Download

1 / 3

30 likes | 52 Vues

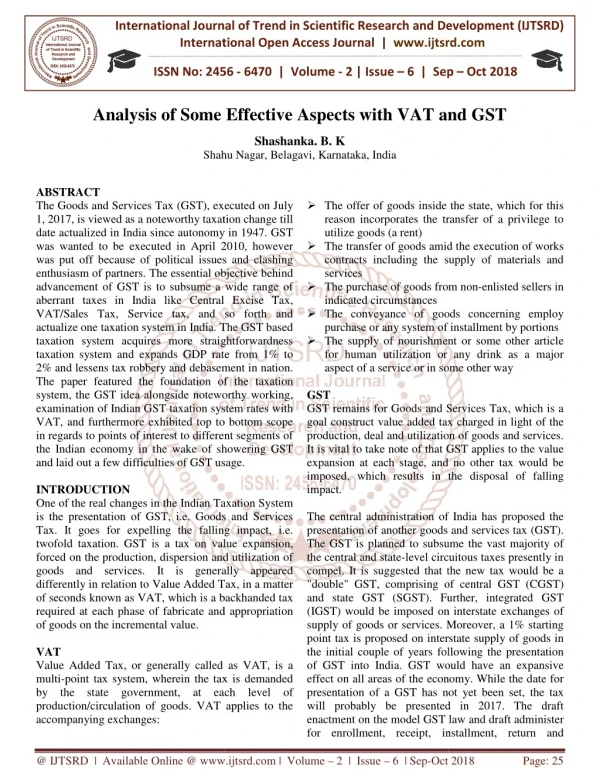

The Goods and Services Tax GST , executed on July 1, 2017, is viewed as a noteworthy taxation change till date actualized in India since autonomy in 1947. GST was wanted to be executed in April 2010, however was put off because of political issues and clashing enthusiasm of partners. The essential objective behind advancement of GST is to subsume a wide range of aberrant taxes in India like Central Excise Tax, VAT Sales Tax, Service tax, and so forth and actualize one taxation system in India. The GST based taxation system acquires more straightforwardness taxation system and expands GDP rate from 1 to 2 and lessens tax robbery and debasement in nation. The paper featured the foundation of the taxation system, the GST idea alongside noteworthy working, examination of Indian GST taxation system rates with VAT, and furthermore exhibited top to bottom scope in regards to points of interest to different segments of the Indian economy in the wake of showering GST and laid out a few difficulties of GST usage. Shashanka. B. K "Analysis of Some Effective Aspects with VAT and GST" Published in International Journal of Trend in Scientific Research and Development (ijtsrd), ISSN: 2456-6470, Volume-2 | Issue-6 , October 2018, URL: https://www.ijtsrd.com/papers/ijtsrd18354.pdf Paper URL: http://www.ijtsrd.com/economics/finance/18354/analysis-of-some-effective-aspects-with-vat-and-gst/shashanka-b-k<br>

E N D

International Journal of Trend in International Open Access Journal International Open Access Journal | www.ijtsrd.com International Journal of Trend in Scientific Research and Development (IJTSRD) Research and Development (IJTSRD) www.ijtsrd.com ISSN No: 2456 ISSN No: 2456 - 6470 | Volume - 2 | Issue – 6 | Sep | Sep – Oct 2018 Analysis of Some Effective Aspects w Analysis of Some Effective Aspects with VAT and GST nd GST Shashanka. B. K Shahu Nagar, Belagavi, Karnataka, India Shahu Nagar, Belagavi, Karnataka, India ABSTRACT The Goods and Services Tax (GST), executed on July 1, 2017, is viewed as a noteworthy taxation change till date actualized in India since autonomy in 1947. GST was wanted to be executed in April 2010, however was put off because of political issues and clashing enthusiasm of partners. The essential objective behind advancement of GST is to subsume a wide range of aberrant taxes in India like Central Excise Tax, VAT/Sales Tax, Service tax, and so forth and actualize one taxation system in India. The taxation system acquires more straightforwardness taxation system and expands GDP rate from 1% to 2% and lessens tax robbery and debasement in nation. The paper featured the foundation of the taxation system, the GST idea alongside noteworthy wo examination of Indian GST taxation system rates with VAT, and furthermore exhibited top to bottom scope in regards to points of interest to different segments of the Indian economy in the wake of showering GST and laid out a few difficulties of GST usage. INTRODUCTION One of the real changes in the Indian Taxation System is the presentation of GST, i.e. Goods and Services Tax. It goes for expelling the falling impact, i.e. twofold taxation. GST is a tax on value expansion, forced on the production, dispersion and utilization of goods and services. It is generally appeared differently in relation to Value Added Tax, in a matter of seconds known as VAT, which is a backhanded tax required at each phase of fabricate and appropriation of goods on the incremental value. VAT Value Added Tax, or generally called as VAT, is a multi-point tax system, wherein the tax is demanded by the state government, at each level of production/circulation of goods. VAT applies to the accompanying exchanges: The offer of goods inside the state, which for this reason incorporates the transfer of a privilege to ?The offer of goods inside the state, which for this reason incorporates the transfer of a privilege to utilize goods (a rent) ?The transfer of goods amid the execution of works contracts including the supply of materials and services ?The purchase of goods from non indicated circumstances ?The conveyance of goods concerning employ purchase or any system of installment by portions ?The supply