.e – dtf becomes + ctf ) 26

Cost of debt capital (continued) • Appendix 19A: Dollar cost of long term debt (before and after tax) • Solve r using IRR for LC loan vs HC loan (no tax and tax cases): similar as in finding YTM as in bond valuation • Dollar cost of LC loan (no tax) = rf(1+g) + g (annual revaluation; g = e1 – eo/eo ) • Equate rHC = rf (1+g) + g to find rf* • General rule rf > rf* borrow at rHC (otherwise borrow at rf) • Equal means indifferent • After tax dollar cost of LC loan = rf (1+g)(1-tf) + g • To find rf* equate rHC(1-tf) = rf (1+g)(1-tf) + g 27

Cost of debt capital (continued) • Price of bond = PV after tax interest + PV maturity value • Po(1-f) = € [Interest (1-t)]/(1+YTM)t + M/(1+YTM)n • Solve for YTM = IRR = after tax cost of debt • E.g public issue of 8% - 10 year bond, price at $1000 with 4% floatation cost and M = $1000 and corporate tax of 40%. • To find YTM or IRR equate 1000(1-4%) = €80(1-0.4)/(1+YTM)t + 1000/(1+YTM)n • Solving for YTM via trial and error method yields 5.35% 29

Problem 3, Chap 14: 7 edition • a. Today’s lecture: dollar costs of borrowing LC = rFC(1-d) – d (no tax case) • = 0.075(1- 0.017) – 0.017 = 5.67% • Cost of borrowing LC < rHC of 6.7% • b. equating the two to find d = 0.74% (indifferent of borrowing in LC (FC) and HC ($) • c. (Today’s lecture): after tax dollar costs of borrowing in LC = rFC(1-d)(1-tFC) -d = 4.78%. 30

Weighted average cost of capitalWACC • ko = (1 – L)ke + Lid(1 – t) • Capital structure based on market value (L and 1-L) • Target capital structure • E.g 60% equity; 30% debt and 10% preferred stock • After tax costs 20%, 6% and 14% respectively • WACC = ko = 0.6*0.2 + 0.3*0.06 +0.1*0.14) = 15.2% 31

Problem 1 Chap 14: 7 edition • WACCproject = ko = (1 – L)ke + Lid(1 – t) • (2/3 *0.12) + (1/3 * 7%) = 10.33% • WACCparent = ko = (1 – L)ke + Lid(1 – t) • (2/3 *0.15) + (1/3 * 7%) = 12.33% • Unlevered beta = Bu = BL /[1 + (1-t)D/E] = 1.21/[1+(1 – 0.4)1/2] = 0.93 32

Weighted average cost of capitalWACC (continue) • No change in risk characteristic of parent • WACCproject = kI = ko – a(ke-ks) – b[id(1-t) – if] • With change in risk characteristic of parent • WACCproject = kI = ko + (1-L)(k’e-ks) + L(id’ – id) - a(k’e-ks) – b[id’(1-t) – if] • Shapiro(1978) “Financial structure and COC of MNC” JFQA 32

Example in computing kI = kproject under no risk and risk characteristics • New foreign project = $100mil (20 parent, 25 retained earnings and 55 debt of subsidiary) • Ke(parent) =14%; kd(parent or id) = 5%; L=30% • Ko (WACC parent) = 0.14*0.7 + 0.05*0.3 =11.3% • Project higher risk; ke’ =16; kd’ (id’)=6%(after tax) and ks (based on 8% incremental tax) = 16(1-0.08) = 14.7% • Let rf = 20%; d = 7% and tf = 40% then dollar costs (today’s lecture) of LC = 0.2(1-0.07)(1-0.4) – 0.07 = 4.2% (if) • Applying kproject with change in risk characteristic = 0.113 + 0.7(0.16-0.14) + 0.3(0.06 – 0.05) - 25/100(0.16 – 0.147) – 55/100(0.06 – 0.042) = 11.7% • WACC (parent) in absence of foreign debt and retained earnings = 0.16*0.7 + 0.3*0.06) = 13% • No change in risk kproject = 0.113 – 25/100[0.14-0.14(1-0.08)] – 55/100(0.05 – 0.042) = 10.58% 33

Diff bet parent and project cash flow Cannibalization Sales creation Opportunity cost Transfer pricing Tax and royalties Foreign tax regulation expropriation Blocked funds Ex rate changes/inflation Project specific financing Different business risk of foreign and domestic risk Issues in international capital budgeting 34

CAPITAL BUDGETING • CONCEPT OF CASH FLOW (2 APPROACHES) • METHODS • NPV • IRR • PI • PAYBACK • ILLUSTRATION • INCREMENTAL CASH FLOW • APV • 3 STAGES APPROACH 35

Concept of cash flow • P/L App 1 App 2 • S (100) PAT + Dep After tax CF • V(50) = 16.5+10 + tDep • FCC (ex dep) (10) = 26.5 (100 – 50 – 10)(1-0.45) • Dep (10) + 0.45(10) • PBT (30) = 26.5 • Tax 45% (13.5) • PAT (16.5) 36

