HSC Business Studies 2009

460 likes | 801 Vues

HSC Business Studies 2009. Topic 2 -1 Financial Planning and Management. Objectives of Financial Management. The objectives of financial management are to maximise a business’s liquidity, profitability, efficiency, growth and return on capital. Liquidity

HSC Business Studies 2009

E N D

Presentation Transcript

HSC Business Studies 2009 Topic 2 -1 Financial Planning and Management

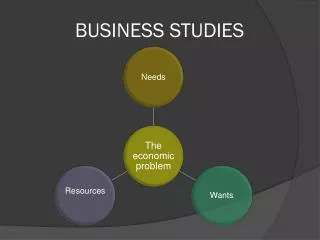

Objectives of Financial Management The objectives of financial management are to maximise a business’s liquidity, profitability, efficiency, growth and return on capital. • Liquidity The ability of a business to meet its financial commitments as they fall due. • Profitability Excess of revenue over expenses which a business seeks to maximise • Efficiency The ability of a business to use its resources effectively in ensuring financial stability and profitability. • Growth The ability of a business to increase its size or market share in the long-run. • Return on Capital The amount of profit returned to owners or shareholders as a percentage of their capital contribution.

Strategic Role of Financial Management Goals/Purpose/Mission Organisational Objectives Strategic Planning Tactical Planning Operational Planning

The goals a business sets are translated into organisational objectives which give a clear indication to management of what the business wants to achieve. The main objective of most business is to make a satisfactory level of profit. This will only occur if it has well defined and achievable goals. The strategies that an organization adopts work towards achieving its goals – both short and long term ones. Developing a strategic plan as part of an organization’s financial management will help guarantee its success.

Strategic plans are the most important. They encompass a long-term view of where the business should go and how to get there. In the process, it monitors progress towards its stated goals, making provision for remedial intervention if actual outcomes deviate significantly from the strategic plan.

Managing Financial Resources Financial resources are those resources of a business that have a monetry value. Financial management is the planning and monitoring of an organisation’s financial resources to enable it achieve its financial goals.

Themismanagement of financial resources can lead to problems such as Insufficient cash to pay suppliers Inadequate capital for expansion Too many assets that are not productive Delays in accounts being paid Misappropriation of funds Business failure.

Strategies for monitoring the financial resources of an organization must be incorporated into its strategic plan and should include: Monitoring cash flows and payment of debts Developing financial control techniques Auditing of financial accounts Profit and dividend projections.

The planning process involves the setting of goals and objectives, determining strategies to achieve them, identifying and evaluating alternative courses of action and choosing the best alternative. Financial planning is essential if a business is to achieve its goals. The financial planning process begins with long-term or strategic financial plans. Long-term plans cover a period of between 2 to 10 years. Short-term plans are more specific and cover periods of 1 to 2 years or less. Financial Planning Process The Planning Cycle

Long-term plans include an organisation’s planned capital expenditure and planned investments. Capital expenditure is spending on non-current assets such as buildings and vehicles. It is used to generate revenue and returns to owners and shareholders. Long-term plans also cover planned sources of finance, spending on research and development, marketing and product development activities.

A business plan might be used when seeking finance or support for a project from a bank or other financial institution or other potential investors. A business plan should set out finance required, the proposed sources of finance and a range of financial statements. The information contained in a financial plan will be determined by the audience to which it is directed: owners, employees, lenders, potential investors etc.

Accounting as ‘Recording System’ Record systems are the mechanisms employed by an organisation to ensure that data are recorded and the information provided by the record keeping system is accurate, reliable and efficient. Every step must be taken to minimise errors in the recording system. The double entry system of accounting is used. By recording each transaction twice, the entries can be seen to balance and the check to identify errors when they fail to balance can be carried out quickly.

Financial Reports Important financial information needs to be collected before future plans can be made. This financial information includes: Balance Sheets Revenue Statements Cash Flow Statements Sales and Price Forecasts Budgets Bank Statements Weekly reports from departments Break-even Analysis Financial Ratio Analysis and Interpretation of Reports

Financial reports are crucial for effective financial management. There are two main types of financial reports: • General Purpose Financial Reports (GPFRS) • Special Purpose Financial Reports (SPFRS)

GPFRs are financial statements that all public companies are required by law to produce. They Include: • Balance Sheets • Revenue Statements • Statement of Cash Flows GPFRs are useful to or required by: • ATO • Shareholders • Creditors • Regulatory Authorities (ASIC, ASX) • Shareholders GPFRs are produced in accord with Generally Accepted Accounting Principles (GAAPs)

SPFRs are financial statements prepared by a business for use by internal stakeholders. More detailed than GPFRs and do not have to comply with externally determined criteria. SPFRs includes: • Budgets • Sales Reports • Break-even analysis. SPFRs allow management compare actual with predicted performance. They give management information on which to make informed decisions. Financial Accounting revolves around GPFRs and Management Account around SPFRs.