of nourishment or some other article for human utilization or any drink as a major aspect of a service or in some other way GST GST remains for Goods and Services Tax, which is a goal construct value added tax charged in light of the production, deal and utilization of goods and services. It is vital to take note of that GST applies to the value expansion at each stage, and no other tax would be imposed, which results in the disposal of falling impact. The central administration of India has proposed the presentation of another goods and services tax (GST). The GST is planned to subsume the vast m the central and state-level circuitous taxes presently in compel. It is suggested that the new tax would be a "double" GST, comprising of central GST (CGST) and state GST (SGST). Further, integrated GST (IGST) would be imposed on interstate exch supply of goods or services. Moreover, a 1% starting point tax is proposed on interstate supply of goods in the initial couple of years following the presentation of GST into India. GST would have an expansive effect on all areas of the economy. W presentation of a GST has not yet been set, the tax will probably be presented in 2017. The draft enactment on the model GST law and draft administer for enrollment, receipt, installment, return and for enrollment, receipt, installment, return and The Goods and Services Tax (GST), executed on July 1, 2017, is viewed as a noteworthy taxation change till date actualized in India since autonomy in 1947. GST was wanted to be executed in April 2010, however The transfer of goods amid the execution of works contracts including the supply of materials and s and clashing enthusiasm of partners. The essential objective behind advancement of GST is to subsume a wide range of aberrant taxes in India like Central Excise Tax, VAT/Sales Tax, Service tax, and so forth and actualize one taxation system in India. The GST based taxation system acquires more straightforwardness taxation system and expands GDP rate from 1% to 2% and lessens tax robbery and debasement in nation. The paper featured the foundation of the taxation system, the GST idea alongside noteworthy working, examination of Indian GST taxation system rates with VAT, and furthermore exhibited top to bottom scope in regards to points of interest to different segments of the Indian economy in the wake of showering GST from non-enlisted sellers in The conveyance of goods concerning employ purchase or any system of installment by portions The supply of nourishment or some other article for human utilization or any drink as a major rvice or in some other way GST remains for Goods and Services Tax, which is a goal construct value added tax charged in light of the production, deal and utilization of goods and services. It is vital to take note of that GST applies to the value pansion at each stage, and no other tax would be imposed, which results in the disposal of falling usage. One of the real changes in the Indian Taxation System is the presentation of GST, i.e. Goods and Services Tax. It goes for expelling the falling impact, i.e. twofold taxation. GST is a tax on value expansion, dispersion and utilization of goods and services. It is generally appeared differently in relation to Value Added Tax, in a matter of seconds known as VAT, which is a backhanded tax required at each phase of fabricate and appropriation The central administration of India has proposed the presentation of another goods and services tax (GST). The GST is planned to subsume the vast majority of level circuitous taxes presently in compel. It is suggested that the new tax would be a "double" GST, comprising of central GST (CGST) and state GST (SGST). Further, integrated GST (IGST) would be imposed on interstate exchanges of supply of goods or services. Moreover, a 1% starting point tax is proposed on interstate supply of goods in the initial couple of years following the presentation of GST into India. GST would have an expansive effect on all areas of the economy. While the date for presentation of a GST has not yet been set, the tax will probably be presented in 2017. The draft enactment on the model GST law and draft administer Value Added Tax, or generally called as VAT, is a point tax system, wherein the tax is demanded by the state government, at each level of production/circulation of goods. VAT applies to the @ IJTSRD | Available Online @ www.ijtsrd.com www.ijtsrd.com | Volume – 2 | Issue – 6 | Sep-Oct 2018 Page: 25

