What is Accounting?

260 likes | 448 Vues

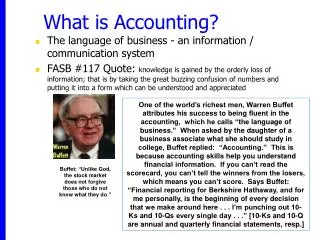

What is Accounting?. The language of business - an information / communication system FASB #117 Quote: knowledge is gained by the orderly loss of information; that is by taking the great buzzing confusion of numbers and putting it into a form which can be understood and appreciated.

What is Accounting?

E N D

Presentation Transcript

What is Accounting? • The language of business - an information / communication system • FASB #117 Quote: knowledge is gained by the orderly loss of information; that is by taking the great buzzing confusion of numbers and putting it into a form which can be understood and appreciated One of the world’s richest men, Warren Buffet attributes his success to being fluent in the accounting, which he calls “the language of business.” When asked by the daughter of a business associate what she should study in college, Buffet replied: “Accounting.” This is because accounting skills help you understand financial information. If you can’t read the scorecard, you can’t tell the winners from the losers, which means you can’t score. Says Buffet: “Financial reporting for Berkshire Hathaway, and for me personally, is the beginning of every decision that we make around here . . . I’m punching out 10-Ks and 10-Qs every single day . . .” [10-Ks and 10-Q are annual and quarterly financial statements, resp.] Buffet: “Unlike God, the stock market does not forgive those who do not know what they do.”

Importance of Providing Accurate Financial Info INFORMATION RISK IvarKreuger

Why Accounting is a Popular Career Choice Challenging Work On-the-Job Exposure Interesting People Transferrable Skills In Demand See Video The stereotype The stereotype

Did You Know that . . . • Colleges and universities graduate more accounting majors than any other undergraduate major? • In 2012 (and prior years as well), accounting was the top undergraduate degree in demand by employers? • In 2012, the average entry level salary for accounting graduates ranged $50,000-$60,000, higher than in any other field except engineering and computer science. • Women constitute 57% of those receiving bachelor degrees in accounting? • Accountants are one of the FBI’s top choice when hiring special agents. Nearly 2000 FBI agents, or about one in eight, have a background in accounting, especially forensic accounting. • The CEOs of nearly half of the largest public companies in the UK have accounting backgrounds. The percentage in the US is unknown but could be equally as high. • Arthur Blank (founder of Home Depot), Phil Knight (founder of Nike), along with many other executives, got their start as accountants?

CPA Certification • The CPA is a highly-valued designation bringing instant credibility, marketability and superior earnings • In most states, you must have bachelor degree PLUS enough college credits to total of 225 qtr credits (150 semcr), including 36 qtrcr (24 semcr) of accounting and another 36 of other business classes (economics, finance, business law). • The CPA Exam is one of the hardest professional exams. Four parts, 14 hrs long. Pass rates are about 1-in-5 for all parts in one testing window. • To get license, must have one year of experience under a CPA • Must also take an ethics exam. • Continuing Professional Education (CPE) of 40 hours per year (average) is required. • Check out WWU grad’s webpage http://www.cpareviewmaterials.com/

UNIFORM CPA EXAMINATION PASSING RATES • CPA Exam has four parts (which can be taken separately in most states): • 1. Auditing and Attestation (AUD) 4 hours; 60% MC, 40% Simulation;Courses: Auditing, Acct Info Systems • 2. Financial Accounting and Reporting (FAR) 4 hours; 60% MC, 40% Simulation;Courses: Intermediate, Advanced, Cost & Managerial, Gov’t & Nonprofit • 3. Regulation(REG) 3 hours; 60% MC, 40% Simulation;Courses: Personal & Advanced Tax, B-Law, Prof Ethics (Auditing) • 4. Business Environment and Concepts (BEC) 3 hours; 85% MC, 15% Writing: Courses: Econ, Finance, CIS, Mgmt, Acct Info Systems • Total: 14 hours The first two months of each quarter constitute a testing window. Candidates can take 1-4 parts in a testing window and have 18 months to pass all parts. For more info, go to http://www.aicpa.org/BecomeACPA/Pages/BecomeaCPA.aspx or http://www.beckercpa.com/state/index.cfm

The Accounting Profession PUBLIC ACCOUNTING Size: • local firm (Bruce J. Toews, CPA) http://www.youtube.com/watch?v=98V9lD48tTk&feature=related (Girard Pisauro) • Regional firm (Moss Adams) • National (McGladrey & Pullen) • International or Big 4 (2012) • Deloitte Touche Tohmatsu ($31.5b revenue, 193k employees) • PricewaterhouseCoopers ($29.2b revenue, 169k employees, in over 150 countries) • Ernst & Young ($22.9 revenue, 152k employees) • KPMG ($22.7 revenue, 145k employees) • https://www.thiswaytocpa.com/profession/profiles/jennifer-de-leon/#video

The Accounting Profession PUBLIC ACCOUNTING Services: • Auditing of Financial Statements • Assurance Services (e.g. Grammies, Oscars, Florida vote count) • Environmental Accounting • Forensic Accounting • Information Technology • International Advisory • Consulting • Personal Financial Planning • Tax Advisory Services

The Accounting Profession BUSINESS AND INDUSTRY Size: • small (Opp & Seibold, Contractors) • medium (Key Technology) • large (CostCo) Services: • Financial Management • Financial Reporting • Internal Auditing • Management Accounting • Tax Planning

