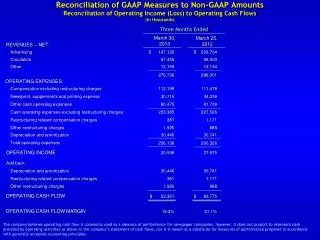

Download

1 / 33

560 likes | 1.51k Vues

Airport commercial revenues . Dr. Romano Pagliari Senior Lecturer, Cranfield University 8 December 2010. What are commercial revenues?. Airports can also generate revenues from non-airline sources. This is known as “commercial” or “non-aeronautical”

E N D

Airport commercial revenues Dr. Romano Pagliari Senior Lecturer, Cranfield University 8 December 2010

What are commercial revenues? • Airports can also generate revenues from non-airline sources. This is known as “commercial” or “non-aeronautical” • Development of commercial activities allows airports to spread their business risk. • Commercial activities are very profitable for airports • Competition with downtown and off-airport operators means that airport commercial services are not subject to economic regulation • As traffic rises – the % of revenue from commercial services should also increase – profitability increases. • Commercial revenues used to subsidise lower aeronautical charges

Who manages commercial revenues? • At most airports terminal commercial facilities are managed by third-party operators who have a concession to trade at the airport for a fixed period. • Duty-free / retail (e.g. World Duty-free, Gebr. Heinenman) • Food and beverage (Autogrill, SSP) • Advertising (advertising companies e.g. JC Decaux) • Usually one duty-free or F&B operator has concession for whole airport • Also individual retailers will have a concession contract with the airport • Third party operators have advantages over direct airport management • Knowledge and experience • Buying power • Some major airports manage some of their commercial activities directly • Dubai, Malaysian Airports, Amsterdam • Car parking and real estate are normally managed directly by the airport

Commercial revenue segmental information Revenue data and profit margin to BAA from selected non-aeronautical activities 2005/6 Source: Competition Commission

Commercial revenue segmental information Revenue data from selected non-aeronautical activities to Zurich airport 2009 Source: Zurich Airport Annual Report 2009

Terminal retail / F&B fundamentals • The market for airport retail / F&B can include: • Passengers • Meeters and greeters • Staff employed in the airport (airline, airport, others) • Local population / shoppers • Only passengers can access airside retail • Passenger’s primary purpose in an airport is to fly – shopping is secondary • Shops / retail units face a very different trading environment from city centres or “downtown” • Airport’s main objective when working with the operators, should be to maximise sales. • Levels of sales are driven by a number of factors

Factors that affect terminal sales • Traffic • Dwell Time • Psychology • Regulations • Terminal design / unit location • Retail / F&B mix • Contracts • Success of operator

Factors that affect terminal sales Average retail gross sales per passenger selection of airports Source: Airport Commercial Revenue Study 2008-9

Traffic and terminal sales • Volume of traffic – increasing returns to scope • Mix of traffic (short-haul v long-haul) • Direction of traffic (residents v non-residents) • Journey purpose (business vs leisure) • Nationality • Socio-economic group

Traffic and terminal sales Top 10 and Bottom 10 Retail spending worthiness of various nationalities at Frankfurt 2007 (Index) Bottom 10 Top 10 Source: Dirk Klann Cranfield PhD thesis

Dwell time and terminal sales • Defined as the amount of time passengers have available to spend in the commercial area • The longer the dwell-time the higher the spend • Influenced by control processes on departure • Check-in • Passport control for international departures • Passenger security check • Check-in • Time depends on airline / handling agent check-in processing • Cost of check-in desk rental

Dwell time and retail sales • Some states have passport control on departures • Most airports have one centralised security search area located between landside and airside areas • More cost-effective for the airport • Risk of long queues • Some airports have decentralised security search points located in pier or departure gate areas • More costly for the airport – complicated security staff scheduling • Shorter queues • Dwell-time affected by airline departure processing

Psychology and terminal sales • High level of impulse purchases in airports • Anxiety, anticipation & excitement key psychological states in passengers • Customers may be stressed • Time pressures • Young children • Queuing at control points • Direct relationship between stress / anxiety and spend • Airports can influence psychology through terminal design

Regulations and terminal sales • Duty and tax-free allowances set by government • Low cost airline one bag rule • Local planning regulations • Sunday trading regulations • Security regulations (EU rules) • Government guidelines / influence on tendering / contracts process • Government sanctioned monopolies

Terminal design and terminal retail • Location of sales units so that they are visible to passengers • One terminal to ensure that all passengers are exposed to one retail / F&B zone • Domestic and international passengers should have access to same airside retail / F&B zone • Orientation zone located between security and airside retail / F&B zone • Walk through stores are very successful • Focus on departures rather than arrivals • Traditionally limited opportunities for arrival retail / F&B as passengers anxious to leave airport – new developments in duty-free arrivals

Terminal design and terminal retail • F&B will occupy largest % of total commercial space (up to 50%) • 100 to 250m2 • Duty-free shops also occupy a large % of retail space • Over 300m2 • Other retail • Up to 100m2 • Books / magazines • 150m2 • Foreign exchange • 502

