Download

1 / 36

360 likes | 497 Vues

Changes in the EU Financial Regulation and the Common Provisions (Financial issues). Question and answer session. Consequences for LIFE+ Common Provisions.

E N D

Changes in the EU Financial Regulation and the Common Provisions (Financial issues) Question and answer session Platform meeting

Consequences for LIFE+ Common Provisions • Additional clause for running 2011 projects regarding interests on pre-financing (formerly art. 24) -> No need to report them as interest on PF to EC anymore but still considered as income • 2. Modifications introduced to LIFE+ 2012 Common Provisions which were already published with 2012 call for proposals -> Link to revised version and explanatory note sent with question letters • 3. Further modifications introduced in LIFE+ 2013 Common Provisions Platform meeting

Document published with the 2012 call on the LIFE website: Main changes in the Common Provisions 2012 (rev. Feb. 2013) (as compared to the text included in the Application Guides)Art 6.6 – introduces obligation for beneficiaries to inform the Commission of any activity by third parties that is likely to have a significant negative impact on the sites/species targeted in the project, and if appropriate to take measures to persuade third parties to refrain from such activities.Art 8.4. introduces stipulation that requirements of transparency and possibility of audit apply also to subcontractorsArt 18 – clarification of article on termination of the grant agreementArt 19 – clarification that confidentially obligations last for 5 years beyond the closing date of the projectArt 23.6 – introduces stipulation that claims for payments of the beneficiaries against the Commission may not be assigned to third parties.Art 24.1 – clarification on the start date for eligibility of costsArt 24.2 – clarification on the calculation of personnel costs and introductions of certain exceptions to time registration obligationsOld article 24.6 – removed; no obligation to report or repay interest on pre-financingArt 28 – payment deadlines (by the Commission) are shortenedArt 28.5 – clarifications concerning the payment suspension procedureArt 30.2 – introduces possibility to submit auditor's certification as justification for VAT non-recoverabilityArt. 32.13 – introduces stipulation that the right of access and assistance described in the rest of article 32 also apply to the Court of Auditors and OLAF.This list is not complete. Please refer to the full text for a comprehensive picture of the changes that have been introduced. Platform meeting

Modifications in Part I of the Common Provisions 2012 (legal and administrative provisions) (1/4) • References to the numbering of articles (partially new numbering) • Art. 5.5 Each AB must contributefinancially to the project and may (formerlyshall) benefitfrom the financial contribution of EC - Art. 6 Common obligations for CB and ABs • New art. 6.6 for NAT and BIO projects: communicate to EC activity by third parties likely to have negative impact on sites/species and, if appropriate, takemeasures to preventthird parties fromsuchactivities Platform meeting

Modifications in Part I of the Common Provisions 2012 (legal and administrative provisions) (2/4) - Art. 8 Subcontractors • Art. 8.1 has been reformulated by merging old art. 8.1 and 8.2 and reflecting a part of old art. 8.4. It contains the provision to award contract to lowest offer or offer with best value for money and to avoid conflict of interest in doing so. • New art. 8.4 c) with references to art. 10, 11, 19 and 32 of CP: Civil Liability, Conflict of Interest, Confidentiality and Audit by the EU Institutions now also applicable to sub-contractors. Platform meeting

Modifications in Part I of the Common Provisions 2012 (legal and administrative provisions) (3/4) Conflict of interest (economic, "family") Art 8,1 & 11: • Seperatelegalidentity • Relatedcompanies (being in controle of or beingcontroled) • Staff members • Demonstrate best value for money • Samelegalidentity (Departments) Article 26 • Excluding profit and overheads Platform meeting

Modifications in Part I of the Common Provisions 2012 (legal and administrative provisions) (4/4) - Art. 19 Confidentiality • Confidentiality obligations last for 5 years (before no time limitwasgiven) Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (1/6) - Art. 23 "Union financial contribution" (formerly Art. 24) • Old art. 24.6 and 24.7 have been deleted: no more need for specific bank account to identify funds paid by the Commission. No more recovery of interest yielded by beneficiaries on pre-financings (as of 2011 call). • Obligation to report interest as income dissapear from 2012-projects Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (2/6) - Art. 24 "Eligible costs" (formerly Art. 25) • Art. 24.1 "legal obligation to paywascontractedafter the start date of the project or after the signature of the grant agreement by the EC in case thistakes place before the projectstart date" (formerlyitwasonlyrelated to the signature of the grant agreement) Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (3/6) Provisions on personnel costs/time registration in Art 24,2 have been elaborated: • Clarification how to calculate the hourly rates • Service contracts are nowcalled "contractswithnaturalpersons" and conditions have been specified • Use of 1720 hours/year by default if reliable time registration system not available • Letter of secondment or contractual document for full time project staff (instead of time registration) • Civil servants: clarification on definition and need of contractual document/ letterof secondmentstressed • Exceptions to time registration (lessthan 2 days of work in project/month) Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (4/6) • Art 28 Payment deadlines (by the Commission) are shortened by 15 days • "Suspension periods" has been clarified further • "Interest paid by the EC on late payments" has been clarified further Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (5/6) - Art. 29 (formerly art. 30) "Statement of expenditure and income" isnowcalled "Financial statement" • Art. 29.1 "Financial statement": the EC requirements have been clarifiedfurther (new guidelines) • Art. 29.5 "Use of the Euro" The exchange rate for beneficiaries effecting purchases from non Euro countries has been specified. Platform meeting

