Download

1 / 113

1.14k likes | 1.25k Vues

Join Celia L. Broadus, CPA, for an informative series on effective financial management tailored for nonprofit organizations. This two-part session will cover best practices, tools for assessing financial health, and essential conversations surrounding the economic realities that nonprofits face. You will learn about budgeting, planning, and how to safeguard funds to enhance sustainability. Perfect for nonprofit leaders and stakeholders dedicated to maximizing their organization's impact with sound financial strategies.

E N D

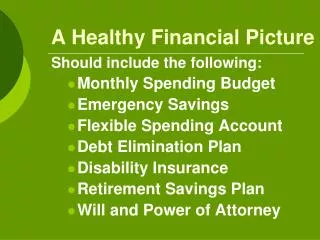

MANAGING YOUR FINANCIAL PICTURE May 6th and 13th 2013 Celia L . Broadus, CPA, Instructor

Introduction We believe this combination of excellence in operations and strong execution of our strategy is critical to achieve our vision. We will continue to focus on both in future as well." — AzimPremji

Introduction • MANAGING YOUR FINANCIAL PICTURE WILL: • Introduce and reinforce best practices of sound financial management • Provide tools for assessing the financial health of a nonprofit organization • Facilitate robust conversations and discussions surrounding the economic realities that nonprofit organizations operate within.

Introduction - Definitions Financial management means recording all of the monetary (and some nonmonetary) transactions of your organization.

Introduction • Financial management also means reporting those transactions in standard forms that show the financial position and performance of your organization.

Introduction • And financial management means ensuring that the organization’s funds are safeguarded and used prudently, now and in the future. • It involves accounting, information management and planning.

Introduction • Public funds for non profit organizations are always scarce and organizations must be both efficient and effective users of this resource!

Budget/Planning • People think focus means saying yes to the thing you’ve got to focus on. But that’s not what it means at all. It means saying no to the hundred other good ideas that there are. You have to pick carefully. I’m actually as proud of the things we haven’t done as the things we have done.” –Steve Jobs

Budget/Planning • Nonprofit Organizations(NPO) must constantly strive for sustainability. A well-planned budget will focus on the primary goals and objectives of the organization and provide financial and programmatic adaptability …………………..key ingredients to maximum sustainability.

Budget/Planning • It is the monetary forecast of your organization’s finances and operations over a certain period of time.

Budget/Planning A policy document used to measure the financial performance of the organization, both how well it is generating revenue and controlling expenses and how well it uses it’s limited financial resources to achieve its mission.

Budget Committees Should reflect the collective knowledge of the organization concerning the goals and objectives for the period in question.

Budget Committees Qualities of committee members • Familiar with prior year activities and potential changes that contemplated in the year/s to come. • A desire to serve the organization as a whole rather than lobby particular project. • Knowledge of ordinary budgeting business or personal.

Budget Committees • Tasks and steps to developing the budget • Define the budget timeline • Estimate the cost or resources required to achieve each objective or goal. • Estimate the expected dates and amount of revenue that will be generated • Verify that revenues exceed expenses • Develop final budget

Types of Budgets Operating Budgets Capital Budgets Program Budgets Cash flow projections Break even projections

Operating Budget • Describes all the day to day income and operating expenses of an organization • Track the fiscal year of the organization.

Operating Budget • Projects into the future of the line items within an organization’s revenue statement • Form the basis of evaluating income/expense reports.

Operating Budget • The basic math Projected income to pay for operating expenses • Projected operating expenses______________Projected operating surplus or deficit

Putting Together the Budget • Operating income includes: • Expected revenues from contracts or fees charged • Expected grants earmarked for operations vs. those for capital projects • Expected interest or investment income

Putting Together the Budget • Operating income does not include: • Loan principal payments expected. This should be included with the capital budget or cash flow projection.

Putting Together the Budget • Operating Expenses • Cash operating expenses, often called overhead. • Depreciation expenses, non cash or paper expenses • Interest paid on loans

Putting Together the Budget • Operating Expense do not include: • Loan principal payments • Considered capital expenses not related to operating costs • Disbursements made in acquiring fixed assets

Putting Together the Budget • Areas to exercise extra care(conservative approach): • Estimating salaries and expenses. • Estimating the amount of staff or consultant time needed for a particular project. • Projecting grant funding for your organization.

Putting Together the Budget • Verifying the numbers The reliability of budget numbers is no better or worse than the raw data on which the numbers are based. This data is called assumptions.

