Download

1 / 45

450 likes | 533 Vues

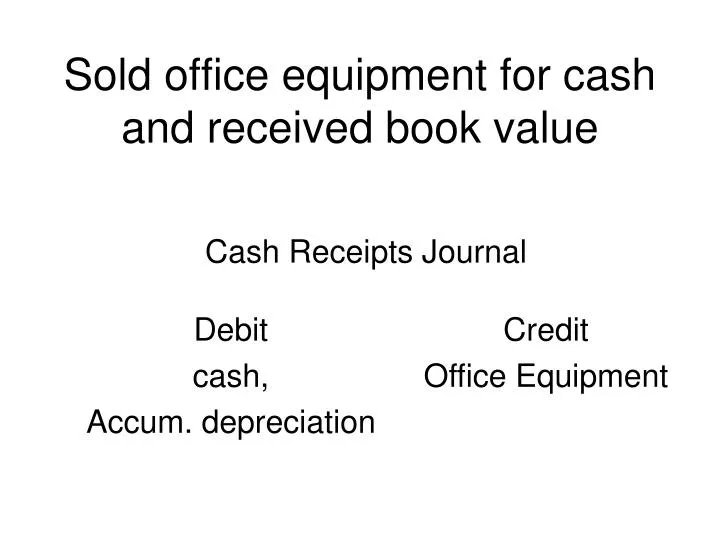

Sold office equipment for cash and received book value. Cash Receipts Journal. Debit cash, Accum. depreciation. Credit Office Equipment. Sold delivery equipment for more than book value. Cash Receipts Journal. Debit Cash Accum. Dep- DE. Credit Delivery Equipment

E N D

Sold office equipment for cash and received book value Cash Receipts Journal Debit cash, Accum. depreciation Credit Office Equipment

Sold delivery equipment for more than book value Cash Receipts Journal Debit Cash Accum. Dep- DE Credit Delivery Equipment Gain on Plant Asset

Wrote off past-due account of Gina Gates as uncollectible General Journal Debit Allow. for Uncollectible Accts. Credit AR/Gina Gates

Reopened Gina Gates account that had been previously written off General Journal Debit AR/Gina Gates Credit Allow. for Uncollectible Accts.

Received cash from Gina Gates for the amount due. Cash Receipts Journal Debit Cash Credit AR/Gina Gates

Sold delivery equipment for less than book value Cash Receipts Journal Credit Delivery Equipment Debit Cash Accum. Dep- DE Loss on Plant Asset

Accepted a note from Patti Day for an extension of time. General Journal Debit Notes Receivable Credit AR/Patti Day

Received cash for the maturity value of a note receivable. Cash Receipts Journal Debit Cash Credit Notes Receivable Interest Income

Joe Brothers dishonored his notes receivable. General Journal Debit AR/Joe Brothers Credit Notes Receivable Interest Income

Signed a note with the American Bank. Cash Receipts Journal Debit Cash Credit Notes Payable

Signed a note with Lawrence Supply for an extension of time. General Journal Debit AP/Lawrence Supply Credit Notes Payable

Paid cash for the maturity value of a notes payable. Cash Payments Journal Debit Notes Payable Interest Expense Credit Cash

Paid cash for semimonthly payroll less income tax, Medicare and social security. Cash Payments Journal Credit Emp. Inc. Tax Pay. Medicare Tax Pay. SS Tax Pay. Cash Debit Salary Exp.

Recorded employer payroll tax expense. General Journal Credit Medicare Tax Pay SS Tax Pay Fed. Unemploy. Tax Pay State Unemploy. Tax Pay Debit Payroll Tax Exp.

Paid cash for liability for employee income tax, Medicare, social security. Cash Payments Journal Debit Emp. Inc. Tax Pay Medicare Tax Pay SS Tax Pay Credit Cash

Paid cash for federal unemployment tax liability. Cash Payments Journal Debit Fed. Unempl. Tax Pay. Credit Cash

Paid cash for state unemployment tax liability. Cash Payments Journal Debit State Unemploy. Tax Pay Credit Cash

The board of directors declared dividends. General Journal Debit Dividends Credit Dividends Payable

Paid cash for dividends that were previously declared. Cash Payments Journal Debit Dividends Payable Credit Cash

Dissolving a partnership:received cash from sale of delivery equipment in which there was a gain. Cash Receipts Journal Debit Cash Accum. Deprec.—DE Credit Delivery Equipment Loss & Gain on Realization

Dissolving a partnership:received cash from sale of supplies in which there was a loss. Cash Receipts Journal Debit Cash Loss & Gain on Realization Credit Supplies

Dissolving a partnership:Paid cash to all creditors for amounts owed. Cash Payments Journal Debit Accounts Payable Credit Cash

Dissolving a partnership:Recorded distribution of Gain on Realization General Journal Debit Loss & Gain on Realization Credit Partner Capital Accounts

Dissolving a partnership:Recorded final distribution of remaining cash to partners. Cash Payments Journal Debit Partner Capital Accounts Credit Cash

Recorded international cash sale. Cash Receipts Journal Debit Cash Credit Sales

Recorded a time draft receivable for an international sale. General Journal Debit Time Draft Receivable Credit Sales

Received cash for the value of the time draft receivable. Cash Receipts Journal Debit Cash Credit Time Draft Receivable

Recorded Internet credit card sales. Cash Receipts Journal Debit Cash Credit Sales

Recorded adjusting entry for uncollectible accounts expense. Note: all adjusting, closing and reversing entries are in the general journal. Debit Uncollectible Accts. Exp. Credit Allow. for Uncollectible Accts.

Recorded adjusting entry for estimated depreciation. Debit Depreciation Exp. Credit Accumulated Depreciation

Recorded adjusting entry for increase to merchandise inventory Debit Merchandise Inv. Credit Income Summary

Recorded adjusting entry for Prepaid Insurance Debit Insurance Exp. Credit Prepaid Insurance

Recorded adjusting entry for supplies. Debit Supplies Exp. Credit Supplies

Recorded adjusting entry for accrued interest income. Debit Interest Receivable Credit Interest Income

Recorded adjusting entry for accrued interest expense. Debit Interest Expense Credit Interest Payable

Recorded adjusting entry for Federal Income Tax Expense Debit Federal Income Tax Expense Credit Federal Income Tax Payable

Close the sales account. Debit Sales Credit Income Summary

Close the purchases account. Debit Income Summary Credit Purchases

Close the rent expense account. Debit Income Summary Credit Rent Expense

Close purchases discount account. Debit Purchases Discount Credit Income Summary

Close the sales returns and allowances account. Debit Income Summary Credit Sales Ret. & Allow.

Close Income Summary for corporation (net income). Debit Income Summary Credit Retained Earnings

Close dividends. Debit Retained Earnings Credit Dividends

Reversing entry for accrued interest expense. Debit Interest Payable Credit Interest Expense

Reversing entry for accrued interest income. Debit Interest Income Credit Interest Receivable