The Accounting Profession GOVERNMENT Federal: • FBI, IRS, GAO, Treasury Dept.http://www.youtube.com/watch?v=8gVjS6LxYGs&feature=related (Lynette Williams) State & Local: • State Treasury • Bond Financing • State & Local Utilities • Counties and cities • Universities, Community Colleges, local K-12 school districts WHAT DO THEY DO? • Analyzing a school district's ability to remain viable • The propriety of expenditures for constructing prisons • The effectiveness of the workers' compensation system • The regulatory compliance of hazardous waste programs

The Accounting Profession NONPROFITS Types of Organizations: • Charities (ARC, Gates Fdn, Seattle Symphony, etc.) • Education (WWU grad Walter Froese, Whitman’s Controller; WWCC VP of Finance DavinaFogg) • Healthcare (lots of connections here) • Churches, political parties, cemeteries, museums . . . Prof: To Know True Wisdom . . . EDUCATION Become a professor and torment hopelessly befuddled groups of students with reams of useless data. Accounting professors are in high demand and paid well (mid-to-upper $100ks) The three best reasons for teaching? June, July and August But the non-physical rewards are what really makes it worthwhile – helping students realize their dreams.

WHAT IS FINANCIAL ACCOUNTING?Involves preparation/interpretation of financial statementsCovered in Principles (1st two qtrs), Intermediate & Advanced Accounting WHAT IS FINANCIAL REPORTING? Financial Statements and Auditors' Report PLUS Management Discussion & Analysis (MD&A) PLUSOther Info (pretty pictures, investor info, list of board members, other fluff & stuff, etc.) WHAT QUALITIES SHOULD FINANCIAL REPORTS HAVE? ComparableAccurate and Reliable Full-Disclosure TimelyRelevant & User Friendly Objective

WHY HAVE ACCOUNTING STANDARDS? Comparability and Efficiency – apples compared to apples Report True Economic Results (measure profits properly)Force Adequate Disclosure (warts and all)Provide Objective, Unbiased, Auditable Figures WHO SETS ACCOUNTING STANDARDS in US? SEC has ultimate authority but has usually let profession self-regulate1953-59 AICPA's Committee on Accounting Procedures (CAP) -- 51 ARBs1959-73 AICPA's Accounting Principles Board (APB) -- 31 Opinions1973-now --Private Sector: Financial Accounting Standards Board (FASB) – SFASs, (7 members, full-time, well-paid, well-represented); FASB Codification (http://asc.fasb.org/home)--Public Sector: Gov=t Accounting Standards Board (GASB)Future? IASB will establish IFRS or iGAAP.

Standard Setting Business Entities CPAs and Accounting Firms Financial Community AICPA (AcSEC) FASB Preparers (e.g., FEI) Academicians Government (SEC, IRS, other agencies) Investing Public Industry Associations Accounting standards, interpretations, and bulletins

Securities and Exchange Commission • Established by federal government • Accounting and reporting for public companies Securities Act of 1933 Securities Act of 1934 • Encouraged private standard-setting body • SEC requires public companies to adhere to GAAP • SEC Oversight and Enforcement Authority • Sarbanes-Oxley Act of 2002 (SarbOx or SOX) created the SEC’s Public Companies Accounting Oversight Board (PCAOB) which is charged with establishing auditing standards for public companies.

HOW IS A STANDARD SET? Need IdentifiedDiscussion Memorandum (DM) out for at least 60 daysPublic Response (much lobbying)Exposure Draft (ED) or rough draft out for atleast 30 days (usually longer)Public Response (again much lobbying)FASB votes (majority of 4/7 needed)

Financial Accounting Standards Board Illustration 1-3 The Due Process System of the FASB

Generally Accepted Accounting Principles GAAP Documents Most authoritative document start at the bottom

Generally Accepted Accounting Principles FASB Codification • Goal in developing the Codification is to provide in one place all the authoritative literature related to a particular topic. • Creates one level of GAAP, which is considered authoritative. • All other accounting literature is considered non-authoritative. FASB has developed the Financial Accounting Standards Board Codification Research System (CRS). CRS is an online real-time database that provides easy access to the Codification. LO 6

Generally Accepted Accounting Principles Illustration 1-5 FASB Codification Framework LO 6

Challenges Facing Financial Accounting • Nonfinancial Measurements:Ignores key performance measures used by managers, such as customer satisfaction, backorder info, product quality rates, etc. • Forward-looking Information:Financial statements primarily contain historical info, which isn’t always relevant in a fast-moving world • Soft Assets:The balance sheet ignores certain intangibles until they have been turned into cash, such as superior managers, strategic location, product domination, etc. (Which gets recorded by accountants: purchase of a paperclip or hire of a new CEO?) • Timeliness:Little real-time data is provided. This is changing. • Understandability:Complexity is overwhelming to many investors.

WHY ARE INTERNATIONAL STANDARDS IMPORTANT? Differences Between Countries Create InefficienciesGlobalization of Financial Markets Requires Cross-Border InvestmentIASB will eventually replace the FASB for public companies. Convergence is planned within the next decade. International Financial Reporting Standards (IFRS or iGAAP) will eventually replace U.S. GAAP for public companies. Private companies will likely still follow “small GAAP” set by FASB.

Principle-based Application (rules)-based

Illustration IFRS1-2 International Standard-Setting Structure

The world’s two big accounting bodies Russell Golden Chair of FASB Hans Hoogervorst, Chair of IASB FASB (Norwalk, Connecticut) http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1218220131802 IASB (London ,England) http://www.ifrs.org/The-organisation/Members-of-the-IASB/Pages/Members-of-the-IASB.aspx

International Convergence The SEC appears committed to move to IFRS, assuming that certain conditions are met. NOTE: Required date continues to change SEC Roadmap