Download

1 / 7

80 likes | 100 Vues

"In this Article, we will discuss about concept of 'Updated Return' Introduced by Finance Act 2022. However, we will analyze the provisions & tim"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/income-tax/income-tax-return-including-updated-return-section-1398a.html

E N D

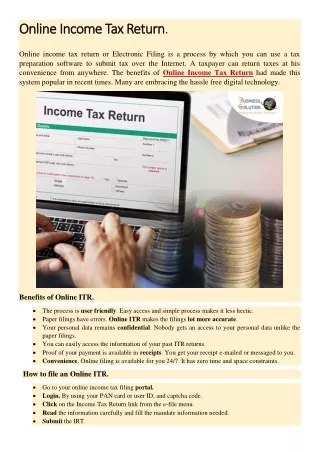

ALL ABOUT INCOME TAX RETURN INCLUDING UPDATED RETURN UNDER SECTION 139(8A) https://taxguru.in/income-tax/income-tax-return-including-updated-return-section-1398a.html In this Article, we will discuss about concept of ‘Updated Return‘ Introduced by Finance Act 2022. However, we will analyze the provisions & timelines in general to file Normal return, belated or revised return before discussing the concept of UPDATED RETURN. GENERAL PROVISIONS & TIMELINE TO FILE INCOME TAX RETURN: As per the provision of section 139(1) of the Income Tax Act 1961, the following category of the taxpayer are mandatorily required to furnish the return of Income within the due specified due date:

CATEGORY OF ASSESSEE Company Firm MANDATORY/OPTIONAL Mandatory in all cases. Mandatory in all cases. Generally, Income Tax Return is mandatory in following case: 1. If total income of the person exceeds the maximum amount not chargeable to Tax; or 2. If total sales, turnover, or gross receipts of a business exceeds INR. 60 Lakh in PY; or 3. If gross receipts of a profession exceeds INR. 10 Lakh in PY; or Any other person other than Company or Firm 4. Aggregate amount of TDS and TCS equal or more than INR. 25,000 in PY (in case of resident senior citizen the limit is INR. 50,000); or 5. Total deposit in saving bank in aggregate is equal or more than INR. 50 Lakh in PY. TIMELINE TO FILE INCOME TAX RETURN: The general timeline to furnish the return of income with tax authority is as hereunder:

CATEGORY OF ASSESSEE Any Assessee who requires to furnish report of Transfer Pricing under section 92E For – DUE DATES 30th November of Assessment Year 1. Company 31st October of Assessment Year 2. Assessee having audit requirement under Income Tax Act or any Other Law 31st July of Assessment Year Others BELTED RETURN: If an assessee has not furnished the return of Income within stipulated time, they may furnish the return of Income at any time: –At any time before 3 months prior to the end of the relevant assessment year. OR -At any time before the completion of Assessment Whichever is Earlier. FEES UNDER SECTION 234E FOR DEFAULT IN FURNISHING RETURN OF INCOME U/S 139(1): Where the return of income filed after due date notified u/s 139(1) but on or 31st December of the Assessment Year, the late fee would be payable by the Assessee as per provisions of Section 234F. The situation and applicable late fees would be as hereunder: Failure Fees / Penalty INR. 5,000 [ However, If the total income of the Assessee does not exceed INR. 5,00,000, the fee payable under this section shall not exceed INR. 1,000.] Fee for default in furnishing ROI U/S 139(1)

REVISE RETURN: If an assessee discovers any error, omission, or wrong statement in the return furnished u/s 139(1) or Section 139(4), they may furnish revised return at any point of time: – Any time before 3 Month prior to the end of the relevant assessment year. OR -Any time before the completion of Assessment- Whichever is Earlier. UPDATED RETURN: Reading the above provisions for furnishing the Return of Income, it appears that an additional time of approximately 5 months to an individual assessee, 2 months to a company/auditable assessee and 1 month to an assessee who enters an international transaction or specified domestic transaction respectively has been given for an assessment year to file belated or revised return. Since the given timeline for filing belated or revise return may not be adequate or to motivates the taxpayer towards the desired objective of voluntary tax compliance, Finance Act 2022 introduced new position under sub-section 8A of section 139 of The Income Tax Act 1961. The said amendment will come into force from 1st April 2022. As per new provision of Section 139(8A) of Act “ Any person, whether or not he has furnished a return under sub-section(1), sub-section (4) or sub-section (5), for an assessment year, may furnish an updated return of his income in respect of which he is assessable under the Act, for the previous year relevant to such assessment year, within 24 months from the end of the assessment year. Such return shall be furnished in the FORM ITR-U and manner and shall contain prescribed particulars’’. Example: For Financial year 2022-23 i.e., Assessment Year 2023-24, the assessee may file updated return till 31 st March 2026. WHEN UPDATED RETURN CANNOT BE FILED? Updated Return u/s 139(8A) cannot be filed when: Updated return will result into loss, or Updated return will result decrease in tax, or Updated return will result refund, or Updated return will result Increase in Refund WHO IS NOT ELIGIBLE FOR FILING UPDATED RETURNS: The following person shall be not eligible to file updated return If Search initiated under section 132 or Books of account, other documents or any assets has been taken into custody under section 132A in the case of such person, or If Survey has been conducted under section 133A, other than subsection(2A) of that section, in the case such person, or If A notice has been issued to the effect that any money, bullion, jewellery or valuable article or thing, seized or requisitioned under section 132 or section 132A in the case of any other person belongs to

