Download

1 / 6

60 likes | 128 Vues

Detailed breakdown of costs and net realizable value in production processes to allocate joint costs effectively.

E N D

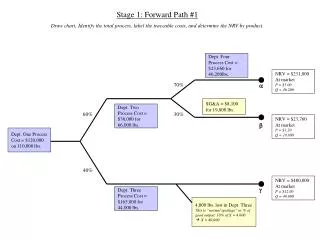

Stage 1: Forward Path #1 Draw chart, Identify the total process, label the traceable costs, and determine the NRV by product. Dept. Four Process Cost = $23,660 for 46,200lbs. NRV = $231,000 At market P = $5.00 Q = 46,200 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% NRV = $23,760 At market P = $1.20 Q = 19,800 b Dept. One Process Cost = $120,000 on 110,000 lbs. 40% NRV = $480,000 At market P = $12.00 Q = 40,000 g Dept. Three Process Cost = $165,000 for 44,000 lbs. 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000

Stage 2: Backward Path Objective: Find NRV at first split off from the NRV at Market for all the products.Why: This the the basis by which joint costs are allocated. NRV = $231,000 - $23,660 = $207,340 at this point Dept. Four Process Cost = $23,660 for 46,200lbs. NRV = $223,000 - $38,000 = $185,000 at this point NRV = $207,340 + $15,660 = $223,000 at this point NRV = $231,000 At market P = $5.00 Q = 46,200 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% NRV = $23,760 At market P = $1.20 Q = 19,800 b Dept. One Process Cost = $120,000 on 110,000 lbs. NRV = $23,760 - $8,100 = $15,660 at this point NRV = $185,000 + $315,000 = $500,000 at this point 40% NRV = $480,000 At market P = $12.00 Q = 40,000 g Dept. Three Process Cost = $165,000 for 44,000 lbs. NRV = $480,000 - $165,000 = $315,000 at this point 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000

Stage 3: Forward Path #2 Objective: Find the per unit product cost for each branch.Joint costs allocated to product g Dept. Four Process Cost = $23,660 for 46,200lbs. 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% b Dept. One Process Cost = $120,000 on 110,000 lbs. For product g: Joint Cost Allocated = 315,000/500,000 * $120,000 = $75,600 Total Product Cost = joint cost + traceable cost = $75,600 + $165,000 = $240,600 Per Unit Cost = $240,600/40,000 = $6.015/unit NRV = $185,000 + $315,000 = $500,000 at this point 40% NRV = $480,000 At market P = $12.00 Q = 40,000 C = $6.015 g Dept. Three Process Cost = $165,000 for 44,000 lbs. NRV = $480,000 - $165,000 = $315,000 at this point 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000

Stage 3: Forward Path #2 Objective: Find the per unit product cost for each branch.Joint costs allocated to product a & b where b is a by product • Assumptions: • No joint costs will be allocated to a by product • A byproduct credit should be given to the main product Dept. Four Process Cost = $23,660 for 46,200lbs. 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% NRV = $23,760 At market P = $1.20 Q = 19,800 C = $0 b Dept. One Process Cost = $120,000 on 110,000 lbs. For product b: Joint Cost Allocated = $0 Traceable Cost Allocated = $0 there is only SG&A which is a period, and not a product cost Total Product Cost = $0 Per Unit Cost = $0/unit 40% g Dept. Three Process Cost = $165,000 for 44,000 lbs. 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000

Stage 3: Forward Path #2 Objective: Find the per unit product cost for each branch.Joint costs allocated to product a & b where b is a by product Dept. Four Process Cost = $23,660 for 46,200lbs. NRV = $231,000 At market P = $5.00 Q = 46,200 C = $1.96 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% b For product a: Joint Cost Allocated = 185/500 * $120,000 = $44,000 Traceable Cost Allocated = $38,000 + $23,660 = $61,660 Less Byproduct Credit = $15,660 Total Product Cost = $44,000 + $61,560 - $15,660 = $90,400 Per Unit Cost = $90,400/46,200 = $1.96/unit Dept. One Process Cost = $120,000 on 110,000 lbs. 40% g Dept. Three Process Cost = $165,000 for 44,000 lbs. • Assumptions: • No joint costs will be allocated to a by product • A byproduct credit should be given to the main product 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000

Per Unit Costs Dept. Four Process Cost = $23,660 for 46,200lbs. NRV = $231,000 At market P = $5.00 Q = 46,200 C = $1.96 70% a SG&A = $8,100 for 19,800 lbs. Dept. Two Process Cost = $38,000 for 66,000 lbs. 60% 30% NRV = $23,760 At market P = $1.20 Q = 19,800 C = $0 b Dept. One Process Cost = $120,000 on 110,000 lbs. 40% NRV = $480,000 At market P = $12.00 Q = 40,000 C = $6.015 g Dept. Three Process Cost = $165,000 for 44,000 lbs. 4,000 lbs. lost in Dept. Three This is “normal spoilage” or % of good output: 10% of X = 4,000 X = 40,000