Putting Together the Budget • Verifying the numbers cont.. Assumptions three categories • Unit costs , i.e.. rental costs per sq foot • Quantity estimates, i.e.. number of sq feet • Lump sum estimates- such as amount of expected grant(not committed).

Putting Together the Budget • Verifying numbers cont.. • Ways to verify • Vendors • Other organizations with similar missions, programs, etc. • Outside consult or expertise

Putting Together the Budget • Contingency and Reserve Accounts • Primary Purpose to offset risk and provide a financial cushion • Funds are put away for a certain purpose • If used in operations, typically represent 2%-5% of the overall budget. • Estimating contingency or operating reserves

Concepts Direct vs. Indirect Direct costs – relate to a specific project or program Indirect or Overhead costs – may not relate to a specific project but may be necessary for its completion.

Concepts Functional Classifications • It is a method of grouping expenses according to the purpose for which the costs are incurred • The primary functional classifications are program services and supporting activities • Program, Management and General, and Fund-raising classifications are functional classifications thought to be predominant in practice

Concepts Joint Activities and Costs Joint activities that are not identifiable with a particular component of the activity Activities that are part of the fund-raising function and have elements of other functions such as programs and/or management and general • An example of a joint activity is an annual dinner that promotes the entity’s programs in addition to raising funds.

Concepts Allocation of Joint Costs Three criteria need to be met to allocate joint costs: 1)Purpose 2)Audience 3)Content The exception-Costs of goods/services in exchange transactions If any of the criteria are not met, all costs of the joint activity is reported as fundraising

Concepts Allocation of Joint Costs • PURPOSE criterion is met if the purpose of the joint activity includes accomplishing program or management and general functions by calling for specific action by the audience that will assist the entity in accomplishing a specific program, mission or goal

Concepts Allocation of Joint Costs • Audience has a specific need or a reasonable potential for use of the specific program action component of the joint activity Audience has the ability to take the proposed action or assist with the specific program action component of the joint activity

Concepts Allocation of Joint Costs • CONTENT criterion is met if the joint activity supports program or management and general functions

Concepts Allocation Methods • Simple Allocation-a single factor used to divide overhead between programs, departments, etc • Multiple Allocations-many factors used to allocate overhead, i.e. percentage, sq foot, labor hours, use.

Budget Exercises • Exercise 1 – Determine who’s involved in your budgeting process? • Exercise 2- Overhead budget

Budget/Planning Summary • The budget/planning process within the nonprofit organization an essential step in the financial management function.

Budget/Planning Summary • It creates the financial roadmap for operations, capital outlays and cash flow projections.

Budget/Planning Summary • It allows the organization to measure the success of program performance and its use of financial resources.

Financial Reporting • Financial Statement Primer • Assessing Your Organization’s Finances • Understanding Financial Reports • Financial Statement Analysis

Financial Reporting Overview: Financial statements are numerical descriptions of fiscal activity and status required as part of an audit. Understanding the financial statements of your organization will give you a different and important view of the nonprofit’s health and prospects.

Financial Statement Primer Overview: Well cover the common terms and classifications that comprise financial statements.

Financial Statement Primer Proper Identification • Account Classifications • Five major account types • Assets • Liabilities • Net Assets • Revenue • Expenses

Financial Statement Primer Account Classifications Assets • Current-Cash, accounts receivable, prepaid expenses and other assets • Investments-stocks, bonds and other securities

Financial Statement Primer Account Classifications Assets • Fixed Assets-Land and durable property and equipment • Other Assets-catch all for items that don’t fit into other categories.

Financial Statement Primer Account Classifications Liabilities Current Liabilities — Obligations that are expected to be satisfied with current within one year, such as accounts payable, wages and other payroll liabilities; also called short-term notes.

Financial Statement Primer Account Classifications Liabilities Long-Term Liabilities — Obligations, such as bonds, pensions and long-term notes (or loans), that are not expected to be satisfied within the current period (one year) but paid in future periods.

Financial Statement Primer Account Classifications Net Assets Assets – Liabilities = Net Assets, or, said another way: What you own less what you owe equals your net worth. The cumulative effect of all of the organization’s transactions throughout its life. 8

Financial Statement Primer Account Classifications R e v e n u e s Most nonprofit organizations classify revenues as either restricted or unrestricted. Restricted revenue Refers to income or resources that come from a special source and must be used for a specific purpose or program