Illustration of methods • E.g NPV = - 10 + 1.666 + 2.082 + 2.895 + 2.41 + 2.814 =1.867 IRR = point where NPV = 0 PI = (1.666 + 2.082 + 2.895 + 2.41 + 2.814)/10 Payback = cumulative CF turn from –ve to +ve 37

Desirable properties of NPV • Definition: NPV = PV (inflows) – PV (outflows) • Theory: PPC/IRR/COC • Consistent with shareholder wealth max • Value additivity principles 38

APV (Adjusted PV mtd) • APV = PV investment outlay + PV operating cash flow (discounted by ke) + PV interest tax shield + PV interest subsidies • Ke = rf + (rm – rf)Bu • MM II: ke = ka + (ka-rf)(1-t)D/E • Ka = rf + (rm – rf)BL • Bu = BL /[1 + (1-t)D/E] 39

3-stage example • IDC-Uk Exhibit 18.1 to 18.7 • 1. Estimating cf from subsidiary stand point • 2. Forecast cf due to parent company • 3. Adjustment for lost sales (cannibalizing) etc. • Adjustment for ex rate changes and inflation (prob 2 chap 18: 5th edition • Political risk consideration. (prob 1 chap 18: 5th edition). 40

Principal cash ouflows Initial investment outlay (plant, equipment, working capital Operating expenses Extra working capital as sales expand Tax paid on net income Principal cash inflow Sales to England and other EC countries Tax shield on depreciation and interest charges Interest subsidies Terminal value of investment including recapture of working capital IDC-UK project 41

Diff between cash flows of IDC-US and IDC-UK • Funds remitted to IDC-US by IDC-UK (e.g dividends) may be subjected to additional taxes paid to UK or US. These are cash outflows from IDC-US and not IDC-UK • IDS-US owes tax to US IRS on gain associated with sale of equipment for $5m which have zero book value • IDC-US receives licensing and overhead allocation fees and incurs no additional expenses. These are costs to IDC-UK • IDC-US also profits from exports to IDC-UK • If the sales of IDC-UK are substitute for exports from IDC-US, adjustment for lost sales. 42

Political and economic risk analysis • 3 approaches • Reduce payback • Adjusted discount rate (higher) • Adjusted cash flow (recommended) • E.g (adjusting CF) • UFC worried about bananas plantation in Honduras …. Appropriation at year end • Honduran govt promise $100mil (year end) if expropriated • Value of plantation at year end = $300 mil (no expro) and $100 mil (if expro). Wealthy Honduran offer $128mil. If discount rate = 22%, find prob of expro at which UFC indifferent bet selling now and keeping it • If p = prob of expro; Expected value (year end) = p*100 + (1-p)*300 • Discount to PV = 300-200p/1.22 and equating with $128 gives a p value of 72%. Therefore if prob of expro > 72% (sell now) and if <72% (holds). 43

prob 1 chap 18: 5th & 6 (chap 21) edition). • Suppose firm project $5 till perpetuity from an investment of $20 m in Spain. Find prob of expro in year 4 before inv has –NPV. (assume no compensation and discount rate of 20%) • NPV with = -20 + 5/1.2 + 5/1.22 + 5/1.23 + 5(1-p)/.2/(1.2)3 • Set equal 0 and solve for p 45

Exchange rate changes and inflation • To analyzed separately: 1st correcting foreign cf with inflation and then convert to HC via ex rate adjustment. • For inflation two stage procedure • Convert nominal cfFC to nominal cfHC • Discount nominal cfHC with rHC • E.g: suppose with no inflation forecast CF2 =FF1 mil with eo=$0.2; CF2 = $200,000 • Suppose inflation in France = 6% annually and FF devalue with eo year 2= $0.1767. • Then forecast CF2 = FF1 mil (1+0.06)2= FF1.1236 • Equivalent to FF1.1236 * eo year 2 =$198,540 46

prob 2 chap 18: 5th & 6th (chap 21) edition • Inv in France generates $2mil annually. Projected inflation in France =7%; US=4% • Real exchange rate remain constant, find depreciation charge at year end 5?? ($ term) • If real ex rate unchanged, $ value of depreciation will decline at 7% annually. If French tax rate is 50%, depreciation charge of $2mil will worth $1mil today. If real dollar value is declining at 7% annually then real value of deprecation at year end 5 = $1mil/1.075 = $712,986. 47

Delaying project/blocked funds • Exhibit 18.10 (5 edition) or exhibit 21.10 (6 edition) for an illustration that delaying project (because of growth option) generate a positive NPV. • See exhibit 21.9 6th edition (adjusting CF) 48

Individual assignment • Collect monthly prices on two companies listed on JSE for a period of 37 months • Compute monthly return for 36 months • compute average return over the period • std deviation of return • Cov/corr • Perform a simple analysis of portfolio of these 2-stock. 49

LECTURE 50