BANK RECONCILIATION STATEMENT

330 likes | 619 Vues

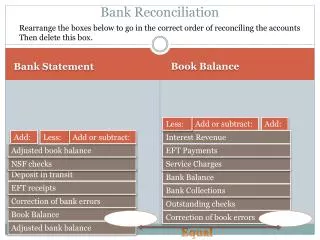

BANK RECONCILIATION STATEMENT. B.R.S. Dr P S Baliyan. BANK RECONCILIATION STATEMENT. Bank reconciliation is the process of matching and comparing figures from accounting records against those presented on a bank statement.

BANK RECONCILIATION STATEMENT

E N D

Presentation Transcript

BANK RECONCILIATION STATEMENT B.R.S Dr P S Baliyan

BANK RECONCILIATION STATEMENT • Bank reconciliation is the process of matching and comparing figures from accounting records against those presented on a bank statement. • Subtract any items which have no relation to the bank statement, the balance of the accounting ledger should reconcile (match) to the balance of the bank statement.

Reasons for difference between these two Balances: • Cheques issued but not presented for payment. • Cheques sent for collection but not collected by the bank. • Credits(deposits) made by bank for interest allowed by the bank. • Payment made by the bank-(insurance premium, bill payables etc. • Collection made by the bank. • Interest charged on bank overdraft by bank.

Reasons for difference... • Any wrong entry on the debit side of the Bank statement. • Cheques paid into bank but omitted to be entered in cash book. • Any wrong entry on the credit side of the Bank statement. • Dishonoured cheques

There are three main forms of accounts in banks….1 • Current account : No interest on deposits. Benefits: Any number of time deposit and with draw the money in a day [ no restrictions on withdrawals] Useful: Business people

There are three main forms of accounts in banks….2 • Savings account : Small rate (%) of interest • Conditions: Few withdrawals in a day up to certain limit. Useful: Employees & small saving habit peoples

There are three main forms of accounts in banks ….3 • Fixed deposit account :Good rate (%) of interest • Condition: No withdrawals up to certain period i.e., 3 ,6 or 1 year etc. • Useful: who plans for long term savings / Investments.

Terms used in banking Standing order: A firm can instruct its bank to pay regular amounts of money at stated dates to persons or other firms. Direct debit: A firm can allow creditors permission to obtain funds directly from the firm’s bank account – which allows the amounts collected to vary.

How to do basic transactions in a Bank • Opening of a bank account • Depositing the money in bank • Withdrawing the money from the bank

Know about cheque : • A cheque must be dated and must include the name of person or organization for which it has to be paid. The amount has to be written in words and figures, and must be signed by account holder. The signature must tally with specimen signature, which is being provided by the account holder while opening the account.

Bank statement or pass book • Banks will either send a periodical bank statement of the account or a give a pass book to the customer. The entries made in the statement or passbook shows the transactions made by the account holder.

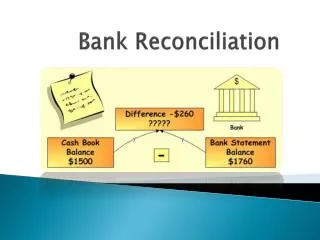

Bank reconciliation statemnt Bank Reconciliation Statement as at ***** Balance as per cash book **** Add: Unpresented cheques **** dividend collected by bank **** All direct deposit by customers **** Less:Cheques sent for collection but not yet col Bank charges Bills dishonoured Payments made by bank **** Balance as per bank statement ****

Pay to the order of: ABC Co. Cash • Coin and currency • Checking, savings, and money market accounts • Undeposited, cashier, and certified checks LO1

Readily convertible to cash • Original maturity to investor of three months or less 1 2 3 4 5 6 7 8 9 10 1 2 3 11 12 13 14 15 16 17 4 5 6 7 8 9 10 1 2 3 18 19 20 21 22 23 24 11 12 13 14 15 16 17 4 5 6 7 8 9 10 25 26 27 28 29 30 31 18 19 20 21 22 23 24 11 12 13 14 15 16 17 25 26 27 28 29 30 31 18 19 20 21 22 23 24 25 26 27 28 29 30 31 Cash Equivalents • Commercial paper • U.S. Treasury bills • Certain money market funds

Cash Management • Necessary to ensure company has neither too little nor too much cash on hand • Tools • Cash flows statement • Bank reconciliations • Petty cash funds LO2

Bank Statements Cash balance, beginning of period + = Cash balance, end of period • Canceled cheques • Direct debit • Service charges • Deposits • Customer notes and interest collected by bank • Interest earned

Example of Reconciliation Bank Statement Adjustments Balance per statement, June 30 P3,308.59 Adjusted balance, June 30 P3,233.05 Cash Account Adjustments Balance per books, June 30 P2,895.82 Adjusted balance, June 30 P3,233.05