Skyline College

860 likes | 1.08k Vues

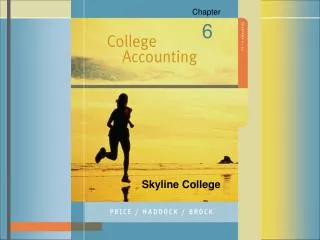

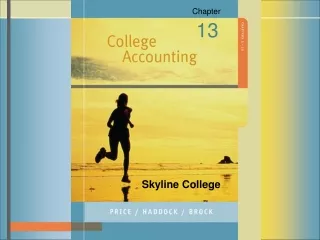

Chapter. 9. Skyline College. Journal Flow Chart. Does the transaction involve cash?. YES. NO. Was cash RECEIVED?. Was inventory PURCHASED?. NO. NO. YES. YES. Record the transaction in the CASH RECEIPTS (CRs) Journal. Record the transaction in the CASH DISBURSEMENTS

Skyline College

E N D

Presentation Transcript

Chapter 9 Skyline College

Journal Flow Chart Does the transaction involve cash? YES NO Was cash RECEIVED? Was inventory PURCHASED? NO NO YES YES Record the transaction in the CASH RECEIPTS (CRs) Journal Record the transaction in the CASH DISBURSEMENTS (CDs) Journal Record the purchase in the PURCHASES Journal (PJ) Was it a credit SALE? YES NO Use the CRs and CDs Journals to prepare the monthly Bank Reconcilation Record the Transaction in the SALES Journal (SJ) Record the Transaction In the GENERAL Journal (GJ)

A cash receipts journal is a special journal used to record and post transactions involving the receipt of cash. The Cash Receipts Journal

Cash Sales and Sales Taxes Consider the cash sales entries for January 8 in the cash receipts journal for The Style Shop.

CASH RECEIPTS JOURNAL PAGE 1 360.00 4,500.00 8 Cash Sales 4,860.00

Cash Short Over Occasionally errors occur when making change. When errors happen, the cash in the cash register is either more or less than the cash listed on the audit tape. • When cash in the register is more than the audit tape, cash is over. • When the cash in the register is less than the audit tape, cash is short.

15 Cash Sales 384.00 4,800.00 Cash Short/Over 18.00 5,166.00 Cash sales with cash short. CASH RECEIPTS JOURNAL PAGE 1 $384 + $4,800 = $5,184 Debits are not the normal balance of the Other Accounts Credit column, so the debit entry is circled.

Cash Discounts on Sales • The Style Shop does not offer cash discounts. • However, many wholesale businesses offer cash discounts to customers who pay within a certain time period. These are sales discounts. • Businesses with many sales discounts add a Sales Discounts Debit column to the cash receipts journal.

12 Investment Amos, Capital 15,000.00 15,000.00 Additional Investment by the Owner CASH RECEIPTS JOURNAL PAGE 1 The account name and amount are entered in the Other Accounts Credit section and the debit is entered in the Cash Debit column.

Cash Refund Supplies 75.00 75.00 Receipt of a Cash Refund CASH RECEIPTS JOURNAL PAGE 1 The name and amount are entered in the Other Accounts Credit section. The debit is entered in the Cash Debit column.

A promissory note is a written promise to pay a specified amount of money on a certain date. Promissory Note Sometimes promissory notes are used to replace an accounts receivable balance when the account is overdue.

$800 July 31, 20-- Six monthsAFTER DATE I PROMISE TO PAY TO THE ORDER OFThe Style Shop Eight hundred and no/100 - - - - - - - - - - - - - - - - - - - - - - - - - - DOLLARS -PAYABLE AT First Texas Bank VALUE RECEIVED with interest at 9% NO. 30 DUE January 31, 20--Stacee Fairley On July 31 The Style Shop accepted a six-month promissory note from Stacee Fairley, who owed $800 on account.

GENERAL JOURNAL Page 16 DATE DESCRIPTION POST. DEBIT CREDIT REF. 20-- July 31 Notes Receivable 800 Accounts Rec./Stacee Fairley 800 Received a 6-month, 9% note from Stacee Fairley to replace open account On July 31 The Style Shop recorded a general journal entry to increase notes receivable and to decrease accounts receivable for $800. The asset account, Notes Receivable, was debited. The Accounts Receivable account was credited.