such person, or If A notice has been issued to the effect that any books of account or documents, seized, or requisitioned under section 132 or section 132A in the case of any other person, pertain or pertains to, or any other information contained therein, relate to, such person. If an updated return has been furnished by him under the subsection (8A) of section 139 of the Act for the relevant assessment year, or If Any proceeding for assessment or reassessment or recomputation or revision of income under the Act is pending or has been completed for the relevant assessment year in his case, or The Assessing Officer has information in respect of such person for the relevant assessment year in his possession under the Prevention of Money Laundering Act, 2002 or the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 or the Prohibition of Benami Property Transactions Act, 1988 or The Smugglers and Foreign Exchange Manipulators (Forfeiture of Property) Act, 1976 and the same has been communicated to him, prior to the date of his filing of return under the proposed sub-section (8A) of section 139 of the Act, or If Information for the relevant assessment has been received under an agreement referred to in sections 90 or 90A of the Act in respect of such person and the same communicated to him, prior to the date of filing of return under the proposed sub-section (8A) of section 139 of the Act, or If Any prosecution proceedings under Chapter XXII have been initiated for the relevant assessment year in respect of such person, prior to the date of his filing of return under the proposed sub-section(8A) of section 139 of the Act, or If he is a person or belongs to a class of persons, as maybe notified by the board in this regard. MANDATORY PAYMENT OF ADDITIONAL TAX BEFORE FILING UPDATE RETURN U/S 139(8A): A new section 140B has been Introduced to provide for the tax required to be paid for opting to file a return under the proposed provisions i.e., sub-section(8A) of section 139 of the Act. Further, Section 139(9) of the Income Tax Act also amended to provide that any updated return filed u/s 139(8A) without accompanied by proof of payment of tax as computed under section 140B shall be deemed to be the defective return. The summary of the additional tax payable along with Updated Return is as hereunder: Updated Return Timing After Expiry of Time allowed u/s 139(4) or u/s 139(5) but within Twelve month from relevant assessment year; After Expiry of Twelve month from end of relevant assessment year but within Twenty-Four month from end of relevant assessment year; Additional Tax Payable Twenty-five percent of aggregate of tax and interest payable, as determined Fifty percent of aggregate of tax and interest payable, as determined MANNER TO DETERMINE ADDITIONAL TAX PAYABLE: SITUATION I – The tax payable to submit “Updated Return” will be calculated as hereunder, when no return of income filed by assessee u/s 139(1) & 139(4) of The Income Tax Act:

TIMING OF UPDATED RETURN WHERE NO ROI FURNISHED EARLIER A. Tax Payable on total income [Net of advance tax, TDS, TCS, relief u/s 89, 90, 90A & 91.] xxx B. Add: Interest on total income xxx [ u/s 234A,234B & 234C] After Expiry of Time allowed u/s 139(4) or u/s 139(5) but within Twelve month from the end of relevant assessment year C. Add: Late Fee u/s 234F xxx D. Add: Additional tax u/s 140B @25% xxx [ (A +B) *25%] Total payable xxx [A + B + C + D] A. Tax Payable on total income xxx [Net of advance tax, TDS, TCS, relief u/s 89, 90, 90A & 91.] B. Add: Interest on total income xxx [ U/s 234A,234B & 234C] After Expiry of Twelve month from end of relevant assessment year but within Twenty-Four month from the end of relevant assessment year. C. Add: Late Fee u/s 234F xxx D. Add: Additional tax u/s 140B @50% xxx [ (A +B) *50%] Total payable xxx [A + B + C + D] SITUATION II –The tax payable to submit “Updated Return” will be calculated as hereunder, when return of income already filed by assessee u/s 139(1) & 139(4) of the Income Tax Act: TIMING OF UPDATED RETURN WHERE ROI FURNISHED EARLIER U/S 139(1) or 139(4) OF THE INCOME TAX ACT 1961

A. Tax Payable on additional income xxx [Net of advance tax, TDS, TCS, relief u/s 89, 90, 90A & 91.] B. Add: Interest on total income After Expiry of Time allowed u/s 139(4) or u/s 139(5) but within Twelve month from the end of relevant assessment year xxx [ u/s 234B & 234C] C. Add: Additional tax u/s 140B @25% xxx [ (A +B) *25%] Total payable xxx [A + B + C] A. Tax Payable on additional income [Net of advance tax, TDS, TCS, relief u/s 89, 90, 90A & 91.] B. Add: interest on additional income After Expiry of Twelve month from end of relevant assessment year but within Twenty-Four month from the end of relevant assessment year. xxx [ u/s 234B & 234C] C. Add: Additional tax u/s 140B @50% xxx xxx [ (A +B) *50%] Total payable xxx [A + B + C] Recently, The Income Tax Authority has notified Form for filing “Updated Return” as form “ITR-U” on 29th April 2022 which can be download from https://taxguru.in/income-tax/cbdt-notifies-form-manner-filing- updated-return.html for reference. Apart from above, in view of the sub-section (8A) of section 139 and new section 140B, consequential amendments in section 144, section 153, section 234A and section 234B and 276CC have also has been made.