Download

1 / 4

50 likes | 187 Vues

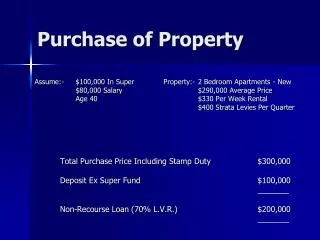

Purchase of Property. Assume:- $100,000 In Super Property:- 2 Bedroom Apartments - New $80,000 Salary $290,000 Average Price Age 40 $330 Per Week Rental $400 Strata Levies Per Quarter Total Purchase Price Including Stamp Duty $300,000 Deposit Ex Super Fund $100,000

E N D

Purchase of Property Assume:- $100,000 In Super Property:- 2 Bedroom Apartments - New $80,000 Salary $290,000 Average Price Age 40 $330 Per Week Rental $400 Strata Levies Per Quarter Total Purchase Price Including Stamp Duty $300,000 Deposit Ex Super Fund $100,000 Non-Recourse Loan (70% L.V.R.) $200,000

Holding Period (Reflected in Super Fund) Rental Income ($330 x 52 wks) 17,000 Costs & Deductions Interest ($200,000 x 6%) 12,000 Strata, Council, Water, etc. 2,000 Depreciation, Building Allowance, etc (Non-Cash) 9,000 23,000 Negative Gearing Amount $( 6,000)

Contributions To Superannuation Fund 9% Levy x $80,000 = $7,000 (Optional to S.M.S.F. or Industry Fund) Assume elected to industry fund, therefore a future buffer for cash flow anomalies that may arise. Salary or Profit Sacrifice – Say to Match Gearing Loss Amount 6,000 Negative Gearing Loss (6,000) NIL - No Contribution Tax Salary Tax Savings $6,000 x 40% - Say $2,500 Cash Surplus in Fund – Non-Cash deductions i.e. $9,000 (Cash Surplus $3,000 + Contribution $6,000) (Can be used to pay down principal loan) Therefore:- A tax deduction is achieved for the principal reduction of the bank loan

Sale of Property(Reflected in Superannuation Fund) Sale Price 350,000 Cost 300,000 Capital Gain $50,000 • Taxed at 10% • Depending on Age and Position of Fund, May be Nil Tax Therefore:- The process delivers a property that actually costs 2/3 of the purchase price purely on the differential in the tax rates of the entities used in the process.