Download

1 / 26

260 likes | 343 Vues

Gain insights on structuring and negotiating partnership terms in private equity investing. Learn about fund formation, economic considerations, tax efficiency, control, and key partnership agreement clauses. Discover strategies for capital commitment, investment limitations, management fees, key man provisions, clawbacks, distribution waterfalls, no-fault remedies, and LP/GP relationships.

E N D

Global Private EquityInvesting ConferenceStructuring Winning Partnership Terms and Conditions April 4, 2008 Glendale, AZ Heather M. Stone Partner; Head of Fund Formation

Structural Overview • Partnerships • Careful with other entities, particularly if you have non-U.S. activities (LLCs) • Multiple layers to accomplish multiple goals • Economics • Tax efficiency (U.S. and other) • Control

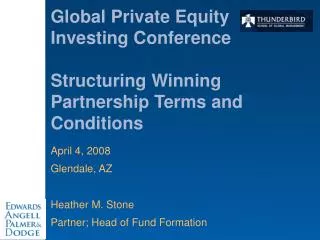

Limited Partner Limited Partner Limited Partner $ $ $ FundLimited Partnership 2% Contract Advisory Committee Management Company, LLC 20% Carried 1% ($) Class A Non-Manager Partner/Member GP/Manager General PartnerLP/LLC Class A Non-Manager Partner/Member GP/Manager Class A Non-Manager Partner/Member Class B Non-Manager Partner/Member GP/Manager • Very Basic Organizational Framework

What Are Key Terms? • Capital commitment of GP • Investment limitations • Restrictions on the GPs or Manager(s) • Management fee • Key man provisions • Clawbacks (GP, individual GPs/Managers and LPs) • Distribution waterfalls • No fault remedies, removal of GP • Confidentiality/FOIA

Capital Commitment of the GPs • How much is it? • Increasing trend • How is it paid? • Cash or “other”? • As a GP or as an LP? Addressing risks and tax efficiency concerns

Investment Limitations • Single company • Public securities – how defined? • “Foreign” – how defined? • Other pooled vehicles • Coordinate with preferred investment structures • Hostile deals • Reinvestment • Caps (during and after commitment period) • Impact of UBTI/ECI and other restrictions

Restrictions on the GPs • Cross-fund investing • Co-investments • Conflicts generally • New fund restrictions • Any new funds? • new lines of business • Percent of commitments • coordinate with reserves, expenses, suspensions and terminations

Management Fee • How much? • How calculated? • Defaults? • After end of investment period • Ramp ups and step downs • Offsets • Capital contributions, deferrals • Budgeted fees and budgets generally

Key Man Provisions • Who are key? Individuals? Groups? • What is trigger? • Active involvement • Substantially all of business time • Criminal behavior – removal a cure? • Cease to be a member • Automatic, Advisory Board vote, LP vote, combination? • What is remedy? • Suspension • Termination • Impact on fees

Clawbacks - GP • Why necessary? • Amount • Net of taxes or tax distributions? • Carry forward and back? • Multi-tiered for preferred return? • Timing • Liquidation • Interim true-ups • Several vs. joint and several; caps • Escrows, guarantees, holdbacks • Not just an LP issue anymore • Departures, retention, etc.

Clawbacks - LP • When appropriate? • Limits • Amount • Timing • after distribution is made • after fund has liquidated

Distribution Waterfalls • Amount of carry – tiers in the marketplace • Preferred returns – true or vanishing? • When does GP get carry? • Commitments vs. contributions vs. other • Venture vs. buyout • Catch-ups • Hurdles • Coordinate with escrows, holdbacks, true-ups • Allocations of expenses

No Fault Remedies – Removal of GP • Circumstances – geographic differences • Triggers – lower trigger for cause? • What is remedy? • Termination of investment period • Termination of fund • Removal? • Coordinate with • Key man provisions • Time commitment restrictions, etc.

Confidentiality; FOIA • Where are we today? • Longer and more complicated side letters • Remedies for breach • Geographic differences • Start managing disclosure now

Tips for Effective Fund Raising • START EARLY • IT TAKES LONGER THAN YOU THINK…

Tips for Effective Fund Raising • Roles and responsibilities • Terms • Managing LP expectations • Companion funds • Managing the process • Timing • Avoid the traps for the unwary

Roles and Responsibilities • Establish the team • Assign responsibilities • Terms • PPM • Contacts with LPs • Due diligence requests • Document comments

Terms • Understand “market” • How does it relates to how you operate? • Review your positioning relative to market • Understand LP’s perspective • Determine what really matters

Managing LP Expectations • Plan ahead • Establish method for allocations • Understand expectations • Pre-sell terms

Friends, Family and Entrepreneur Funds • Purpose • Expand network of resources • Deal flow • Due diligence • Significant marketing effort to do correctly • Involves everyone in the firm • Split marketing among GP “sponsors” • Administratively time consuming

Managing the Process • Database • Current investors • Prospects • Rank likely prospects • Maintain detailed notes of each contact • Allocation system • Summarize LP comments • Respond in a coordinated way • Don’t negotiate against yourself

Timing • Set realistic expectations • Allow 1-1/2 to 2 months from documents to close • Talk to investors before they read the documents • Keep promises to a minimum until you have reviewed points with counsel – don’t negotiate against yourself

Timing • THE DAY AFTER CLOSING • START PLANNING FOR THE NEXT FUND…

Traps for the Unwary • Not being conservative – timing and performance • Not reporting performance consistently • Sweeping failures under the rug • Not disclosing all relevant information on valuations (assumptions, methodology, etc.) • Using performance data from a prior fund • Making off-the-cuff predictions • Publicity

THANK YOU! • Heather M. Stone • Partner • Head of Fund Formation Group • Edwards Angell Palmer & Dodge LLP • hstone@eapdlaw.com • (617) 951-3331 • www.eapdlaw.com