Download

1 / 77

770 likes | 865 Vues

Learn about the Tax Relief, Unemployment Insurance, Reauthorization, and Job Creation Act of 2010, its implications, and how it affects estate, gift, and generation-skipping transfer taxes. Gain insights on temporary extensions and modifications.

E N D

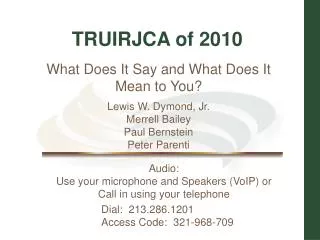

TRUIRJCA of 2010 What Does It Say and What Does It Mean to You? Lewis W. Dymond, Jr.Merrell BaileyPaul BernsteinPeter Parenti Audio:Use your microphone and Speakers (VoIP) orCall in using your telephone Dial: 213.286.1201Access Code: 321-968-709

TRUIRJCA of 2010 What Does It Say and What Does It Mean to You? Lewis W. Dymond, Jr.Merrell BaileyPaul BernsteinPeter Parenti

Circular 230 Pursuant to the rules of professional conduct set forth in Circular 230, aspromulgated by the United States Department of the Treasury, nothing contained inthis communication was intended or written to be used by any taxpayer for thepurpose of avoiding penalties that may be imposed on the taxpayer by the InternalRevenue Service, and it cannot be used by any taxpayer for such purpose. Noone, without our express prior written permission, may use or refer to any taxadvice in this communication in promoting, marketing, or recommending apartnership or other entity, investment plan or arrangement to any other party. For discussion purposes only. This work is intended to provide general informationabout the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010. The author, WealthCounsel, LLC or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors. WealthCounsel, LLC

Introduction • “Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010” • TRUIRJCA 2010. • An Amendment to H.R. 4853 passed earlier in the year which authorizes funding of the Airport and Airway Trust Fund. WealthCounsel, LLC

Temporary Extension ofSunset of EGTRRA 2010 Section 1.01 – Temporary Extension of 2001 Tax Relief. Amends Section 901 of EGTRRA. • Substitute December 31, 2012 for December 31, 2010. • Effective as if included in the enactment of EGTRRA 2010. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 301 - Reinstatement of Estate Tax; Repeal of Carryover Basis. • (a) IN GENERAL - Accomplished by repealing Subtitle A and E of Title V of EGTRRA. • Subtitle A – made the Chapter 11 (estate taxes) inapplicable to estates of decedents dying after 2009 and Chapter 13 (GSTT) inapplicable to generation-skipping transfers after 2009. • Subtitle E – contained the modified basis adjustment under Section 1022. • (b) Conforming Amendment. • Clean-up amendment to Section 2505(a)(1) from EGTRRA language to deal with re-unification of the gift and estate tax. • This may take further work.

Title IIITemporary Estate Tax Relief Section 301 - Reinstatement of Estate Tax; Repeal of Carryover Basis. • (c) - Special election with respect to estates of decedents dying in 2010. • Can opt back into repeal of estate tax and modified basis adjustment under EGTRRA Section 1022. • Election applies the code as if the amendment repealing the estate tax had not been made with respect to the repeal of Chapter 11 (the estate tax). • Amendment eliminating the repeal of Chapter 13 (the GSTT) would still apply so the decedent will still be considered a transferor for GSTT purposes. • But the GSTT rate is zero percent.

Title IIITemporary Estate Tax Relief Section 301 - Reinstatement of Estate Tax; Repeal of Carryover Basis. • (d) Extension of time until 9 months after date of enactment. • Filing an estate tax return • GSTT returns; • Filing a basis allocation return; • Paying estate taxes; and • Making disclaimers (still need to satisfy state law). • (e) Effective date • Retroactive application to end of 2009. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 302 - Modifications to Estate, Gift and Generation-Skipping Transfer Taxes. • (a) Modifications to estate tax • Applicable exclusion amount increased to $5M. • Adjusted for inflation after 2011 to nearest $10K. • Maximum estate tax rate 35%. • (b) Modifications to gift tax. • Restoration of unified credit against gift tax for gifts after 2010. For 2010 gifts determined as if applicable exclusion amount were $1M. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 302 - Modifications to Estate, Gift and Generation-Skipping Transfer Taxes. • (c) Modification of generation-skipping transfer tax. • GSTT rate for 2010 is 0%. • All other GST rules apply. • Generation-skipping transfers not exempt. • 0% rate in 2010. • 35% rate after 2010. • Generation-skipping transfers do not create an inclusion ratio of zero; must apply GST Exemption. • GST Exemption equal to the applicable credit amount $5M. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 302 - Modifications to Estate, Gift and Generation-Skipping Transfer Taxes. • (d) Modification of estate and gift taxes to reflect differences in credit resulting from different tax rates. • Modifications to IRC § 2001(b)(2) and § 2505(a). • Provide technical computational guidance for calculating the tentative tax taking into account lifetime gifts. • Includes guidance for determining the amount of the credit for gift taxes paid taking into consideration the amount of applicable exclusion amount. • Appears to be an attempt to legislatively modifyPLR 9250004. • There is a difference of opinion as to how this plays out if we have a total Sunset.