International Journal of Trend in Scientific Research and International Journal of Trend in Scientific Research and Development (IJTSRD) ISSN: 2456 Development (IJTSRD) ISSN: 2456-6470 discount under GST has been made access general population. There are numerous aberrant taxes, which are subsumed after the presentation of GST in India, which are as under: ?At CGST level: Excise Duty, Service tax, additional charge and cess ?At SGST level: Octroi or Entry tax, VAT extravagance tax, additional charge and cess ?At IGST level: Central Sales Tax GST sections are settled at 5%, 12%, 18% and 28%. Some aspects amongst VAT and GST The essential contrasts amongst VAT and GST are clarified, with the assistance of followin 1.VAT or Value Added Tax is a circuitous tax, wherein tax is forced at the state level, at each phase of production and dissemination of goods and services, with credit for tax paid at the past stage. GST grows to Goods and Services Tax, which is a solitary tax, imposed on the supply of the goods and services that depends on the guideline of value expansion. 2.While VAT is collected on the offer of goods, in GST the purpose of taxation is the supply of goods and services. 3.The enlistment and installment under administration are performed disconnected, while GST is totally an online system, wherein the enrollment, recording of return and all other capacity can be performed through a typical GST gateway overseen by Goods and Services Network (GSTN). 4.When it comes to enlistment of provider, in VAT system the enrollment ends up compulsory when the turnover of the provider is past Rs. 10 Despite what might be expected, if the total turnover of the provider surpasses Rs. 20 that point he/she is required to get enlistment under GST. 5.VAT system is a rundown based system of taxation, wherein the dealer of the goods needs to present the arrival, toward the finish of the specific time frame. Alternately, GST is an exchange based taxation system. 6.In instance of the VAT, the merchant state gathers the income, though, in GST, the accumulation of income is finished by the customer state. 7.In VAT system, the maker of excisable items is charged extract obligation on its production and VAT on intra-state sales, which causes twofold discount under GST has been made accessible to the taxation. Then again, extract obligation is subsumed in GST, thus there are no odds of twofold taxation on such things. 8.Under VAT system, input tax credit can't be benefited, if there should be an occurrence of interstate sales. For example: Suppose, on the produce of material, central extract obligation (CENVAT) is required and VAT is forced on its deal inside the state. Albeit both CENVAT and VAT both are a value-added tax however set off isn't conceivable on the grounds that they CENVAT is required by the central government, and State Government forces VAT. Not at all like, GST depends on the guideline, 'one country one tax', so input tax credit is accessible for the interstate sales. LITERATURE REVIEW Kautilya`sArthasastra: His works state that the taxes are often perceived to be a measure for raising resources for the government. In the primitive barter economies of the medieval period in Europe and even in ancient India, the primary objective of taxation was to raise resource MukhopadhyaySukumar (2005): His study reveals that Revenue growth is the most important aspect by which to judge the success of VAT in Haryana. The deemed growth of revenue estimated by the Commercial Tax Department of Haryana, however, has not taken into account a number of positive factors. As Haryana implemented VAT only in 2003, one year is too short a period to judge its efficiency from a revenue point of view. The conclusion is that the design of VAT introduced in Haryana is unexceptional NishithaGuptha (2014) in her study stated that implementation of GST in the Indian framework will lead to commercial benefits which were untouched by the VA essentially lead to economic development. Jaiprakash ( 2014) in his