Mastering NPV and Discounted Cash Flows: Key Formulas and Financial Decisions

Learn the Mathematics of the Time Value of Money: discover how to determine NPV based on cash flow size, timing, and risk. The text includes examples of compounding, discounting, and simplifications, as well as practical financial decision-making strategies. This guide also covers various compounding periods, effective interest rates, and scenarios involving annuities and growing perpetuities. Gain insights into calculating the present and future value of cash flows, making informed investment decisions, and maximizing returns over time.

Mastering NPV and Discounted Cash Flows: Key Formulas and Financial Decisions

E N D

Presentation Transcript

NET PRESENT VALUE • MATHEMATICS OF THE TIME VALUE OF MONEY • NPV DEPENDS UPON THE SIZE, TIMING AND RISKINESS OF EXPECTED CASH FLOWS • 3 WAYS TO DETERMINE NPV: • FINANCIAL CALCULATOR • FORMULAS • TIME VALUE FACTOR TABLES

A Recipe for Financial Decision Makers • 1. Identify the SIZE and TIMING of all relevant cash flows on a time line. • 2. Identify the RISKINESS of the cash flows to determine the appropriate discount rate. • 3. Find NPV by discounting the cash flows at the appropriate discount rate. • 4. Compare the value of competing cash flow streams at the same point in time.

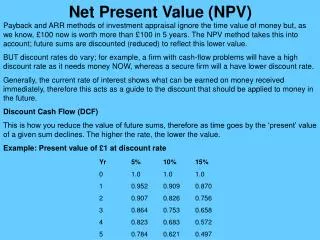

The Mathematics of Discounted Cash Flows • Compounding • Suppose we invest £1 at 9% for 2 years: 0 1 2 £1.00 £1.09 £1.1881 Future value = £1 ´ 1.09 ´ 1.09 = £1(1.09)2= £1.1881 Discounting Suppose we receive £1 discounted at 9% in 2 years: 0 1 2 £1.00 £0.917 £0.842 Slide T 4-2

–£1,000 £500 £700 0 1 2 -£1,000 £500 £700 0 1 2 Compounding Periods(first part) Annual Compounding At a discount rate of r = 9%: NPV = -£1,000 + £500/1.09 + £700/(1.09)2 = £47.89 • Semiannual Compounding • At a stated annual interest rate of 9% compounded semi-annually, the periodic discount rate is (9%/year) ¸ (2 periods/year) = 4.5% per six-month period: • NPV = -£1,000 + £500/(1.045) + £700/(1.045)2 = £44.86 • Effective annual interestrate = [1 + (r /m )] m – 1 • = [1 + (.09/2)] 2 – 1 = 9.2025% per year, • where m = 2 is the number of compounding periods per year. Slide T4-3a

EFFECTIVE ANNUAL INTEREST RATES • EAR = (1 + r/m))m -1 • Suppose that a cash flow stream of -£1,000, £500, and £700 is discounted at 9% compounded daily over a 2-year period. What is the NPV? • NPV = -£1,000 + £500/(1 + (.09/365))365 + £700/(1 + (.09/365))365 - 1 = £44.86 • EAR = (1 + .09/365))365 -1 = 9.42%

Example –£1,000 £500 £700 r = 9% 0 1 2 Future value = –£1,000(e.09 ´ 2) + £500(e .09) + £700 = –£1,197.28 + £547.09 + £700 = £49.87 Present value = –£1,000 + £500(e-.0 9) + £700(e-.09 ´ 2) = –£1,000 + £456.96 + £584.69 = £41.65 Verification £49.87 (e-.09 ´ 2) = £41.65 Compounding Periods(final part) • Continuous Compounding (e@ 2.718) • Future value = C0(erT ) • Present value = CT(e-rT ) • C0CT • 0 1 2 T-1 T … Slide T4-3b

… … Simplifications(first part) • Perpetuity: £100 per period forever discounted at 10% per period • C C C • 0 1 2 3 • PV = C/r = £100/.10 = £1,000 • Growing perpetuity: £100 received at time t = 1, growing at 2% per period forever and discounted at 10% per period • C C(1 + g) C(1 + g) 2 • 0 1 2 3 • PV = C/(r –g ) = £100/(.10 – .02) = £1,250 Slide T4-4a

Simplifications(second part) • Annuity: £50,000 per period for T = 20 periods • C C C C • 0 1 2 T-1 T • This cash flow stream is equivalent to • C C C C C • minus • 0 1 2 3 T T + 1 T + 2 • so that … … … [ ] ( ) ( ) 20 ( ) = £50 , 000 / . 1 ´ 1 - 1 / 1 . 1 = £ 425 , 678 Slide T4-4b

Simplifications(third part) • Growing Annuity: £50,000 growing at 2% per period for T = 20 periods and discounted at 10% per period • C C(1 + g) C(1 + g)2 C(1 + g)T-1 • 0 1 2 3 T • This cash flow stream is equivalent to • C C(1 + g) C(1 + g)2 • 0 1 2 3 • C(1 + g)TC(1 + g)T+1C(1 + g)T+2 • minus • TT + 1 T + 2 T + 3 … … … Slide T4-4c

Simplifications(final part) • so that Slide T4-4d

A Net Present Value Problem • What is the value of a 10-year annuity that pays £300 a year (at year- end) if the annuity’s first cash flow starts at the end of year 6 and the interest rate is 15% for years 1 through 5 and 10% thereafter? • 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 • 300 300 300 • • • • • • 300 • . • . • . Slide T4-5

TVM Problem • Your son just turned 5 today. You plan to start saving for his college education by making equal semiannual deposits in an investment account that pays a stated annual rate of 9.1% compounded semiannually with the first deposit to be made 6 months hence. You want to provide £24,000 per year for 4 years beginning when he is 19 years old. How much money should you deposits every six months until your son turns 18?

TVM Problem • You are 30 years old and wish to provide for your old age. Suppose you invest £5000 per year at an effective rate of return of 9% per year for the next 30 years, with the first deposit beginning one year hence. Beginning at age 61 you will tour the world for five years and will need £X per year at the start of each year. After you return to the U.S., you will withdraw £30,000 per year for the next 15 years. Assuming that the 9% return remains constant, what is the maximum £X you can consume each year during your world tour?