Title IIITemporary Estate Tax Relief Section 302 - Modifications to Estate, Gift and Generation-Skipping Transfer Taxes. • (e) Conforming amendment. • Repeals Section 2511(c), the provision that went into effect in 2010 treating all transfers in trust as gifts unless the trust is wholly “grantor trust” as to the donor. • Effective date. • Retroactive as to December 31, 2009. • Except as to the gift tax re-unification.

Title IIITemporary Estate Tax Relief Section 303 – Applicable Exclusion Amount Increased by Unused Exclusion Amount of Deceased Spouse. • Further modification of applicable exclusion amount for estates and gifts after 2010. • Sum of: • Basic exclusion amount $5M adjusted for inflation; and • For a surviving spouse, any deceased spousal unused exclusion amount (DSUEA). • Deceased spousal unused exclusion amount for a surviving spouse is the lesser of: • The basic exclusion amount; or • The basic exclusion amount of the last deceased spouse, minus • The sum of that spouse’s taxable estate and adjusted taxable gifts. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 303 – Applicable Exclusion Amount Increased by Unused Exclusion Amount of Deceased Spouse. • Special Rules. • Election Required – DSUEA not available unless timely estate tax return filed, amount computed and election made. • IRS may examine prior returns after period of limitations with respect to DSUEA. • Secretary to prepare regulations. • (b) Conforming Amendments. • Indexed $5M and filing thresholds apply to basic exemption amount not exemption amount. • Effective date • December 31, 2010. WealthCounsel, LLC

Title IIITemporary Estate Tax Relief Section 304 – Application of EGTRRA Sunset to this Title. • Section 901 of EGTRRA applies to the amendments made by this section (sic). WealthCounsel, LLC

Title VIITemporary Extension of Certain Expiring Provisions Section 725 – Tax-free distributions from individual retirement plans for charitable purposes. • Termination date of IRC § 408(d)(8) extended through December 31, 2011 retroactive to January 1, 2010. • Client age 70 1/2 or over may make charitable donation up to $100,000 directly from IRA accounts to charity. • Donations made in January, 2011 may be counted as having been made in 2010. WealthCounsel, LLC

Elect out of Estate Tax;Elect into Modified Basis Adjustment WealthCounsel, LLC

Carryover Basis Election With the retroactive reinstatement of the estate tax, the carryover basis provisions of I.R.C. § 1022 are repealed, effective January 1, 2010. • However, the Executor (IRC § 2203) of the estate of a decedent who died in 2010 may elect to have the modified basis rules of I.R.C. § 1022 apply “with respect to property acquired or passing from the decedent” within the meaning of I.R.C. § 1014(b)). WealthCounsel, LLC

Carryover Basis Election With the retroactive reinstatement of the estate tax, the carryover basis provisions of I.R.C. § 1022 are repealed, effective January 1, 2010. • If the election is made the estate tax will not apply and I.R.C. § 1014(a) will not apply. • If no election is made, the Estate Tax will apply to estates of decedents who died in 2010 and the fair market value basis rules of I.R.C. § 1014(a) will apply. WealthCounsel, LLC

Carryover Basis Election • The election shall be made at such time and in such manner as the Secretary of the Treasury or the Secretary’s delegate shall provide. • Such an election once made shall be revocable only with the consent of the Secretary of the Treasury or the Secretary’s delegate. (The Commissioner of the Internal Revenue Service). WealthCounsel, LLC

Carryover Basis Election • In almost all cases for 2010 estates of less than the available applicable exclusion amount, now $5M, the election should not be made. WealthCounsel, LLC

Carryover Basis Election • Section 1022 – Treatment of property acquired from a decedent dying after 12/31/2009. • 1022(a) – In general. • Carry over basis. • Treated same way as property transferred by gift. • Basis is the lesser of decedent’s adjusted basis or fair market value on date of death • 1022(b) – Basis increase for certain property • $1.3M of basis increase. $60K for non-resident non-citizens • No restrictions on who can receive • Must be “acquired from a decedent” – won’t apply to QTIP property or Section 2041 power of appointment property WealthCounsel, LLC

Carryover Basis Election • Section 1022 – Treatment of property acquired from a decedent dying after 12/31/2009. • 1022(c) –Additional $3M basis increase for “qualified spousal property.” • Outright transfers to spouse or QTIP. • Spouse has a “qualified income interest.” • All income on at least an annual basis. • No person has a power to appoint to any person other than spouse. • May not apply to general appointment trusts or even survivor’s trust on a joint RLT. WealthCounsel, LLC

