Credit Card Services and Receivables Management

290 likes | 549 Vues

Credit Card Services and Receivables Management. FIN 292 Accounting and Finance for Entrepreneurs. Credit Card Services. Businesses prefer to sell for cash. Consumers increasingly prefer to use credit or debit cards to pay for goods and services

Credit Card Services and Receivables Management

E N D

Presentation Transcript

Credit Card Servicesand Receivables Management FIN 292 Accounting and Finance for Entrepreneurs

Credit Card Services • Businesses prefer to sell for cash. • Consumers increasingly prefer to use credit or debit cards to pay for goods and services • Startups cannot afford to grant credit directly for two reasons. • granting credit requires significant upfront capital • receivables management is costly and time consuming

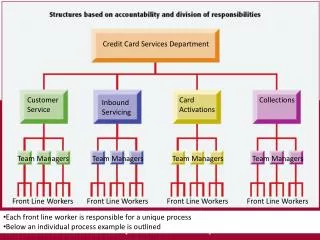

Credit Card Services • Four Parties to Each Credit Transaction • The Merchant (Seller) • The Customer (Buyer) • The Issuing Bank (Card Issuer) • The Acquiring Bank (Transaction Processor)

Credit Card Services • The Process • Buyer swipes card at the point-of-sale reader • Transaction information transmitted to the acquiring bank which verifies the information with Issuing Bank and sends back the approval to the merchant • Acquiring bank credits merchant account with payment less discount fee. • Acquiring bank receives funds from Issuer bank less an interchange fee.

Credit Card Services • Other Fees May be Imposed • Online and Phone transactions incur additional fee to cover possible chargeback costs • Chargeback: a credit to customer’s account • There is always the possibility that charge is incorrect or fraudulent – reason for CVV code

Credit Card Service Process • All credit transactions are channeled through a payment gateway • Payment Gateway verifies cardholder information and authorizes payments to merchant’s account • Sends data to card holder’s bank which then accepts or rejects transaction • If accepted, payment to merchant follows and transaction is complete.

Setting Up Credit Card Services • Two Steps Required • Setting up a Gateway account • Verification and processing of credit card transactions • Provide transaction summaries • Provide means for merchant-customer communication • Setting up a Merchant account • Receive payments – credit to merchant account

Setting Up Credit Card Services • Gateway Requirements • Comply with Payment Card Industry Data Security Standard (PCI DSS) • Incorporate a Secure Socket Layer (SSL) to encrypt and protect transaction information • Provide full eCommerce capabilities • Shopping cart • Email receipt (transaction verification record) • Support recurring payments

Caveats • Investigate before you sign a contract • Read all the fine print • Does the provider impose any additional fees? • Is there an auto-renewal feature? • Where is their call center located? • How easy is it to contact them to resolve problems?

Receivables Management • The Cash Cycle • Cash to Inventory to Sales to Receivables to Cash • Receivables a function of Credit Policy • Receivables must be financed up front • Profitability affected by collections experience • Collections experience reflects Credit Policy • Moral of the story: in WCM, everything affects everything else...

Granting Trade Credit • Credit rating agencies • Business customers = Dun $ Bradstreet • Consumers = Experian, Trans Union, Equifax • Large Corporations = Standard & Poor

Credit Instruments • Open Account • Limits impose when payments don’t arrive. • most common form of trade credit account. • Bankers’ Acceptances • Banks guarantee payment. • Goods are collateral against guarantee. • Promissory Notes • documentary evidence of amount owed + terms

Credit Policy Variables • Maximum Credit Period • How long can firm carry receivables and still be profitable? • Minimum Credit Standard • Is being warm and breathing enough? • Collection Policy • How do we deal with deadbeats?

Credit Policy Variables • Discounts • Granting discounts to encourage early payment • Advantage - reduce carry time and related expense. • Disadvantage - reduces cash inflow, some firms pay late and still take discount!

Determining Creditworthiness • Five C’s of Creditworthiness • Character - past history • Capacity - income • Capital - What the Own less What they Owe • Collateral - Reducing the risk of loss • Conditions - expectations relative to economy • Assigning relative weights and setting minimums

Collection Performance • How well are we managing A/R? • Days Sales Outstanding (DSO); • DSO = S di / n • ACP = A/R divided by Avg. Daily Credit Sales • ACP = [1/ARTO] * 360

Alternative Strategies • What can firms do if cash is slow in being received? • Factoring - selling receivables (at a discount) • with recourse • without recourse • Farfaiting - selling receivables in the international market

Cost of Carrying Receivables • Functional Relationship • CCR = DSO * ACSPD * VCR * kf • Where: DSO = days sales outstanding • ACSPD = average credit sales per day • VCR = Variable Cost Ratio • kf = cost of funds utilized

Questions and Problems • How does the credit card process work? • Why are credit card services important to the merchant? • What characteristics should you look for in a credit card processor? • What are some sources to check the creditworthiness of a potential customer?

Questions and Problems • What effects do the following changes in terms have on the cost of trade credit? • a.Changing from 2/10 Net 30 to 3/10 Net 30. • b. Changing from 4/15 Net 40 to 3/15 Net 40. • c. Changing from 2/10 Net 30 to 2/15 Net 40 • 6. When should you consider loosening credit standards? tightening credit standards?

Incremental Analysis • Evaluating Changes in Credit Standards • CCRo = DSOo * ACSPDo * VCRo * kf • CCRn = DSOn * ACSPDn * VCRn * kf • DCCR = CCRn - CCRo

Incremental Analysis • Identifying Opportunity Costs • What happens when we receive cash later? • OC = DDSO * DACSPD * (1 - VCR) * kf • Where: • DDSO = change in DSO • DACSPD = change in ACSPD • (1 - VCR) = contribution margin • kf = opportunity cost of funds

Credit Standard Change • Impact on Receivables Investment (DI) • Assumption: Loosening credit standards will result in more sales but slower payment. • DI = DDSO*ACSPDo + VCR*DSOn* DACSPD • Assumption: Tightening credit standards will result in less sales but quicker payment. • DI = DDSO*ACSPDn + VCR*DSOo* DACSPD

Credit Standard Change • Changes in Profitability • DOP = DGP - DCCR - DBDE - DCD • Where: • DOP = changes in operating profits • DGP = changes in gross profits • DCCR = changes in cost of carrying A/R • DBDE = changes in bad debt experience • DCD = changes in cost of discounts taken

Credit Standard Change • Alternative Method for Change in Op Profits • DOP = DS*(1-VCR) - (kf*DI) - (BnSn - BoSo) • - (DnSnPn - DoSoPo) • Where: • DS = change in operating profits • Bo,n = bad debt expense rate (old, new) • So,n = sales activity • Po,n = percent of customers taking discount • Do,n = discount percent