Download

1 / 7

70 likes | 147 Vues

Learn how target-date funds can optimize retirement planning for investors. Explore asset allocations, risk analysis, and factors for fiduciary considerations to make informed decisions.

E N D

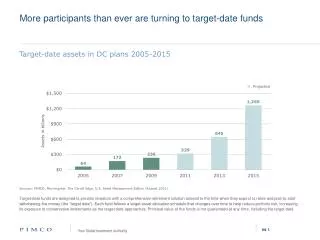

More participants than ever are turning to target-date funds Sources: PIMCO, Morningstar, The Cerulli Edge, U.S. Asset Management Edition (August 2011). Target-date funds are designed to provide investors with a comprehensive retirement solution tailored to the time when they expect to retire and plan to start withdrawing the money (the “target date”). Each fund follows a target asset allocation schedule that changes over time to help reduce portfolio risk, increasing its exposure to conservative investments as the target date approaches. Principal value of the funds is not guaranteed at any time, including the target date. Target-date assets in DC plans 2005-2015 Projected 1,265 Assets in billions 645 329 236 172 64 1

Target Date Funds Risk – Equity Glide Path Allocations

Target Date Funds Asset composition

Target Date Funds 3 year Sharpe Ratio comparisons

Target Date Funds 3 year return comparisons

Target Date Funds 3 year Standard Deviation comparisons

Target Date Funds Considerations for Fiduciaries • Demographics of your plan – average age at retirement • Does the plan offer an in-plan retirement income solution? • Do participants typically take distributions from the plan within a short window of retirement? (Most do!) • Which risk allocation is most appropriate for both plan fiduciaries and participants? • What is the upside to having higher risk profiles at retirement – if participants are going to leave the plan shortly after? • What is the composition of the underlying portfolios – are they constructed in a manner that is consistent with “prudent investors” and institutional investors? • Are there legitimate inflation hedging vehicles in the construction of the fund? • Fees of the underlying options and the overall target date solutions • Procedural Prudence vs. Substantive Prudence – Fiduciaries have a duty of care to participants – not to engage in herding • Does your TDF evaluation process rely solely on historical returns? Many score-card systems have an overweight to return data • Consider addressing TDF and QDIA specifically in the investment policy statement • Consider an RFP specific to the QDIA