research study mentioned that the GST at the Central and the State level are expected to give more relief to industry, trade, agriculture and consumers through a more co coverage of input tax set-off and service tax setoff, subsuming of several taxes in the GST and phasing out of CST. SaravananVenkadasalam (2014) has analysed the post effect of the goods and service tax (GST) on the national growth on ASEAN States using Least Squares Dummy Variable Model (LSDVM) in his Squares Dummy Variable Model (LSDVM) in his taxation. Then again, extract obligation is subsumed in GST, thus there are no odds of twofold taxation on such things. Under VAT system, input tax credit can't be benefited, if there should be an occurrence of example: Suppose, on the produce of material, central extract obligation (CENVAT) is required and VAT is forced on its deal inside the state. Albeit both CENVAT and added tax however set off isn't conceivable on the grounds that they CENVAT is required by the central government, and State Government forces VAT. Not at all like, GST depends on the guideline, 'one country one tax', so input tax credit is accessible for the There are numerous aberrant taxes, which are subsumed after the presentation of GST in India, At CGST level: Excise Duty, Service tax, At SGST level: Octroi or Entry tax, VAT, extravagance tax, additional charge and cess GST sections are settled at 5%, 12%, 18% and 28%. Some aspects amongst VAT and GST The essential contrasts amongst VAT and GST are clarified, with the assistance of following focuses: VAT or Value Added Tax is a circuitous tax, wherein tax is forced at the state level, at each phase of production and dissemination of goods and services, with credit for tax paid at the past stage. GST grows to Goods and Services Tax, tax, imposed on the supply of the goods and services that depends on the orks state that the taxes are often perceived to be a measure for raising resources for the government. In the primitive barter economies of the medieval period in Europe and even in ancient India, the primary objective of taxation was to raise resource MukhopadhyaySukumar (2005): His study reveals that Revenue growth is the most important aspect by which to judge the success of VAT in Haryana. fo for the economy. While VAT is collected on the offer of goods, in GST the purpose of taxation is the supply of The enlistment and installment under VAT administration are performed disconnected, while GST is totally an online system, wherein the enrollment, recording of return and all other capacity can be performed through a typical GST gateway overseen by Goods and Services Network The deemed growth of revenue estimated by the Commercial Tax Department of Haryana, however, has not taken into account a number of positive factors. As Haryana implemented VAT only in 2003, one year is too short a period to judge its efficiency enue point of view. The conclusion is that the design of VAT introduced in Haryana is unexceptional NishithaGuptha (2014) in her study stated that implementation of GST in the Indian framework will lead to commercial benefits which were untouched by the VAT system and would essentially lead to economic development. Jaiprakash ( 2014) in his research study mentioned that the GST at the Central and the State level are expected to give more relief to industry, trade, agriculture and consumers through a more comprehensive and wider off and service tax setoff, subsuming of several taxes in the GST and phasing comes to enlistment of provider, in VAT system the enrollment ends up compulsory when of the provider is past Rs. 10lakhs. Despite what might be expected, if the total f the provider surpasses Rs. 20lakhs, at uired to get enlistment VAT system is a rundown based system of taxation, wherein the dealer of the goods needs to present the arrival, toward the finish of the specific time frame. Alternately, GST is an tance of the VAT, the merchant state gathers the income, though, in GST, the accumulation of income is finished by the customer state. In VAT system, the maker of excisable items is charged extract obligation on its production and SaravananVenkadasalam (2014) has analysed the post effect of the goods and service tax (GST) on the on ASEAN States using Least , which causes twofold @ IJTSRD | Available Online @ www.ijtsrd.com www.ijtsrd.com | Volume – 2 | Issue – 6 | Sep-Oct 2018 Page: 26

