Fraud and Internal Control

Fraud and Internal Control. Presented by Andy Harper Pugh & Company, P.C. April 28, 2011. Outline and Learning Objectives. Types of Fraud Considering Fraud Conditions Red Flags Controls to deter or detect fraud Specific controls to help churches. Types of Fraud.

Fraud and Internal Control

E N D

Presentation Transcript

Fraud and Internal Control Presented by Andy Harper Pugh & Company, P.C. April 28, 2011

Outline and Learning Objectives • Types of Fraud • Considering Fraud Conditions • Red Flags • Controls to deter or detect fraud • Specific controls to help churches

Types of Fraud • Misappropriation of assets • Fraudulent financial reporting

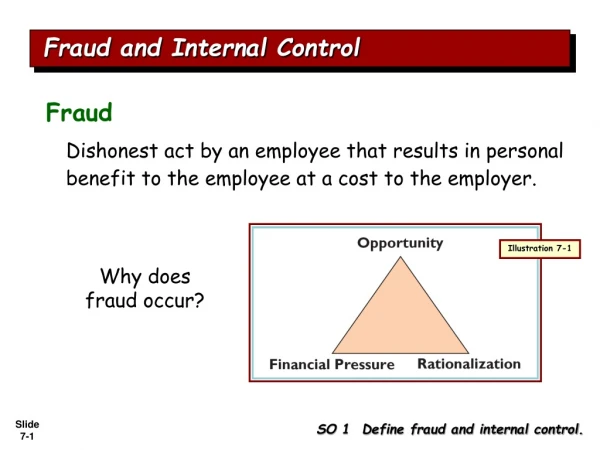

Considering Fraud Conditions Conditions present when fraud occurs: • Incentives/pressures to commit fraud • Opportunities to carry it out • Attitudes/rationalizations to justify it

Incentives and Pressures Generally, incentives and pressures to misappropriate assets may be classified as either: • Personal financial obligations that create pressure on employees with access to assets susceptible to misappropriation to steal those assets • Adverse relationships between the business and its employees with access to those assets that motivate them to steal those assets

Incentives and Pressures Pressures that may motivate an individual to steal may be financial in nature, relate to a personal habit, or stem from work-related feelings.

Incentives and Pressures Personal financial obligations include factors such as • debt arising from high medical bills • overuse of credit cards • divorce • investment losses • sheer greed. Personal habits may include • alcohol, drug, or gambling addiction • an expensive extramarital affair Work-related factors may include • feelings of resentment because of being overworked, underpaid, or not promoted

Incentives and Pressures For fraudulent financial reporting, the incentives and pressures are somewhat different. • Pressures to achieve a certain level of financial results in order to keep a job, to obtain a bonus or other compensation based on financial results • Support a financing plan

Incentives and Pressures Generally, incentives or pressures to commit fraudulent financial reporting may be classified into the following categories: • Economic, industry, or operating conditions that threaten the financial stability or profitability • Pressures to meet the requirements or expectations of third parties, such as investors or creditors • Conditions related to the organization's financial performance that threaten the personal net worth of management or the owner • Pressures to meet financial targets set by management or the owner/manager.

Incentives and Pressures Situations that may increase the pressure to achieve certain financial results include: • unfavorable economic conditions within an industry • insufficient working capital • high debt levels or credit difficulties • and pressures related to a pending merger or acquisition.

Opportunities Misappropriation of assets • Assets susceptible to theft • Inadequate safeguarding Fraudulent Financial Reporting • Inadequate monitoring • Accounts or transactions susceptible to manipulation

Opportunities Generally, conditions that provide opportunity for misappropriation of assets to occur may be classified into the following categories: • Circumstances or characteristics of the assets that increase their susceptibility to misappropriation, such as ready marketability, liquidity, high value, or small size. • Inadequate internal controls over assets susceptible to misappropriation, such as lack of safeguards.

Opportunities Conditions that provide opportunity for fraudulent financial reporting to occur may be classified into the following categories: • Conditions related to the nature of the industry or the entity's operations, such as significant related-party transactions. • Ineffective monitoring of management. • A complex or unstable organizational structure. • Internal control deficiencies.

Attitudes/Rationalizations Some typical rationalizations for misappropriation of assets and fraudulent financial reporting include— • I am only borrowing the money and will pay it back. • Nobody will get hurt. • The company treats me unfairly and owes me. • It's for a good purpose. • It's only temporary, until operations improve. • Employees are depending on us to protect their jobs.

Attitudes/Rationalizations Personal integrity may be the most important factor in keeping a person from misappropriating assets or fraudulently misstating the financial statements.

Red Flags • Missing records • Original documents not available • Accounts not reconciled • Current financial statements not available • Employees that work excessive hours • Employees with serious family or personal issues • Employee lifestyle changes

Red Flags • Employees who are possessive with their work • Stale-dated outstanding items on reconcilements • IRS notices related to payroll taxes

Controls to Deter and Detect Fraud • Segregation of duties • Oversight • Supporting documentation for transactions • Communication and enforcement of ethical values • Reconcilement of subsidiary ledgers, bank accounts, investments, loans, payroll register, accounts payable, etc. to the general ledger

Controls to Deter and Detect Fraud • Independent checks • Access and authorization controls

Specific Controls to Help Churches • Segregate cash handling from posting and reconciling the bank account. • Independent review of the bank account reconcilement. • Periodic review of budget versus actual results • Periodic review of payroll transaction journal

Specific Controls to Help Churches • Segregation of duties related to A/P, check writing and posting, and check signing • Proper approval process for A/P and check signing