Download

1 / 23

230 likes | 359 Vues

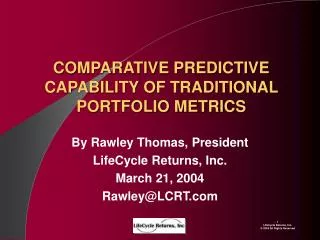

COMPARATIVE PREDICTIVE CAPABILITY OF TRADITIONAL PORTFOLIO METRICS. By Rawley Thomas, President LifeCycle Returns, Inc. March 21, 2004 Rawley@LCRT.com. Multiples P/E Continuing Operations* E/P Yield Continuing Operations* Price/Cash Flow Free Cash Flow Multiple Enterprise/EBITDA

E N D

COMPARATIVE PREDICTIVE CAPABILITY OF TRADITIONAL PORTFOLIO METRICS By Rawley Thomas, President LifeCycle Returns, Inc. March 21, 2004 Rawley@LCRT.com

Multiples P/E Continuing Operations* E/P Yield Continuing Operations* Price/Cash Flow Free Cash Flow Multiple Enterprise/EBITDA Enterprise/EBIT (1-Tax Rate) Enterprise/Capital Book Price/Equity Book Price/Sales Growth Rates EPS Basic* Cash Flow Per Share Return Measures ROE ROE before Non-Recurring ROCE ROA Cash Economic Return Size Sales Equity Market CAP Gross Investment Risk Measures Beta Debt/Capital at Market Debt/Capital at Book Foreign Sales % of Sales > 0 Dividend Annualized Dividend Yield Payout PORTFOLIO METRICS COMPARED TO LCRT FOR PREDICTIVE CAPABILITY * Multiple variants of these measures produced very similar results.

Traditional Approach Forecasts 3-10 Years of Cash Flows specific for each firm Applies Perpetuity or Multiple for Terminal Value Discounts to Present (plan valuation) Implicitly assumes the structure and parameters of the terminal valuation are robust and accurate or “plugs” the parameters to explain current price LCRT Methodology Employs onlyactual data to to empirically test robustness and accuracy of valuation models, methodologies, and parameters Enables testing hypotheses in an independent way which does not contain a look-ahead bias by knowing current price Extends the validated models to use as terminal values in traditional plan valuations using security analyst estimates or other forecasts LCRT’S RESEARCH METHODOLOGY CONTRASTS SHARPLY WITH THE TRADITIONAL VALUATION APPROACH

~ 3,000 INDUSTRIAL AND MANUFACTURING COMPANIES WITH MEDIAN TOTAL SHAREHOLDER RETURN OF -7.84% 1994-2002 DIVIDED INTO “WINNERS” AND “LOSERS” BASED ON INTRINSIC VALUE SCREENS AT FISCAL YEAR + 3 MONTHS SPLITTING DISTRIBUTION APPROXIMATELY IN HALF Total Universe Median = -7.84% N = 17,697 Company-Years 1994-2002 Panel Data “Winners” are under-valued at Fiscal Year + 3 Months and “Losers” are over-valued at Fiscal Year + 3 Months. Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million

LCRT “WINNERS” OUT-PERFORM “LOSERS” BY 12.3% (= -2.04 –(-14.38)) “Winners” Median = -2.04% N = 8,628 Company-Years 1994-2002 Panel Data “Losers” Median = -14.38% N = 8,771 Company-Years 1994-2002 Panel Data On average, the under-valued companies under-performed the S&P, but did better than the 7.8%decline in the universe. On average, the over-valued companies under-performed both the S&P, and the 7.8%decline in the universe. “Winners” are under-valued at Fiscal Year + 3 Months and “Losers” are over-valued at Fiscal Year + 3 Months. Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million

EARNING PRICE YIELD (E/P*) AND LCRT PERFORM BEST TO SEPARATE “WINNERS” AND “LOSERS”; TRADITIONAL P/E* IS POOR * Multiple variants of E/P and P/E produced very similar results. Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

MOST TRADITIONAL PORTFOLIO METRICS DO NOT SEPARATE “WINNERS” FROM “LOSERS” PARTICULARLY WELL Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

EPS AND CASH FLOW PER SHARE GROWTH PICK “WINNERS” BUT NOT “LOSERS” * Multiple variants of EPS growth produced very similar results. Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

SIZE MEASURES ARE NOT GOOD PREDICTORS Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

WITH AGGREGATE POSITIVE SPREADS OF ECONOMIC RETURNS OVER THE COST OF CAPITAL, ALL MEASURES OF FIRM RATES OF RETURN ON INVESTMENT ARE PREDICTIVE Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