Modifications in Part II of the Common Provisions 2012 (financial provisions) (6/6) - Art. 30 "Value addedtax" (formerly art. 31) • In case a beneficiarycannotprovide a VAT certificateemitted by the responsibleauthority, the possibility has been introduced to provide an auditor's certification as justification for VAT non-recoveribility. This justification willbeinserted in the independentfinancial audit, to beprovided by the beneficiaryat the end of the project. - Art. 32 "Audit by the EU Institutions" (formerly art. 33) • In art. 32.8 not only the European Anti-Fraud Office (OLAF) but also the Court of Auditors are given the right of access and assistance. Platform meeting

Modifications in Part I of the Common Provisions 2013 (legal and administrative provisions)(1/2) - Art. 4 Coordinatingbeneficiarynot solelylegally and financiallyresponsible to the EC anymorebut • Is the onlyintermediary for all communications betweenbeneficiaries and EC, • Provides EC with information related to any changes in legal, financial, technical, organisational or ownership situation of any of the beneficiaries • Monitors the actions as per grant agreement (GA), …/… Platform meeting

Modifications in Part I of the Common Provisions 2013 (legal and administrative provisions)(2/2) • Establishespaymentrequests and provides the EC with all the necessary reports, • Is sole recipient of payments on behalf of all beneficiaries, • Ensuresthat all appropriatepayments are made to the otherbeneficiaries in accordance with the agreementsconcludedwithABs, • Providesnecessary documents in the event of checks and audits. Platform meeting

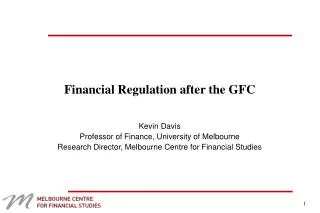

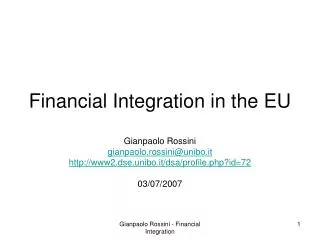

Modifications in Part II of the Common Provisions 2013 (financial provisions)(1/5) • Art. 23.4 New definition of "profit" rule: Profit = surplus of the receipts over the eligible costs of the action Reminder: Before, profit was entirely deducted from the amount to be paid, now it is shared between the EC and the beneficiary/ies, at the rate of the co-financing. Two types of receipts:i) income generated by the actionii) financial contributions specifically assigned by co-financiers to financing of eligible costs of the action reimbursed by the EC Platform meeting

Modifications in Part II of the Common Provisions 2013 (financial provisions)(2/5) receipts not to be taken into account for verification whether grant produces profit for the beneficiaries: i) financial contributions used by beneficiaries to cover costs other than the eligible costs under the GA ii) unused part of financial contributions which is not due to the donors at the end of the implementation period Platform meeting

Modifications in Part II of the Common Provisions 2013 (financial provisions)(3/5) Example (only rare cases): Platform meeting

Modifications in Part II of the Common Provisions 2013 (financial provisions)(3/5) Example (most cases): Platform meeting

Modifications in Part II of the Common Provisions 2013 (financial provisions)(5/5) - Art. 30 Value addedtax • VAT iseligibleexcept for • taxedactivities or excemptactivities, bothwith right of deduction • Activitiesengaged in as a public authority by the beneficiarywhereitis a State, regional or local governmentauthority or another body governed by public law Platform meeting

Other financial issues 2% rule: The European Court of Auditors report in 2003 on the LIFE II in paragraph 48 set out that the LIFE "administrative provisions should be amended in such a way as to exclude the possibility of financing the salaries of public servants, including cases where public bodies are involved in carrying out projects…" Temporary staff: If the staff member of the project is hired on the first day of the project, and his/her contract does not mention the end date, but he/she quits the job on the last day of the project - is that considered temporary or permanent position? Key issue – contract mentions the project? Platform meeting

Other financial issues Use of travel logs: • Proof the use of the car for the project. • Apportion costs between activities. • Short term rent of cars – probably no • Reimbursement of use of private car – probably no IF AGRESSO identify each travel to the project Platform meeting

Other financial issues Clearreference on the invoice: • It is defined to be LIFEXX NAT/YY/000ZZZ – ACRONYM • At the end of the day the costs have to belinked to the LIFE project • Number or acronym • Project code • Anythingthat links the invoice to the project area • etc Platform meeting