Terminal design and terminal retail Airside v landside

Terminal design and terminal retail • Location of Duty-free, F&B and other retail very important • Most passengers when airside will look for somewhere to eat and or buy newspaper • Profits to the airport from Duty-free much greater than F&B and newspapers • Duty-free shop should be before F&B and news • Business class lounges should be located beyond Duty-free / retail area not before • Too much seating will encourage immobility • Too little seating and passengers may sit for long periods in F&B area

Terminal design and terminal retail Airside departures retail area – Oslo Gardermoen

Terminal design and terminal retail Airside departures retail area – Heathrow Terminal 3

Retail / F&B mix Average sales penetration (% of passengers who buy) rate by product segment selected airports (2008/9) Source: Airport Commercial Revenue Study 2008/9

Retail / F&B mix % of retail space by activity (2008/9) - Sample of airports Source: Airport Commercial Revenue Study 2008/9

Retail / F&B mix • What type of retail / F&B should an airport have? • Depends on characteristics of customers – mix based on market research • Duty-free operators will stock global / regional branded goods • F&B operators will have franchise agreements with major brands (McDonalds, Starbucks) • F&B operators will also develop local airport offers • Global brands more familiar / recognised by all customers • Especially F&B • Regional / local brands less familiar to non-residents • works better in retail / speciality retail

Contracts • Terminal commercial shops managed by operators under a concession agreement • Concession agreement features: • % of sales turnover paid to the airport • Minimum guaranteed level of income to airport • Contracts for between 5 to 10 years • At some airports operators also pay space rental • Concession contracts awarded through invitation to tender • Operator that promises the highest % wins the contract • % different for each product • Typical % airports receive from different types of retail activity? • Duty-free @ 30% • Speciality retail @20% • Food & Beverage @17% • Bureau de change @3%

Contracts • Problem of over-bidding by operators • High % and 100% MAG • Operator unable to meet sales commitments / poor performance • Operator offered higher % than more competent rival bidders • Evaluation of bids should also include technical appraisals of bidding operator • If airports have deep knowledge of retail then possible for them to accurately estimate likely sales and a sustainable % for the operator • Airport sets the % • Operators bid on technical aspects only (marketing, product, track record) • Airports can innovate on concession contract by lowering the % at high sales volumes to incentivise the operator • Length of contract linked to level of investment required by the retailer • F&B @ 7- 10 years • Duty-free and speciality retail @5 years

Contracts • If the contract is too short the retailer will not have enough time to develop the business. • If the contract is too long, the airport authority will lose: • Boost in revenue that comes with regular competitive tendering • Opportunity to capture new and profitable retail offers / trends • Pricing / value for money of F&B is crucial as it may influence sales penetration on Duty-free where margins to the airport authority are higher • Monitoring of retailer performance • Check prices with “downtown” / “high street” • Regular market research on passenger / customer experience of different retailers • Service level agreements should be included in concession contracts

Car parking Car parking revenue as a % of total commercial • Car parking a significant source of revenue for airports • Demand for car parking driven by a number of factors • Airport passenger traffic profile • Location of the airport in relation to catchment area • Convenience • Availability, quality and price of public transport • More airports under pressure to encourage more use of public transport • Many passengers can make use of friends / family drop-off and pick-up • Most airports offer short stay (up to 24-48 hours) and long-stay car parking products (other levels can also be introduced – medium stay and premium valet parking)

Car parking • Charges based on a variety of factors: • Location within airport site • Space available (demand and supply conditions) • Public transport prices • Competition from other car park operators • Higher charges for short stay parking (close to terminal) – used by business passengers • Lower charges for long stay parking (further away from terminal) • Used by leisure passengers • Competition from other car park operators (BAA has 70% share of total LHR parking spaces) • Need for bus transfer to / from terminal

Car parking • Increased use of on-line advanced booking / internet sales / pre-book • Internet sales channel • Allows airport to target new customers • Sell space to online car parking sales agencies • Vary prices to compete with off-airport operators • Used mainly by leisure passengers for long stay • 10 to 30% is paid in commission to online car parking operators

Advertising • Airports can be attractive advertising sites – (especially for premium brands) • Depends on: • Volume and characteristics of passengers • Architecture of airport • Quality of Media • General economic conditions • Airports generate €0.30 to €1 per passenger in advertising income. (BAA = €0.35), (Fraport = €0.51), (Amsterdam = €0.29) • Airports normally receive 70% to 80% of advertising sales – the rest goes to agency

Small regional airports • Limited traffic volume and mix makes it difficult to develop terminal retail • In the terminal there is scope for limited F&B, news and car hire • Focus of most retail / F&B on landside as airside may not sustain enough business • Few major global operators will be attracted to small regional airports – likely partners would be local, regional or national operators • Concession fees and space rental would be much lower than that achieved at larger international airports • Potential to exploit car parking revenue opportunities • Possible property development opportunities could be non-airport related activity (industrial parks)