Carryover Basis Election Only “Property Acquired” from a decedent is entitled to a step-up in basis under § 1022(b) and (c). • IRC Section 1022(e). • Not General Power of Appointment property. • Not Surviving-Spouse-via-QTIP property. • Not IRC Section 2036 or 2038 property. i.e. Grantor dies during GRAT or QPRT. • Not IRD assets (IRA accounts). • Not property received via gift within 3 years of death except yes property received via gift within 3 years of death from spouse. WealthCounsel, LLC

Carryover Basis Election • The carryover basis report under § 6018 is required to be filed with the decedent’s final in come tax return. I.R.C. § 6075(a). • The due date for filing this report may also be deferred up to 9 months after the date of enactment (December 17, 2010). • TRUIRJCA 2010 § 301(d)(1)(A). • Draft of Form 8939 draft was released by IRS just before TRUIRJCA 2010. • IRS is collecting comments. • May be revised as a result of TRUIRJCA 2010. WealthCounsel, LLC

Carryover Basis Election WealthCounsel, LLC

Carryover Basis Election WealthCounsel, LLC

Carryover Basis Election WealthCounsel, LLC

Carryover Basis Election • Factors to consider when making the decision for taxable estates: • Estate tax payable currently vs. the capital gain tax on the future sale of assets. • Anticipated dates of sales of assets. • Ability to allocate basis adjustments up to the fair market value at the date of death for assets that will likely be sold in the near future. • Anticipated future capital gains rates (and ordinary income rates for “ordinary income property”). • Weighing the present value of anticipated income tax costs against the current estate tax amount

Carryover Basis Election Factors to consider when making the decision for taxable estates: • 35% estate tax or…

Carryover Basis Election • Resolving potential disputes among heirs: • Whether to make the election? • Where the marital deduction share goes to the spouse; and • The non-marital deduction share goes to deceased spouse’s children. • What property gets the limited basis increase? • Family agreement with court approval. • Pro rata allocation with court approval.

Carryover Basis Election Fred dies, leaving $6.3M estate to Child. • Fred’s basis in the $6.3M estate is $5M. • Estate tax calculation. • $6.3M estate - $5M exemption = $1.3M taxable estate. • $1.3M TE x 35% tax = $455,000 estate tax due. • Income tax calculation. • $6.3M assets - $5M basis = $1.3M in gain. • Section 1022(b) Special Basis Allocation of $1.3M. • Child’s basis is $6.3M, so complete step-up in basis. • Easy, choose carryover basis.

Carryover Basis Election Fred dies, leaving $8M estate with basis of $2M to wife Grace. • Estate tax calculation • $8M estate – unlimited marital exemption = zero taxable estate = zero estate tax. • Complete step-up in basis under Section 1014. • If left in QTIP, can make partial QTIP election to preserve $5M exemption amount or possible disclaimer to remainder beneficiaries. • Elect out of estate tax and into Section 1022 • $8M assets - $2M basis = $6M in built in gain. • Only $4.3M of basis adjustment available; special basis allocation of $1.3M plus spousal basis adjustment of $3M. • Adjusted basis of $6.3M vs. $8M basis with estate tax.

Carryover Basis Election • Fred dies, leaving $9M estate with basis of $6M all LTC assets. • $3 million to Child A. • H’s basis is $2 million. • $6 million to Child B. • H’s basis is $4 million. • Estate tax would be 35% x $4M = $1.4M.

Carryover Basis Election Fred dies, leaving $9M estate with basis of $6M all LTC assets (continued). • Carryover basis looks like easy answer, right? • Adjusted basis of $7.3M ($6M + $1.3M). • LTC gain of $1.7M ($9M minus $7.3M). • Total income tax @ 15% LTCG = $255,000. • Total income tax @ 20% LTCG = $340,000. • Medicare Surtax @ 3.8% = $64,600. • Total between $314,600 and $404,600 vs. $1.4M. • But Executor allocates basis of $1.3M to A or B. • All to A? All to B? ½ to each? 1/3 to A and 2/3 to B? • What if Executor is Child A or Mother of Child B? • Cost to complete and calculate Form 8939?

Carryover Basis Election Fred dies, leaving $20M estate with basis of $5M one half to wife Grace and one half to his children. • Estate tax calculation. • All property receives full step-up in basis. • $10M to wife – no estate tax. • $8.75M to children - $10M minus $1.75M estate tax (($10M - $5M ) x 35%). • Elect out of estate tax and into Section 1022. • $10M to wife – basis of $2.5M increased to $5.5M. • Built in LTC gain of $4.5M vs. no built in LTC gain. • $10M to children – basis of $2.5M increased to $3.8M. • Built in LTC gain of $6.2M vs. estate taxes of $1.75M. • What if beneficiaries don’t plan to sell assets?