Other financial issues Equipment or consumables: • Just because items are depreciated 100% in the year of purchasedoes not meanitis not equipment. • Residual value • Stationarry, "off-the-shelf" product (held in stock) • Available in the cupboard or shoulditbeordered • Examples in the guidelines are clear • Equipment: laptop computer’, ‘database software (off-the-shelf or developed under sub-contract)’, ‘measurement equipment’, ‘mowing machine’, etc • Consumables: materials for experiments, animal feeding stocks, materials for dissemination, repair of durable goods given that this is not capitalised and that they are purchased for the project or used 100% for the project, etc. • For nature projectsfollow the classification of the budget. Platform meeting

Other financial issues Simplify reporting: Avoid the registration of low value invoices. Annex copies of log books Group invoices. Description allow for assessing the eligibility/relation to the project Platform meeting

Other financial issues Tender rules (1/3): How to document the selection process. When no selection or written procedure is carried out for direct contract Platform meeting

Other financial issues Tender rules (2/3): • Anslået værdi ekskl. Moms Fremgangsmåde ved indgåelse af varekøbsaftale • DKK 0 – 99.999 Ingen formkrav. • Men vær opmærksom på benyttelsen af kontrakt - særligt betalingsbetingelser, kontraktens genstand, mangler, levering og opsigelse. • MIU råder til at gøre brug af Miljøministeriets standardkontrakt og at markedsprisen kendes. Hvis markedsprisen ikke kendes, da råder MIU til at spørge minimum to leverandører. • Er du i tvivl da kontakt MIU. Platform meeting

Other financial issues Tender rules (3/3): • Anslået værdi ekskl. Moms Fremgangsmåde ved indgåelse af varekøbsaftale • DKK 100.000 – 499.999 Der indhentes minimum to skriftlige tilbud, såfremt det økonomisk og administrativt kan svare sig. Hvis der ikke indhentes minimum to skriftlige tilbud, da skal der udarbejdes referatark på sagen med indhold af økonomisk og/eller administrativ begrundelse. Der er ved disse opgaver ligeledes krav om skriftlighed og institutionen følger denne fremgangsmåde: • 1. Indhente minimum to skriftligetilbud (frit valgang.hvem der retteshenvendelsetil). Hvisdetikkeøkonomisk og/elleradministrativtkansvare sig, da kanpunkt 1 afviges. Begrundelseskrivesireferatarketpåsagen. • 2. Referatarkpåsagen med oplysningeromforventetkontraktsum mv. • 3. Udarbejde en skriftlig opgavebeskrivelse med oplysninger om behov, ønsker mv. Ved udvælgelse skal der være ligebehandling og gennemsigtighed i processen. • 4. Indgå en skriftlig aftale (gerne Miljøministeriets kontraktskabelon) Platform meeting

Other financial issues Foot note on model timesheet: Platform meeting

Other financial issues The happy FDO: Payquickly, no ineligiblecosts, no additional information • Reply on previous questions in a structuredway • Address the key issue, whichisoften the eligibility of the costs • Provide the requested documents • Providesufficientexplanations to understand the documents. Focus on the relevant invormation Platform meeting

Other financial issues Issues to considerat the beginning of projects (1/3): • Establish project codes in the analytical accounting system(s). • Establish project codes in the time registration system. • Establish a time registration system. • A short description of the time registration system, i.e. the registration and submission routines for the employees and the validation procedure for the supervisor/line manager. • Public body permanent staff must be specifically seconded to the project, i.e. ensure that such instructions are issued. Platform meeting

Other financial issues Issues to considerat the beginning of projects (2/3): • Public beneficiaries should get familiar with the applicable tender rules, i.e. when competitive price offers are and are not requested. Get familiar with what kind of documentation can be requested. Keep a short description of these rules in the project files. • Other types of beneficiaries should observe the requirement of competitive price offers for contracts above 125.000 € and the necessity to be able to provide written evidence of this procedure. I should be stressed that below this threshold best value for money still apply. Platform meeting

Other financial issues Issues to considerat the beginning of projects (3/3): • Download the financial report and the CP and distribute it to your ABs if applicable. • Provide all requested information. Add but not delete columns • Establish reporting routines for the ABs. • Ensure that supporting documents are retained in 5 years. • Obtain a declaration from the national tax authorities certifying with regard to VAT, if applicable and keep this certificate in the project file. Platform meeting

Other financial issues Issues to considerduring the projectperiod (1/2): • No blank cells. • Sufficiently detailed description to facilitate the assessment of the eligibility of the costs. • Classify the costs according to the budget. In case the budget does not give decisive guidance consult the CP. • In case it appear that durable goods are classified in other cost categories than durable goods, you should contact the Monitor. • Check that invoicing among beneficiaries, between their departments or between related companies does not take place. Platform meeting

Other financial issues Issues to considerduring the projectperiod (2/2): • You should monitor the costs and compare them to the budget on a regular basis. If you have ABs it is therefore important that they send their updated financial report to you on a regular basis. • Time worked for the project should be registered per day. • There should be a clear reference to the project on the invoice in the format LIFEXX NAT, ENV or INF/AB/000123. • Costs incurred by co-financiers or members of the cooperate groups not listed as ABs are not eligible. This apply in particular for projects where the holding company are CB in a project and where member companies of the same company group carry out the technical implementation of the project. Platform meeting

Thank you ! Platform meeting