Interest rate = 9% per year Time = six months Interest amount $800 x 9% x 6/12 = $36 P x i x t Total amount with interest = $836 ($800 + $36) Amount owed (principle) = $800

31 Collection of Notes Receivable 800.00 note/S. Fairley Interest Income 36.00 836.00 Collection of a Promissory Note and Interest CASH RECEIPTS JOURNAL PAGE 1 The note and the interest are recorded in the Other Accounts Credit section.

Posting the Cash Receipts Journal Posting the Column Totals At the end of the month, the cash receipts journal is totaled and the equality of debits and credits is proved.

The column totals are posted to the general ledger. CASH RECEIPTS JOURNAL PAGE 1 2,133 + 1,800 + 22,500+ 15,909 = 42,342

The amounts in the Other Accounts Credit section are posted. CASH RECEIPTS JOURNAL PAGE 1 The (X) indicates that the individual amounts are posted, and not the total.

Posting to the Accounts Receivable Ledger Post entries from the Accounts Receivable Credit column to the customers’ accounts in the accounts receivable subsidiary ledger daily. On January 7, $432 was posted to Roy Anderson’s account in the accounts receivable subsidiary ledger.

CASH RECEIPTS JOURNAL PAGE 1 SALES DATE DESCRIPTION POST. ACCOUNTS TAX SALES OTHER ACCOUNTS CREDIT CASH REF. RECEIVABLE PAYABLE CREDIT ACCOUNT TITLE POST. AMT. DEBIT CREDIT CREDIT REF. 20-- Jan. 7 R. Anderson 432 .00 432.00 The “CR1” indicates that the transaction appears on page 1 of the cash receipts journal. Name Roy Anderson Terms n/30 Address 8913 S. Hampton Rd, Dallas, Texas 75232-6002 DATE DESCRIPTION POST. DEBIT CREDIT BALANCE REF. 20-- Jan. 1 Balance 432.00 3 Sales Slip 1101 S1 432.00 864.00 7 CR1 432.00 432.00 31 Sales Slip 1110 S1 267.50 699.50

Advantages of the Cash Receipts Journal The cash receipts journal: • Saves time and effort when recording and posting cash receipts • Allows for the division of work among the accounting staff • Strengthens the audit trail by recording all cash receipts transactions in one place

A cash payments journal is a special journal used to record transactions involving the payment of cash. The Cash Payments Journal

Journal Flow Chart Does the transaction involve cash? YES NO Was cash RECEIVED? Was inventory PURCHASED? NO NO YES YES Record the transaction in the CASH RECEIPTS (CRs) Journal Record the transaction in the CASH DISBURSEMENTS (CDs) Journal Record the purchase in the PURCHASES Journal (PJ) Was it a credit SALE? YES NO Use the CRs and CDs Journals to prepare the monthly Bank Reconcilation Record the Transaction in the SALES Journal (SJ) Record the Transaction In the GENERAL Journal (GJ)

Payments for Expenses Businesses write checks for a variety of expenses each month. In January The Style Shop issued checks for rent, electricity, telephone service, advertising, and salaries. Consider the January 3 entry for rent expense.

20-- Jan. 3 111 January rent Rent Expense 1500 1500 The account name and amount are entered in the Other Accounts Debit section. The credit is entered in the Cash Credit column.

Payments on Account Merchandising businesses usually make numerous payments on account for goods that were purchased on credit. Consider the January 27 entry for International Apparel Mart.

27 122 International Apparel Mart 2400.00 2400.00 If there is no cash discount, the entry in the cash payments journal is a debit to Accounts Payable and a credit to Cash.

Purchases Discounts Purchases Discounts is a contra cost of goods sold account. For an example of a payment with a discount, refer to the January 13 entry for Fashion Designs.

Debit Accounts Payable for the invoice amount, $2865 Credit Purchases Discounts for the amount of the discount, $57.30. Credit Cash for the amount of cash paid, $2807.70.

Cash Purchases of Equipment and Supplies Businesses use cash to purchase equipment and other assets. On January 10 The Style Shop issued a check for store fixtures.

10 112 Store fixtures Store Equip. 2400.00 2400.00 The account name and amount appear in the Other Accounts Debit section. The credit is recorded in the Cash Credit column.

Payment of Taxes Retail businesses collect sales tax from their customers. Periodically the sales tax is remitted to the taxing authority. Consider the entry on January 11.

The Style Shop issued a check for $749 to pay the December sales tax. 11 113 Tax remittance Sales Tax Pay. 756.00 756.00 Notice that the account name and amount appear in the Other Accounts Debit section. The credit is entered in the Cash Credit column.

