Download

1 / 15

150 likes | 260 Vues

The Future of the Power Industry: The Russian View. Anatoly Chubais Chief Executive Officer RAO UES of Russia. Verbund-Conference – ENERGY 2020 21.09.2005 Fuschl, Austria. 5 000. 3 , 993. 4 %. 4 000. RAO UES of Russia. 3 000. 1 , 640. 2 000. Other. 1 , 088. 889. 96 %. 601.

E N D

The Future of the Power Industry: The Russian View Anatoly Chubais Chief Executive Officer RAO UES of Russia Verbund-Conference – ENERGY 2020 21.09.2005 Fuschl, Austria

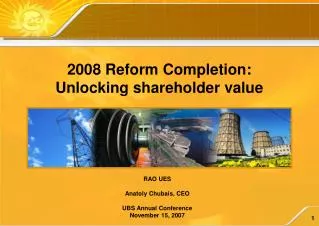

5 000 3,993 4% 4 000 RAO UES of Russia 3 000 1,640 2 000 Other 1,088 889 96% 601 597 567 555 30% 1 000 384 345 32% 0 70% US UK 68% TWh India China Brazil Japan Length of transmission lines RAO: 2,483 thsd km Russia France Canada Germany % of World Total Electricity generation RAO: 652bn kWh Heat generation RAO: 466m Gcal Source: IEA 24.9% 10.2% 6.8% 5.5% 3.7% 3.7% 3.5% 3.5% 2.4% 2.1% RAO UES and the Russian Electricity Market RAO UES of Russia: a leading role in the power industry

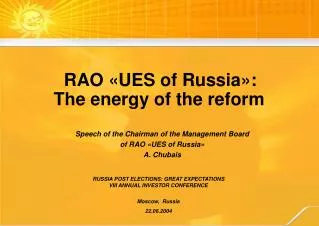

RAO UES and the Russian Electricity Market RAO UES Russia 1999-2004 RAO UES of Russia - financial performance US$m 23,593 25,000 25.0% 23,000 23.0% 21,000 19,339 20.0% 21.0% 19,000 16,052 17,000 18.0% 18.0% 13,712 15,000 15.0% 13,000 14.0% 10,520 11,000 8,780 10.0% 9,000 7,000 5,348 4,066 5,000 5.0% 5.0% 2,857 1,938 3,000 1,856 1,429 1,116 1,109 880 445 18 1,000 (1,000) 0.0% (400) 1999 2000 2001 2002 2003 2004 (2) (1) Revenues EBITDA Net Income EBITDA Margin Source: IAS Group financial results (1) Excluding doubtful debtor expense (2) As reported

Russia (2003) Global Power Market Trends: liberalization and globalization Market-Oriented Energy Industry Development:the choice of most countries California (1995) UK (1990) Private ownership Argentina (1990) Hungary (1999) Scandinavia(1992) Thailand (1996) Italy (1999) Moldova (1999) Kazakhstan (1998) Brazil (1995) EU Electricity Directive Austria (2001) Privatization Ukraine (1997) Greece (2000) South Africa (2000) Belarus (2004) Government ownership France (2000) Government regulation Deregulation Competitive market Sources: JP Morgan, RAO UES of Russia

Prerequisites for liberalization: opportunity… Spectacular development of advanced technologies …and necessity Consumers’ pressure on prices Global Power Market Trends: liberalization and globalization Power Sector Liberalization: a radical change over the last 15 years 1990s: launch of the liberalization process in the power sector involving complete unbundling of vertically integrated companies confined to their own region (country) Dramatic increase in competition Markets redistribution: crowding out the competitors and takeovers Greater geopolitical role of the power sector as a result of its liberalization

After acquiring TXU Australia, Singapore Power has emerged as a key player in the Australian electricity market Global Power Market Trends: liberalization and globalization Recent Major Cross-Border Acquisitions Sources: Cambridge Energy Research Association (CERA);PwC; companies’ data E.On National Grid Singapore Power PowerGen (2001)* • TXU Europe (2002) • PowerGen Renewable • Holdings (2002) • Midland Electricity • (2004) • TXU Australia (July 2004) • New England • Electric System (2000) • Niagara Mohawk (2001) On 30 July 2004, Singapore Power finalised its acquisition of TXUAustralia from TXU Corp, USA • Yorkshire Cogen (1998) • East Midland Electricity (1998) National Grid USA is one of the 10 largest electric utilities in the U.S. by number of customers (more than 3.2 million) E.On ranks 2nd in the UK with its 11% of the total generation * YearActualClosed