International Journal of Trend in Scientific Research and International Journal of Trend in Scientific Research and Development (IJTSRD) ISSN: 2456 Development (IJTSRD) ISSN: 2456-6470 research paper. He stated that seven of the ten ASEAN nations are already implementing the GST. He also suggested that the household final consumption expenditure and general governmen consumption expenditure are positively significantly related to the gross domestic product as required and support the economic theories. But the effect of the post GST differs in countries. RESEARCH METHODOLOGY The examination depends on Secondary info gathered from different alluded books, National and global Journals, government reports, productions from different sites which concentrated on different parts of VAT and Goods and Service tax. Data Analysis Factor analysis is utilized to distin measurements fundamental the idea of VAT. The technique for factor analysis utilized here is the foremost part strategy for factor analysis with Varimax pivot. The Varimax turn is a symmetrical pivot of the factor tomahawks to amplify the change of the squared loadings of a factor (section) on every one of the factors (lines) in a factor network, which has the impact of separating the first factors by removed factor. Each factor will have a tendency to have either substantial or little stacking of variable. A varimax arrangement yields results which make it as simple as conceivable to recognize every factor with a solitary factor. This is the most well known turn choice. The Rotation really makes the yield more justifiable and is generally important to encourage the translation of factors. The fundamental significant measurements of VAT separated from Factor analysis are utilized in assist analysis in the wake of dedicating a reasonable name to them. The scores of the things with high loadings with each factor are found the middle value of and normal scores are utilized in resulting analysis. CONCLUSION Taking everything into account, we can state that GST is one tax that can be a noteworthy leap forward in the Indian taxation system. GST is an indirect tax which involves that the tax is affirmed till the last stage where it is the purchaser of the goods and services who bears the tax. The GST will substitute most other indirect taxes and synchronize the differential tax rates on mass-created goods and services. The legislature of India asserts that GST will upgrade Indian GDP by 2%. With the sanctioning of GST, Indian GDP by 2%. With the sanctioning of GST, research paper. He stated that seven of the ten ASEAN nations are already implementing the GST. He also suggested that the household final consumption expenditure and general government consumption expenditure are positively significantly related to the gross domestic product as required and support the economic theories. But the effect of the clients will have assets to spend due to bring down tax rates. It can be seen that it will totally change the m in India. Give us a chance to trust this "One country, one tax" turns out to be a distinct advantage decidedly and ends up being to be advantageous to the regular man. clients will have assets to spend due to bring down tax rates. It can be seen that it will totally change the indirect tax system in India. Give us a chance to trust this "One country, one tax" turns out to be a distinct advantage decidedly and ends up being to be advantageous to the regular man. REFERENCES 1.Empowered Committee of State Finance Ministers (2009). First Discussion Government of India, New Delhi 2.Report of Task Force on Implementation of FRBM Act, Government of India, New Delhi 3.Thirteenth Finance Commission (2009). Report of Task Force on Goods & Service Tax 4.Vasanthagopal, R., GST in India: A Big Leap in the Indirect Taxation System. International Journal of Trade, Economics and Finance, 2(2), 144–147, 2011. 