Tax Policy Research

480 likes | 584 Vues

This literature review by Mary M. McCormick, Assistant Director for Public Services at Florida State University College of Law Research Center, examines the relationship between low income tax rates and value-added taxes (VAT) in different countries. It explores how countries with lower income tax compensation often implement VATs that considerably contribute to their overall tax revenue. The analysis draws on data from the OECD, showcasing the effectiveness of VAT in generating substantial revenues, thereby sustaining lower income tax rates. Emphasis is placed on the implications of these findings for tax policy debates.

Tax Policy Research

E N D

Presentation Transcript

Tax Policy Research Mary M. McCormick Ass’t. Director for Public Services Florida State University College of Law Research Center Fall 2008 Florida State University College of Law Research Center

Literature Review,Pre-emption Check,Academic Articles Florida State University College of Law Research Center

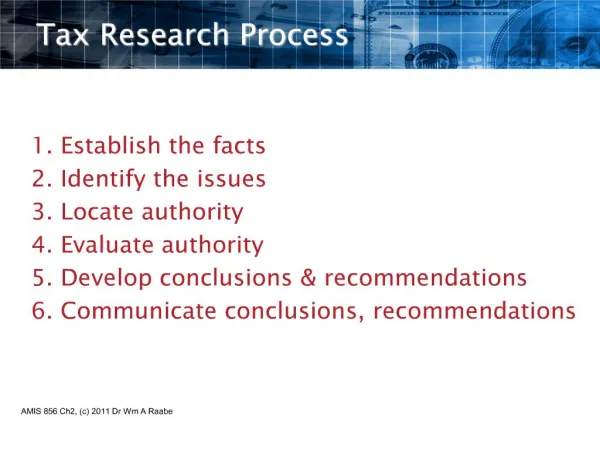

Yes to Low Income Taxes and No to the VAT??? In the Real World, Countries with Low Income Tax Rates have VATs VAT Revenues as a Percentage of Total Tax Revenues (2001) VAT Revenues as a Percentage of GDP (2005) VAT Rate (2005) Percent The VAT generates substantial revenues in the countries the WSJ praises and helps make their low income tax rates possible. Source: OECD Data (2005)

Expanding Your Research Florida State University College of Law Research Center

Is there a better citation? Burman, Leonard E., William G. Gale, and David Weiner. "The Taxation of Retirement Savings: Choosing Between Front-Loaded and Back-Loaded Options." National Tax Journal 54 No. 3 (September, 2001): 689-702. Florida State University College of Law Research Center