Global Power Market Trends: liberalization and globalization Power Sector: globalization is just the beginning Forecast: Further redistribution of assetsin the global electricity industry comparable, in scope and effect, to similar developments in the oil and gas markets

Generation • Market prices • Competitive environment Competitive sectors Market rules Sales Dispatching • Securing equal access to grids • Establishing the market infrastructure Transmission Regulated tariffs Monopolies Distribution Power Sector Reform and Liberalization in Russia RAO UES of Russia: reform basics

System operator FGC (Transmission) Wholesale GenCos, WGC (6) Territorial GenCos (14) IDC (Distribution) (4) Nuclear power generating company Hydro GenCo (1) Target Sector Model Power Sector Reform and Liberalization in Russia Monopolies Competitive Generation Private shareholders Government Competitivemarket FGC – Federal Grid Company IDC – Inter-regional distribution grid company

Business Trends in the Russian Power Industry: two-way street Foreign companies in Russia RAO UES of Russia in other countries • - Acquired or took under management electricity assets in Georgia, Armenia, Moldova; • - Launched the Sangtuda-1 hydropower plant construction in Tajikistan; • - RAO UES of Russia acquired 50% of the shares in a high-capacity power plant in Kazakhstan; • - RAO UES of Russia is a preferred bidder for the purchase of major generation assets in Bulgaria - Enel (Italy), in an alliance with ESN Energo, Russia, won a public tender for the operation of North-West CHP; - Fortum (Finland) acquired more than 30%of the shares in RAO UES’ Saint Petersburg regional utility Lenenergo;

Reliability and Interconnection Security of Energy Supply: lessons and conclusions Europe and North America: blackout geography and statistics • August 2003: USA/Canada. About 50 million people without electricity . . . • August 2003: UK. About 400,000 people. . . • September 2003: Denmark and Sweden. Almost 5 million people . . . • September 2003: Italy. About 57 million people . . . • May 2005: Russia. About 6million people . . . Conclusions from the Russian Blackout The accident was not caused by the liberalization or reform It is necessary to modify the liberalization and restructuring process to make it more reliability-oriented August 29, 2005: The Management Board of RAO UES of Russia approved the Action Program for Reliability Improvement of the Unified Energy System of Russia

Reliability and Interconnection Electric Border Between FSU Countries and Europe: a hurdle on the path to cooperation The solution proposed is interconnection

- Cooperation agreement on the joint feasibility study between the East (8 companies from FSU countries and the West (11 European companies)was signed (April 2005) Current activities - Development of the joint feasibility study of synchronous interconnection (2005-2007), with a Conceptual Report by end-2006 Reliability and Interconnection Integration of Electricity Systems of FSU Countries and Europe: the sequence of steps Accomplished activities - CIS Electric Power Council (CIS EPC) and UCTE agreed to undertake a joint feasibility study on synchronous interconnection (July 2003); - CIS EPC and EURELECTRIC signed a long-term cooperation agreement to promote future electricity markets integration (November 2003) • Synchronous integration Integration: Possible Options and/or • Asynchronousintegration • (installation of direct current links)

Climate Protection Climate and Environment Protection: challenges and business responsibility Major climate and environment protection initiative of RAO UES of Russia: support for the Kyoto Protocol mechanisms September 2004: the Kyoto Protocol was ratified by Russia allowing it to come into force Two main targets: Environment protection Technological breakthrough - Replacement of steam-turbine equipment by combined cycle turbine facilities - Conversion of existing equipment from coal to gas - Development of renewables, including small- and medium-capacity hydroelectric power plants Problem: correct direction, but low speed

Conclusions Global Power Sector: an arena of global changes The Russian power sector follows global trends using the best industry practices, taking account of Russia’s specificity. Common objectives and goals: • Market liberalization • Competing generation • Enhanced reliability • Environment protection • Participation by European strategic investors in the Russian power sector • Participation by Russian strategic investors in the European power sector 2020: For Europe, Russia should become more than a global supplier of oil and gas. Russian power sector should become an integral part of that of the continent.