Revenue Statement A Revenue Statement shows the revenue and expenses of a business for a particular period of time.

Revenue statement for year ended 30 June 2006 Sales 150 000 Cost of goods sold 105 000 Gross profit 45 000 Operating expenses Administrative 5 000 Selling & distribution 7 000 Financial 3 000 Net Profit 30000

Balance Sheet A Balance Sheet is a statement of financial position of a business at a particular point in time. A Balance Sheet shows assets and liabilities. The difference between Assets and Liabilities is Owner’s Equity (Capital, Net Worth, Proprietorship). On this basis, a Balance Sheet is based on the Accounting Equation which is: OE (owners equity) = ASSETS – LIABILITIES

Cash Flow Statements Adequate cash flow is essential to the success of a business. Some business operate on a cash only business. In such a case cash flow is easier to manage. Most businesses operate on a cash/credit basis. Here the business will need to ensure it will have sufficient cash on hand to meet its day-to-day operations and debts that have to be paid, as well as sufficient cash to replace equipment. A Cash Flow Budget records the expected receipts of cash (inflows) and payments of cash (outflows) over a period of time. The budget will show whether the business can expect either a surplus or shortage (deficit) of cash. Cash flow budgets are usually prepared for 1-3 month periods. If excess cash is identified in the cash flow budget, plans can be made for its placement in short term ibvestments to maximise income. If a shortage of cash is expected, then plans can be made to borrow short term or reorganise current assets. If borrowing necessary to meet a shortfall of cash, it should be at the lowest interest rate possible, which is often a bank overdraft.

How to Avoid a Cash Flow Crisis • Account for every dollar spent and do your banking regularly • Install an up-to-date and relevant accounting system • Keep your financial records up-to-date • Keep a detailed account of all debtors and act promptly on overdue accounts and dishonoured cheques • Draw up budgets and cash flow forecasts • Be prepared for anticipated tax instalments and other payments • Reconcile your bank statements regularly: double-check receipts and payments with your own records • Never pay accounts unless a tax invoice bearing an ABN is provided • Retain all records for GST taxable purchases • Consider offering discounts for cash payments or early settlement of accounts receivable • Keep a detailed list of accounts owing and when they are due for payment. Ask for discounts on early payment.

Break-even Analysis Break-even analysis is an example of a SPFR. It is prepared for management and shows at what point a project or process will start earning profit. It is crucial for management decision-making.

Developing Budgets Budgets provide information in quantitative terms (figures) about requirements to achieve a particular purpose. A business should produce a budgeted Cash Flow Statement, budgeted Revenue Statement and budgeted Balance Sheet. Budgets will show: Cash required for planned outlays for a particular period Cost of capital outlay and estimated earning capacity Estimated cost of raw materials and other inventories Number of hours and cost of labour for production.

Budgets are used in both the planning and control aspects of business. They reflect strategic planning decisions about how resources are to be used. Budgets enable constant monitoring of objectives and provide a basis for administrative control, production planning, direction of sales and marketing efforts, control of inventories etc. Various factors need to be taken into account in preparing a budget such as: Review of past forecasts and actual results, as well as trends in the industry and in the economy Potential growth in market and current market share Proposed expansion or discontinuation of projects Proposals to alter price of products Current orders and plant capacity.

Planning Financial Controls The most common causes of financial problems and losses are: Theft Fraud Damage to or loss of assets Errors in record system. Theft and fraud include unnecessary or over-purchase of stock for personal use, conflict of interest, misuse of expense accounts, false invoices, theft of inventory or assets and credit card fraud.

Financial controls ensure plans will lead to the achievement of the organisation’s goals in the most efficient way. Control is especially important in assets such as accounts receivable, inventory and cash.

Policies and procedures promoting control within an organisation are: Clear authorisation and responsibility for tasks in the organisation Separation of duties, eg. one person is responsible for ordering and another for receiving inventories; one person writes cheques and another signs them Rotation of duties, eg. staff are skilled in a number of areas and can rotate duties Control of cash: use of cash registers, cash banked daily, payments made by cheque not cash Protection of assets: buildings kept locked, registry of assets maintained, regular checks of inventory, surveillance systems are installed Control of credit procedures: following up overdue accounts and credit checks of customers.

Financial risk is the risk to a business of being unable to cover its financial obligations. If this occurs, bankruptcy will result. Questions a business shouldask in relation to financial risk are: Should the business borrow to expand operations? Will owners/shareholders finance expansion or will the money be borrowed?

Should excess funds be used to purchase assets or be invested in the short-term money market? What direction are interest rates likely to move? Will the business be affected by changing exchange rates? What is the current level of borrowings and when is it due to be repaid? Has the business sufficient current assets to finance operations.

To minimise financial risk, business must consider the amount of profit that will be generated. The profit must be sufficient to cover the cost of debt as well as increasing the net wealth of owners.