TRADITIONAL RISK MEASURES FOLLOW COUNTER-INTUITIVE PREDICTIVE CAPABILITY Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

ROTATION TOWARD DIVIDEND PAYING FIRMS HAVE REWARDED INVESTORS, BUT LITTLE SPREAD EXISTS BETWEEN HIGH AND LOW YIELDS OR PAYOUTS Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

EARNING PRICE YIELD (E/P*) AND LCRT PERFORM BEST TO SEPARATE “WINNERS” AND “LOSERS”; TRADITIONAL P/E* IS POOR * Multiple variants of E/P and P/E produced very similar results. Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

MOST TRADITIONAL PORTFOLIO METRICS DO NOT SEPARATE “WINNERS” FROM “LOSERS” PARTICULARLY WELL Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

NEITHER EPS OR CASH FLOW PER SHARE GROWTH RATES SEPARATE “WINNERS” FROM “LOSERS” AS WELL AS LCRT Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

SIZE MEASURES ARE NOT GOOD PREDICTORS Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

WITH AGGREGATE POSITIVE SPREADS OF ECONOMIC RETURNS OVER THE COST OF CAPITAL, ALL MEASURES OF FIRM RATES OF RETURN ON INVESTMENT ARE PREDICTIVE Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

TRADITIONAL RISK MEASURES FOLLOW COUNTER-INTUITIVE PREDICTIVE CAPABILITY Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

ROTATION TOWARD DIVIDEND PAYING FIRMS HAVE REWARDED INVESTORS, BUT LITTLE SPREAD EXISTS BETWEEN HIGH AND LOW YIELDS OR PAYOUTS Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002, 17,697 Company-Years

COMBINING EARNING PRICE (E/P) AND LCRT SCREENS SEPARATE “WINNERS” FROM “LOSERS” BY 17.1% = (-.06-(-17.17) E/P “Losers” & LCRT “Winners” Median = -6.41% Average = 8.20% N = 1,807 Company-Years E/P “Winners” & LCRT “Winners” Median = -0.06% Average = 8.16% N = 6,898 Company-Years E/P “Losers” & LCRT “Losers” Median = -17.17% Average = -0.75% N = 6,872 Company-Years E/P “Winners” & LCRT “Losers” Median = -6.22% Average = 1.40% N = 1,870 Company-Years Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million, Panel Data from 1994-2002

COMBINING ROA AND LCRT SCREENS SEPARATE “WINNERS” FROM “LOSERS” BY 20.4% = (1.83-(-18.60) ROA “Winners” & LCRT “Winners” Median = 1.83% Average = 9.49% N = 5,837 Company-Years ROA “Losers” & LCRT “Winners” Median = -8.83% Average = 5.38% N = 2,872 Company-Years ROA “Losers” & LCRT “Losers” Median = -18.60% Average = 0.80% N = 5.616 Company-Years ROA “Winners” & LCRT “Losers” Median = -8.12% Average = -0.19% N = 3.144 Company-Years

COMBINING CER AND LCRT SCREENS SEPARATE “WINNERS” FROM “LOSERS” BY 20.4% = (2.26-(-18.01) CER “Winners” & LCRT “Winners” Median = 2.26% Average = 11.05% N = 5,558 Company-Years CER “Losers” & LCRT “Winners” Median = -7.85% Average = 2.99% N = 3,150 Company-Years CER “Winners” & LCRT “Losers” Median = -8.58% Average = -0.13% N = 3,168 Company-Years CER “Losers” & LCRT “Losers” Median = -18.01% Average = 0.08% N = 5,595 Company-Years

MOST TRADITIONAL PORTFOLIO METRICS ARE 100% ROBUST, BUT A FEW NOTABLE EXCEPTIONS EXIST, LIKE P/E AND FREE CASH FLOW MULTIPLES, BECAUSE THE METRIC LACKS MEANING WITH A NEGATIVE DENOMINATOR Equity Market CAP Robustness: % of 20,920 Company-Years with Equity Market Value Gross Investment Debt/Total Capital at Book Cash Economic Return Foreign Sales % of Sales > 0 Sales ROA ROE ROE before Non-Recurring ROCE E/P Continuing Operations Debt/Total Capital at Market Annualized Dividend Yield LCRT Price/Sales Enterprise/Capital Book Price/Equity Book Enterprise / EBITDA Cash Flow Per Share Growth Dividend Payout Price/Cash Flow Beta – Fiscal Year with Dividends Enterprise/EBIT (1-Tax Rate) EPS Growth Basic P/E Diluted Continuing Operations Sources: Financial Statements and Price Data – Simplystocks Calculations - LCRT’s Platform Constant Dollar Gross Investment > $100 Million