Download

1 / 19

190 likes | 420 Vues

The most vulnerable in time of market downturns are those in retirement living on investment income AND Those investors with a high growth risk profile who receive low income. This presentation will discuss techniques to assist both the above categories of investors as well as accumulators.

E N D

The most vulnerable in time of market downturns are those in retirement living on investment incomeANDThose investors with a high growth risk profile who receive low income.This presentation will discuss techniques to assist both the above categories of investors as well as accumulators. INVESTING IN VOLATILE TIMES Monday 10th November 2008

OPTIMIST The market has bottomed ACTION Buy now to take advantage of a perceived opportunity PESSIMIST The markets will get worse ACTION Sell now to avoid further losses

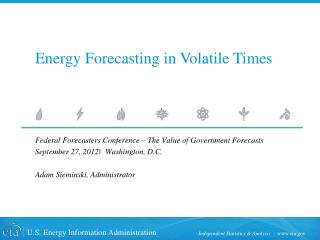

Global Sharemarkets 1986 - 2008 MSCI World Ex Aus in AUD Credit crunch 1800 Tech wreck 1600 1400 1200 1000 800 Crash of ‘87 600 400 200 0 1997 1998 1999 2006 1993 1994 1995 1996 2000 2001 2007 2008 1992 2005 2004 2002 1985 1987 1989 1991 1986 1988 1990 2003 Source: Bloomberg. Data from 1 January 1985 to 1 October 2008 (weekly).

Take the Emotion Out of the Equation • Re-Evaluate your risk profile and years to retirement. • Conservative • You are prepared to only invest into growth assets e.g. shares and property within a guaranteed portfolio. This means you are prepared to sacrifice higher potential return for the security of protecting the value of your capital against market fluctuations.

Cautious • You are comfortable with an overall portfolio that has a lower exposure to growth asset classes (shares, property and international investments). This means you are seeking • -Stable income stream, • -Lower growth on the capital invested, • -Medium to long term capital security. • You appreciate that money placed within investment funds is subject to market forces, which means that the value of the investment may rise and fall. You are prepared to accept these market movements (which are generally short-term in nature) in anticipation of achieving potentially higher long-term returns than those provided by investments whose entire asset composition is in cash or fixed interest funds.

Balanced • You are comfortable with investment funds that have a reasonable exposure to growth asset classes (shares, property and international investments). • You are willing to pursue potentially greater long term returns while accepting short term volatility. Your aim is capital growth over a period of longer than five years and your investment portfolio includes equities, property and international investments balanced by fixed interest securities and/or deposits. You will have exposure to offshore markets which may also entail exchange rate fluctuations. • Money placed within investment funds is subject to market forces, which means that the value of the investment may rise and fall. You are prepared to accept these market movements (which are generally short-term in nature) in anticipation of achieving potentially higher long-term returns.

Managed Growth • You are comfortable with investment funds that have a higher exposure to growth asset classes (shares, property and international investments). • You are an investor who is willing to pursue some speculative investments within a portfolio. You appreciate and accept that a portion of your portfolio may be exposed to negative returns and increased volatility. Capital growth rather than income is your aim. You have significant exposure to share markets, with some fixed interest component. • You appreciate that money placed with investment funds will be subject to market fluctuations which means that the value of the investment will rise and fall. The minimum investment time frame for this strategy is 7 years.

High Growth • You are comfortable with investment funds that have a higher exposure to growth asset classes (shares, property and international investments). • You are an investor who is willing to pursue some speculative investments within a portfolio. You appreciate and accept that a portion of your portfolio may be exposed to negative returns and increased volatility. Capital growth rather than income is your aim. You have significant exposure to share markets, with some fixed interest component. • You appreciate that money placed with investment funds will be subject to market fluctuations which means that the value of the investment will rise and fall. The minimum investment time frame for this strategy is 7 years.

Techniques for Mitigating Risks for Retirees • 1.Consider your income needs. If your pension is above the minimum 4% of assets, consider recontribution to superannuation to increase the tax free component of your fund (if you are under 65) or 65-75 (5% of assets). • Note work test obligations for people 65-75. • 2. Ensure that all pension is drawn purely from the cash component of your fund.

Techniques for Mitigating Risks for Retirees (cont’d) • 3. A fundamental rule is to always ensure that pensions are drawn purely from the cash component. • We always set up pensions with three years in cash. We are comfortable running down the cash component in the lean times so that other asset classes can be left alone to recover. • Remember just as you have not made a profit until you sell, you likewise have not crystallised a loss until you sell.

Techniques for Mitigating Risks for Retirees (cont’d) • 4. Consider cash out and re-contribution to maximise tax free component. • 5. Remember the impact of franking credit on the cash flow for your superannuation fund. A 30% franking credit is paid tax free to the super fund for shares held when the return is lodged. There are no franking credits on any other asset class. • 6. If you have run your cash reserves low, consider selling to release cash, but buyback using gearing.

Accumulators 1. Review certainty of income from business or employment. 2. Consider capital protected investment 3. Utilise dollar cost averaging – don’t try to pick up the bottom of the market

Accumulators (cont’d) 4. Consider setting up a SMSF and move assets outside super to super to take advantage of lower prices, eg. Trusted shares, unlisted Property Trusts, Business Real Property and Managed Funds 5. Prepay interest in advance. Lodge S221D variation form to receive lower PAYG & higher take home income, rather than wait for a large lump sum.

Accumulators (cont’d) 6. Gearing Opportunities in Superannuation • Legislation changes have enabled investors to gear within superannuation. • The structure allows double the dividends to be earned and double the franking credits for the same amount of money, whilst doubling your exposure. • The risk is similar to margin loan, but the super fund can self fund.

Accumulators (cont’d) 6. Gearing Opportunities in Superannuation (Self Funding Instalment Receipts or Limited Recourse Loans) • The loan is limited recourse, and therefore lender has no claim over other superannuation or personal assets. • Able to invest in Top 100 ASX listed shares • Receive the benefits of increased dividends, franking credits and exposure to shares. • Potentially take advantage of having greater exposure to the market when the market recovers.

Summary • Market will rebound – it’s just a case of when. • Remember you risk profile and stick to your investment strategy. • Pension funds should have sufficient cash to ride out 3 years of tough times. • Gearing opportunities in superannuation. • Restructure assets outside super to super to retire debt • Dollar Cost Averaging • Capital Protection