Cash Purchases of Merchandise Although most merchandising businesses buy their goods on credit, occasionally purchases are made for cash. Consider the January 31 entry for the purchase of goods.

Purchase of goods 31 126 Purchases 3200.00 3200.00 Cash purchases are recorded in the cash payments journal.

Freight In 175.00 175.00 Payment of “freight-in” and amount appear in the Other Accounts Debit section. The credit is in the Cash Credit column.

Cash PaymentsJournal The Style Shop issued a check for $172.80 to a customer who returned a defective item. 31 128 Cash refund Sales Ret. & Allow. 160.00 12.80 Sales Tax Payable 172.80

Payment of a Promissory Note and Interest A promissory note can be issued to settle an overdue account or to obtain goods, equipment, or other property.

GENERAL JOURNAL Page 16 DATE DESCRIPTION POST. DEBIT CREDIT REF. 20-- Aug. 2 Store Equipment 131 6,000 Notes Payable 201 6,000 Issued a 6-month, 10% note to Metroplex Equipment Company for purchase of new store fixtures On August 2, The Style Shop issued a six-month promissory note for $6,000 to purchase store fixtures from Metroplex Equipment Company. The note had an interest rate of 10 percent.

On January 31 The Style Shop issued a check for $6,300 in payment of the note ($6,000) and the interest ($300). P x i x t = interest $6,000 x 10% x 6/12 = $300

Cash Payments Journal Debit Notes Payable for $6,000 Debit Interest Expense for $300 Sales Ret. & Allow. 160.00 31 128 Cash refund Sales Tax Payable 12.80 172.80 31 129 Note paid to Metroplex Notes Payable 6000.00 Equipment Company Interest Exp. 6300.00 300.00 Credit Cash for $6,300

Posting from the Cash Payments Journal During the month, the amounts recorded in the Accounts Payable Debit column are posted to the individual accounts in the accounts payable subsidiary ledger. The amounts in the Other Accounts Debit column are also posted individually to the general ledger accounts during the month. Consider the January 3 entry in the cash payments journal that was posted to Rent Expense account.

CASH PAYMENTS JOURNAL PAGE 1 ACCOUNTS PURCH. DATE CK. EXPLANATION POST. PAYABLE OTHER ACCOUNTS DEBIT DISCOUNT CASH NO. REF. DEBIT ACCOUNT TITLE POST. AMOUNT CREDIT CREDIT REF. 20-- Jan. 3 111 January rent Rent Expense 634 1500 1500 ACCOUNTRent Expense ACCOUNT NO. 634 DATE DESCRIPTION POST. DEBIT CREDIT BALANCE REF. DEBIT CREDIT 20-- Jan. 3 CP1 1500 1500 The “CP1” indicates that the entry is recorded on page 1 of the cash payments journal.

Posting to the Accounts Payable Ledger Post entries from the Accounts Payable Debit column of the cash payments journal to the vendor accounts in the accounts payable subsidiary ledger daily. On January 13, $2,865 was posted to Fashion Designs account in the subsidiary ledger.

NameFashion DesignsTerms2/10, n/30 Address 2313 Belt Lane, Dallas, Texas, 75267-6205 DATE DESCRIPTION POST. DEBIT CREDIT BALANCE REF. 20-- Jan. 1 Balance 2,200 3 Invoice 5819,12/29/-- P1 2865 5,065 13 CP1 2,865 2,200 30 CP1 1,135 1,065 Page 303 The amount of $2,865 was posted to Fashion Designs account in the subsidiary ledger.

Advantages of the Cash Payments Journal The cash payments journal: • Saves time and effort when recording and posting cash payments • Allows for a division of labor among the accounting staff • Improves the audit trail because all cash payments are recorded in one place and listed by check number

The Petty Cash Fund Most businesses use a petty cash fund to pay for small expenditures The amount of the petty cash fund depends on the needs of the business. Usually the office manager, cashier, or assistant is in charge of the petty cash fund.

Establishing the Fund The Style Shop’s cashier is responsible for petty cash. The Style Shop wrote a $175 check to the cashier, who cashed the check and put the currency in a locked cash box.

Debit Petty Cash Fund in the other Accounts Debit section and enter the credit in the Cash Credit column.

A petty cash voucher is a form used to record the payments made from a petty cash fund. Petty Cash Voucher The person receiving the funds signs the voucher. The person who controls the petty cash fund initials the voucher.