Vertical Integration and Retailing

Vertical Integration and Retailing. June 6, 2006. Overview. Successive monopolies analysis Make or buy analysis, markets versus hierarchies Unbalanced throughput Monitoring problems Strategic perspectives. Vertical Integration.

Vertical Integration and Retailing

E N D

Presentation Transcript

Vertical Integration and Retailing June 6, 2006

Overview • Successive monopolies analysis • Make or buy analysis, markets versus hierarchies • Unbalanced throughput • Monitoring problems • Strategic perspectives

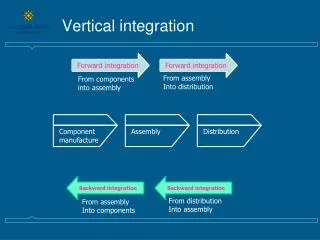

Vertical Integration • Single firm, or unified ownership, of both sides of an exchange relationship. • Individuals employed by separate firms are now employed by a single firm. • Examples: • Manufacturer owned outlets • Retailer owned warehouse and distribution • True private labels

Successive markup, independent profit maximization 6.35 (6.35-5.25)20=$22 5.25 (5.25-2.00)20=$65 2.00 20

All margin is retail, supplier delivers at cost 6.40 (4.70-2.00)47=$126.9 5.25 4.70 2.00 20 47

Retailer accepts unit markup 6.40 (5.00-4.50)42=$21.0 5.00 4.50 (4.50-2.00)42=$105.0 2.00 42 20

“Allure of Vertical Integration” • One profit-maximizing markup in the channel yields superior “channel profits.” • Achieving this is difficult without control of pricing of the supplier’s price by the retailer or retailer’s price by the supplier. • Analysis is based strictly on gross margins.

“Make or Buy” • Oliver Williamson • Make—vertical integration • Buy—using the market, outsourcing • Asset specificity, transaction specific assets • Transaction frequency • Bounded rationality and uncertainty

Transaction Specific Assets • The assets required of a retailer specific to conducting business with a single supplier. • Signage, store appearance, manufacturer marks • Equipment • Training and skills required of employees • The more transaction specific assets required of the retailer, the greater the likelihood of vertical integration

Transaction Frequency • Repetitive transactions, dealings, with a supplier versus… • One-time, idiosyncratic negotiations • The greater the transaction frequency, the greater…

Monitoring Problems • Agency problem: Providing proper incentive structure for employees to discourage “theft” from owners. • Dulled incentives--having one arm operate only to “reduce costs” rather than profit maximization

“Unbalanced Throughput” • One side of the exchange relationship cannot produce/consume the volume required to keep the other side operating at an efficient scale. • Car dealerships desiring to sell a broader/deeper line than that provided by a single supplier. • Retailers cannot sell the volume of a dedicated warehouse.

Ford’s “Dealer Network” 1998 • Obtains a controlling level of ownership within a market • Implemented one-price, no haggling approach to reduce intrabrand competition • Plan included: • Consolidation of selling locations, • Increased number of service locations

UnitedAuto, which has pursued a strategy based on internal growth from its existing dealerships, as well as from strategic acquisitions, operates 150 franchises in the United States and 96 franchises internationally, primarily in the United Kingdom. UnitedAuto dealerships sell new and used vehicles, and market a complete line of after-market automotive products and services.

Life cycle issues • Specialization is limited by the extend of the market • Economics dictate forward integration into retailing early and late in a product life cycle • Kathryn Harrigan, looks at strategic integration in mid-levels of market development, “Bailing out” in the end-game

Outsourcing versus vertical integration • Motivation • Specialization • Survival of the economically fittest • Economies of scale • Heavier market coverage • Independence from any single manufacturer

Uncertainty • “Absent significant specificity, uncertainty favors outsourcing. • “In the presence of significant specificity, uncertainty favors vertical integration forward.

Bridgestone/Firestone • Leading Bridgestone Firestone's sales recovery in North America are its almost 2,300 company-owned stores--the world's largest tire and automotive service network--and thousands of independent retailers. In support of their efforts, Bridgestone Firestone North American Tire, LLC is promoting all our main tire brands aggressively through stepped-up advertising and PR events.

“With nearly 1,500 Firestone Complete Auto Care stores nationwide, finding a store that is convenient to your home or business is easy.” Firestone Complete Auto Care

Sherwin William • Williams Company (NYSE: SHW) • 101 Prospect Ave. NWCleveland, OH 44115-1075 (Map) • Phone: 216-566-2000Fax: 216-566-2947 • No matter how you coat it, Sherwin-Williams is the largest paint manufacturer in the US and #2 worldwide, after Akzo Nobel. Sherwin-Williams' products include a variety of paints, finishes, coatings, applicators, and varnishes sold under the names Dutch Boy, Krylon, Martin-Senour, Red Devil, Sherwin-Williams, Thompson's, and Minwax. The company operates 2,700 paint stores throughout North America

Danskin • “The Company's Danskin Division operates two full-priced stores and 32 outlet stores in 18 different states. The Company's outlet stores, in addition to offering in-line merchandise, provide a distribution channel for irregulars and excess inventory.

Liz Claiborne • “Our brands include AXCESS, BORA BORA, C&C CALIFORNIA, CLAIBORNE, CRAZY HORSE, CURVE, DANA BUCHMAN, ELISABETH, ELLEN TRACY, EMMA JAMES, ENYCE, FIRST ISSUE, INTUITIONS, J. H. COLLECTIBLES, JANE STREET, JUICY COUTURE, LAUNDRY BY SHELLI SEGAL, LIZ, LIZ CLAIBORNE, LUCKY BRAND, MAMBO, MARVELLA, MEXX, MONET, MONET 2, REALITIES, SIGRID OLSEN, SPARK, SWC, TRIFARI and VILLAGER. In addition, we hold certain licenses for men's, junior's and women's sportswear, jeanswear and activewear under the DKNY(R) JEANS and DKNY(R) ACTIVE trademarks, women's sportswear under the CITY DKNY(R) trademark, jewelry products under the KENNETH COLE NEW YORK and REACTION KENNETH COLE trademarks, and fragrance, cosmetic and beauty products under the CANDIE'S trademark.

Specialty Retail Stores. As of January 1, 2005, we operated a total of 269 specialty retail stores under various Company trademarks, comprised of 158 retail stores within the United States and 111 retail stores outside of the United States (primarily in Western Europe and Canada). The following table sets forth information, as of January 1, 2005, with respect to our specialty retail stores: • U.S. RETAIL SPECIALTY STORES • ------------------------------------------------------------------------------- • Approximate Average Store Specialty Store • Format Number of Stores Size (Square Feet) • ------------------------------------------------------------------------------- • LUCKY BRAND DUNGAREES 86 2,300 • ELISABETH 30 3,000 • SIGRID OLSEN 25 2,300 • MEXX 7 10,100 • DANA BUCHMAN 4 4,800 • LAUNDRY BY SHELLI SEGAL 4 1,700 • ELLEN TRACY 1 5,300 • JUICY COUTURE 1 2,200