Download

1 / 37

370 likes | 564 Vues

AUDITING REQUIREMENTS AND eXTENSIBLE BUSINESS REPORTING LANGUAGE (XBRL ) . By ABDULLAHI, Sani . Alhaji Ph.D Faculty of Administration, Ahmadu Bello University, Zaria. OBJECTIVE.

E N D

AUDITING REQUIREMENTS ANDeXTENSIBLE BUSINESS REPORTING LANGUAGE(XBRL) ByABDULLAHI, Sani. AlhajiPh.DFaculty of Administration, Ahmadu Bello University, Zaria

OBJECTIVE • To present an overview of Auditing, Auditing requirements and XBRL, as well as the technical aspects relevant to financial reporting and auditing.

PRESENTATION OUTLINE • Introduction • Origin, Meaning and Objectives of Auditing • Qualities and Qualifications of an Auditor • Duties and Rights of an Auditor • IFRS and XBRL • Auditing and XBRL • Challenges of XBRL • Conclusion

INTRODUCTION • Most digital representations of financial information are coded in Hypertext Markup Language (HTML) • The HTML format also does not allow for easy searching, analysis, or manipulation of information

…INTRODUCTION • Extensible Business Reporting Language (XBRL) was initiated and developed by a Professional Accountant-Charles Hoffman but well popularized by a consortium of leading financial organizations • It is designed to make financial reports easier to post on the Internet and easier to understand once they are posted

…INTRODUCTION • Investors and other financial stakeholders need accurate and reliable financial information that can be delivered promptly in order to help them make informed financial decisions. • XBRL meets these needs and is particularly important in improving the usefulness of financial information delivered via the Internet

ORIGIN • The word “audit” came from the Latin word audire, meaning “to hear”. The origin of audit dates from ancient times when the landowners allowed tenant farmers to work on their land whilst the land owners themselves did not become involved in the business of farming. • The landlords relied upon an overseer who ‘listened’ to the accounts of stewardship given by the tenants

…ORIGIN • In those days, the receipts and payments of an establishment were read to the hearing of an individual termed the AUDITOR. Consequently, the individual to whom the receipts and payments of an organization were read became known as the auditor • Auditing as it exists today was established only in the later part of the nineteenth century, born out of the complexity of modern day business world..

MEANING • The Consultative Council of the Accountancy Bodies (CCAB), defines auditing as the independent examination of, and expression of opinion on, the financial statements of an enterprise by an appointed auditor in pursuance of that appointment and in compliance with any relevant statutory obligation".

… MEANING • An audit is an independent examination of the financial statements; the auditor must be independent of those responsible for the financial statements (i.e. management). • (ii) Matters to be addressed in the audit report are dictated by the terms of the auditor(s) appointment and any relevant statutory and professional matters that the auditor is obliged to comply with.

OBJECTIVES • The primary objective of an audit under CAMA, 2004, is for an appointed auditor to express a professional opinion on the financial position of an enterprise as contained in the financial statement prepared by the management so that any person reading and using them can have faith in them

…OBJECTIVES (Secondary) • to prevent fraud and errors; • to detect any form of irregularities; • to evaluate the effectiveness or otherwise, of the internal control system within the enterprise; • to assist the management in the establishment of effective auditing system; • to advise on financial matters for efficient decision making by the management;

…OBJECTIVES (Pay offs) • Audited financial statement serves as a basis of determining the net worth of a business • To negotiate bank loan. • For the purpose of taxation. • As a basis for measuring performances by potential investors.

…OBJECTIVES (Pay offs) • As a requirement of the Nigerian stock exchange for a business that is seeking quotation. • In aid of insurance claims. • In aid of Professional Advice

QUALITIES OF AN AUDITOR • Independence In the accountancy profession independence is a concept which is fundamental. Essentially, it is an attitude of mind characterized by integrity and objectivity in approach to audit assignment.

…Qualities (CAMA rules) • An auditor shall not be an officer or employee of the client. • Auditor is normally appointed by shareholders so that he is independent of the directors. • An auditor cannot be a partner to an officer or employee of the company. • An auditor can only be removed by the shareholders as they have been appointed by them. • The auditor reports directly to the shareholders to avoid his independence being hindered.

…Qualities (CAMA rules) • The auditor has the right of access to the books and records of the company at all time. This is otherwise known as programming independence. • The auditor is not qualified under Section 387 as a receiver of the same company, in the same accounting year. • Auditor's remuneration is fixed by shareholders and not by the directors. • Auditor has a right to make representations of a reasonable length in case of an attempt to remove him from office.

…Qualities (Other Rules) • The auditor should not be involved in an assignment where he has relationship either by blood or by marriage; • Acceptance of undue hospitality constitutes a similar threat to independence; • An auditor should not accept to audit a client where he derives, the greatest proportion of his recurrent audit fees i.e. more than 15%.