5.SaravananVenkadasalam, Goods and Service Tax (GST): An ASEAN States using Least Squares Dummy Variable Model Conference on Economics, Education and Humanities (ICEEH'14) Dec. 10 (Indonesia), Pg No. 7-9 6.Nishita Gupta, Goods and Services Tax: Its implementation on Indian economy, CASIRJ Volume 5 Issue 3 [Year 9202, Pg. No.126-133 7.Neha & Sharma Manpreet, A Study on Goods and Services Tax in India, Research journal of social science & management ISSN 2251 03, Number: 10, February- 8.Dr. ShaikShakir, Dr. Sameera S. FirozSk. C., Does Goods and Services Tax (GST) Leads to Indian Economic Development? Journal of Business and Management e 2278-487X, pISSN: 2319- 12 .Ver. III (Dec. 2015), PP 01 9.Raghuram G., DeepaK. S , Goods and Services Tax: The Introduction Process, W.P. No. 2015 01 10.Panda Aurobinda and Patel Atul , The Impact of GST (Goods and Services Tax) on the Indian Tax Scene, SSRN Electronic Journal 1868621 11.Khan, M., & Shadab, N., Goods and Services Tax (GST) in India: prospect for states. Budgetary Research Review, 4(1), 38 12.http://www.indiataxes.com/Information/VAT/Intr oduction.htm 13.www.goodsandservicetax.com www.goodsandservicetax.com Empowered Committee of State Finance Ministers (2009). First Discussion Government of India, New Delhi Report of Task Force on Implementation of FRBM Act, Government of India, New Delhi Thirteenth Finance Commission (2009). Report of orce on Goods & Service Tax Vasanthagopal, R., GST in India: A Big Leap in the Indirect Taxation System. International Journal of Trade, Economics and Finance, 2(2), Paper Paper on on GST, GST, The examination depends on Secondary information gathered from different alluded books, National and global Journals, government reports, productions from different sites which concentrated on different parts of Factor analysis is utilized to distinguish the measurements fundamental the idea of VAT. The technique for factor analysis utilized here is the foremost part strategy for factor analysis with Varimax pivot. The Varimax turn is a symmetrical pivot of the factor tomahawks to amplify the change of the squared loadings of a factor (section) on every one of the factors (lines) in a factor network, which has the impact of separating the first factors by removed factor. Each factor will have a tendency to have either substantial or little stacking of a specific variable. A varimax arrangement yields results which make it as simple as conceivable to recognize every factor with a solitary factor. This is the most well- known turn choice. The Rotation really makes the SaravananVenkadasalam, Goods and Service Tax (GST): An Analysis on ASEAN States using Least Squares Dummy Variable Model Conference on Economics, Education and Humanities (ICEEH'14) Dec. 10-11, 2014 Bali Implementation Implementation of of (LSDVM)International (LSDVM)International Nishita Gupta, Goods and Services Tax: Its ndian economy, CASIRJ Volume 5 Issue 3 [Year - 2014] ISSN 2319 – & Sharma Manpreet, A Study on Goods and Research journal of social science & management ISSN 2251-1571. Volume: ly important to encourage the translation of factors. The fundamental significant measurements of VAT separated from Factor analysis are utilized in assist analysis in the wake of dedicating a reasonable name to them. The -2014 Dr. ShaikShakir, Dr. Sameera S. A, &Mr. C., Does Goods and Services Tax (GST) to Indian Economic Development?, IOSR Journal of Business and Management e-ISSN: dings with each factor are found the middle value of and normal -7668. Volume 17, Issue 12 .Ver. III (Dec. 2015), PP 01-05 S , Goods and Services Tax: The Introduction Process, W.P. No. 2015-03- Taking everything into account, we can state that GST is one tax that can be a noteworthy leap forward in the ST is an indirect tax which involves that the tax is affirmed till the last stage where it is the purchaser of the goods and services who bears the tax. The GST will substitute most other indirect taxes and synchronize the differential tax eated goods and services. The legislature of India asserts that GST will upgrade Panda Aurobinda and Patel Atul , The Impact of GST (Goods and Services Tax) on the Indian Tax Scene, SSRN Electronic Journal 1868621 Goods and Services Tax (GST) in India: prospect for states. Budgetary Research Review, 4(1), 38–64.n.d http://www.indiataxes.com/Information/VAT/Intr @ IJTSRD | Available Online @ www.ijtsrd.com www.ijtsrd.com | Volume – 2 | Issue – 6 | Sep-Oct 2018 Page: 27