Download

1 / 8

90 likes | 284 Vues

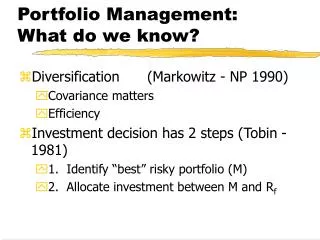

Portfolio Management: What do we know?. Diversification (Markowitz - NP 1990) Covariance matters Efficiency Investment decision has 2 steps (Tobin -1981) 1. Identify “best” risky portfolio (M) 2. Allocate investment between M and R f. Portfolio Management: What do we know?.

E N D

Portfolio Management: What do we know? • Diversification (Markowitz - NP 1990) • Covariance matters • Efficiency • Investment decision has 2 steps (Tobin -1981) • 1. Identify “best” risky portfolio (M) • 2. Allocate investment between M and Rf

Portfolio Management: What do we know? • Risk has two parts • Assets are priced to make M efficient • Systematic risk is all that matters • Beta and CAPM • Option Valuation and Hedging (Merton and Scholes NP-1997) • option risk can be derived from security risk • delta hedging

What do Portfolio Managers do? • “Markets are efficient” • indexation • get better information • asset allocation • risk management • “Markets are inefficient” • find mispriced securities () • identify tops and bottoms

Investment Objectives • PM must start with a clear objective! • Four-step process • 1. Devise a policy statement • 2. Study current financial/econ. Conditions • 3. Construct portfolio • 4. Monitor/update investor’s needs and market conditions • Applies to individual and institutional investors

Objectives: Return LT vs ST needs Total Return = Cap Gain + reinvestment income Risk tolerance Capital preservation Capital appreciation Current income Constraints: Liquidity needs Time Horizon Tax Factors Legal/Regulatory Factors Unique needs and preferences Objectives: Policy Statement

Suitability and Optimality • Suitability: The appropriateness of particular investments or portfolios of investments for specific investors • Optimality: developing a portfolio with the highest expected return for a given level of risk (also called efficiency)

Scenario 1 • 70-year old widow provides her life savings of $300,000 to a financial planner. Portfolio earnings represent nearly all of her income. The planner places 50% of her funds in corporate bonds rated AA or higher and 50% in a variety of vehicles including penny stocks, options, and commodity futures. After two years, interest rates have fallen, but the total value of the portfolio is $240,000 due to losses and trading expenses of managing the speculative portion of the portfolio. • Has the planner acted ethically? • Is the portfolio suitable?

Scenario 2 • A 45-year old man with some investment experience opens an account with a discount broker. His wealth is sufficient to allow writing of naked options. He begins trading aggressively, primarily selling puts on stocks and stock indicies. In six months, he has accumulated losses in excess of $100,000. • Is the broker acting ethically? • Is the portfolio being maintained for him suitable?