…Qualities • Competence • Integrity • Objectivity • Confidentiality

Qualifications • A person shall not be qualified for appointment as an auditor of a company unless he is a member of a body of accountants in Nigeria established from time to time by an Act. • A ‘connected person’ cannot be appointed as auditor of a company

DUTIES OF AUDITORS • The primary duty of the auditors of a company is to make a report to its members on the accounts examined by them, and on every balance sheet and profit and loss account, and on all group financial statements ( S. 359 CAMA, 1990)

…Duties (Schedule 6) • Whether the auditors have obtained all the information and explanations which to their knowledge and belief were necessary for the purposes of their audit. • Whether, in their opinion, proper books of account have been kept by the company and proper returns adequate for the purposes of their audit have been received from branches not visited by them. • Whether the company's balance sheet and profit and loss account are in agreement with the books of account and returns.

…Duties (Schedule 6) • Whether in their opinion and to the best of their knowledge the accounts give the information required by the Act in the manner required. • Whether in their opinion the accounts give timely, true and fair view; In the case of the balance sheet, of the state of the company's affairs as at the end of the financial year; and In the case of the profit and loss account, of the profit or loss for the financial year.

…Duties (Fiduciary) • Auditors should exercise due care and diligence in performance of their duties. • An auditor should not delegate his authority • The auditor should not disclose confidential information or document entrusted to him during the course of his audit.

RIGHTS OF AUDITORS (CAMA) • Right of access at all times to the company's books, accounts and vouchers, (S.360). • Right to require from the company's officers such information and explanations as he thinks necessary for the performance of the auditor's duties. (S. 360) • To attend AGMs, receive all notices of and other communication relating to AGMs and be heard at any such meetings (S. 363)

…Rights Under S. 364 auditors have rights where there is a proposed resolution for their removal to: • Receive a copy of the special notice required for a resolution at a general meeting of the company to remove the auditor. • To make representations in writing of a reasonable length, and • To request that the representation be sent to members of the company.

IFRS and XBRL • IFRS are standards and interpretations adopted by the International Accounting Standards Board (IASB). They include: International Financial Reporting Standards (IFRS), International Accounting Standards (IAS) and interpretation originated by the International Reporting Standards Interpretation Committee (IFRSIC)

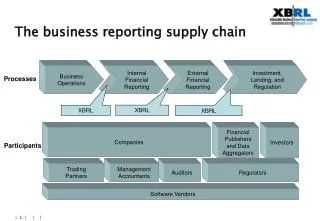

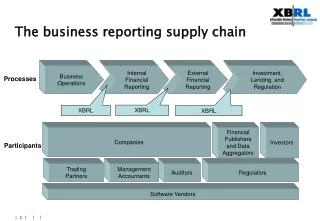

…XBRL • XBRL is a language for the electronic communication of business and financial data. • XBRL is an international computer language, for coding financial information by adding ‘tags’ to each section of financial data, allowing it to be both computer- and human-readable. • XBRL is owned by a consortium (XBRL International). This consortium comprises 642 companies who are a mixture of accountancy organizations, consultancy firms and software vendors.

…XBRL (Features) • Financial Statements (Source documents) • Taxonomies • Instance Document

AUDITING AND XBRL • The auditor may give assurance to an XBRL financial statement • XBRL Assurance is the auditor’s opinion on whether a financial statement published in XBRL format, is relevant, accurate, complete, and fairly presented.

..AUDITING AND XBRL • The auditor needs to design procedures that determine whether the specifications, taxonomy, and instance documents are appropriate for financial statements. • Adequately designed internal controls over XBRL that have been placed in operation and are operating effectively are important in ensuring the integrity and consistency of a particular taxonomy being applied in an entity.

..AUDITING AND XBRL • General control audit procedures relevant to XBRL include network operations, application development and maintenance, and access controls. Application controls relevant to XBRL address input, error correction, and output. For example, when a taxonomy is assigned, modified, or added, the auditor should validate or check an instance document against the taxonomy so to ensure the tags used are all from the taxonomy.

..AUDITING AND XBRL • When fully implemented, the risks of XBRL center on the accurate and complete mapping of the financial information and accounting data to the tags. An adequately designed and effective internal control structure for XBRL will ensure that the data retrieved represents valid and accurate transactions, has integrity, and is recognized in the proper accounting period.

..AUDITING AND XBRL The Auditor checks that: • the right standard (base) taxonomy has been used; • the custom (extension) taxonomy is complete, correct and accurate; • the source data used for reporting is reliable; • the correct and complete mapping (or tagging) of source data to taxonomy elements has occurred; • the XBRL report (instance) is technically correct and validates with the taxonomy

CHALLENGES • Resources • Software • Standards • Costs

CONCLUSION • Auditing is a legal requirement for both public companies and agencies. XBRL is the new driving revolution in the world of financial reporting with adoption in over 120 countries. There is no doubt that conversion to IFRS and adoption of XBRL in Nigeria is a huge task and a big challenge. It is a revolutionary impact requiring a great deal of decisiveness and commitment. It is in the best interest of Nigeria to adopt XBRL while implementing IFRS. A countrywide intensive capacity building programme to facilitate and sustain the process of adoption is needed as early as possible.