Generation-SkippingTransfer Tax Section 302(c) – Modification of Generation-Skipping Transfer Tax. • GSTT rate for 2010 is 0%. • All other EGTRRA GSTT rules apply. • GST Exemption equal to the applicable credit amount $5M. • GSTT rate after December 31, 2010 is 35%. • Subject to Sunset per EGTRRA Section 901 as of December 31, 2012. WealthCounsel, LLC

Generation-SkippingTransfer Tax Planning with a larger GST Exemption. • Avoid temptation to believe that GSTT planning has become irrelevant because of the $5M exemption. • Current $5M GSTT exemption makes it easy to create dynasty trusts that will: • Be exempt from estate taxes; GSTT taxable distributions; and GSTT taxable terminations. • Asset protected. • For as long as applicable RAP provision will allow. • We don’t know how long the $5M GST Exemption will be with us. • Subject to Sunset provisions. • Dynasty trust are designed to last a long time and further modification is likely.

Generation-SkippingTransfer Tax Planning with a larger GST Exemption. • GST Exemption used to be a very limited resource. • Sometimes it could be difficult to decide how to best use and leverage this limited resource: • Multi-generational gifting trusts. • Multi-generational ILITs. • Multi-generational IDGTs. • With larger GST Exemption our choices are less limited and easier to implement.

Generation-SkippingTransfer Tax Designing Multi-Generational Trusts. • Design so that gifts to the trust are completed gifts. • Design to avoid inclusion in grantor’s estate. • Design to avoid estate tax in beneficiaries’ estates by making sure that no beneficiary has a general power of appointment. • Design to benefit multiple generations by using cascading trusts. • Allocate sufficient GST Exemption to always have an inclusion ratio of zero.

Generation-SkippingTransfer Tax • Summary of Multi-Generational Gifting Trust Strategy. • Create a multi-generational irrevocable trust. • Typically will use Crummey powers to qualify as present interest gifts and use annual gift tax exclusion. • With prior limited GST Exemption this was frequently considered to be a less efficient use of the GST Exemption because of lack of leveraging. WealthCounsel, LLC

Generation-SkippingTransfer Tax • Summary of Multi-Generational ILITs. • Create a multi-generational irrevocable trust. • Use gifts to purchase life insurance. • Typically will use Crummey powers to qualify as present interest gifts and use annual gift tax exclusion. • Frequently it was difficult to find enough Crummey beneficiaries to pay the annual premium. • With increased gift tax exemption can use exemption to purchase a single premium policy. • Before there may not have been sufficient GST Exemption to cover all of the premium payments. WealthCounsel, LLC

Generation-SkippingTransfer Tax • Summary of IDGT Strategy. • Create a multi-generational irrevocable trust. • Design so that transfers are completed gifts. • Designed to avoid estate tax inclusion in Grantor’s estate. • Include provision(s) that cause the trust to be deemed to be owned by the Grantor for income tax purposes without causing estate tax inclusion(IRC §§ 671 through 679). • Allocate GST Exemption to any transfers so that IDGT has an inclusion ratio of zero. WealthCounsel, LLC

Generation-SkippingTransfer Tax • Power of IDGTs • Grantor taxed on income. • Payment of taxes by Grantor not considered a gift. • Assets in IDGT grow faster when Grantor pays income taxes • Sale of assets to an IDGT by the Grantor are ignored for income tax purposes. • Estate freeze • Purchase of value adjusted family investment entities. • Grantor trusts with same grantor can exchange properties without recognition of income, capital gains or capital loses (PLRs 200434012 and 200606027). WealthCounsel, LLC

Generation-SkippingTransfer Tax • Now Easier to Overcome IDGT Limitations. • Limited amount of GST Exemption, limited amount that can be transferred to IDGT and maintain inclusion ratio of zero. • Sale of assets to an IDGT by the Grantor must be commercially reasonable. • Seed money needed. • Personal guarantees. • Increase in GST Exemption greatly increases IDGITs’ power and easy of use. WealthCounsel, LLC

Portability of Deceased Spouse’s Unused Exclusion Amount(DSUEA)

Portability • Requirements: • Married at time of death. • Death of spouse occurs after December 31, 2010. • Election to transfer any DSUEA must be made on timely filed 706. • May only be transferred to a surviving spouse. • The DSUEA (or lack thereof) of the last deceased spouse wipes out any DSUEA previously transferred to the surviving spouse by an earlier deceased spouse. WealthCounsel, LLC

Portability • Additional Information: • For Estate and Gift tax purposes. • GST Exemption is not portable; any unused GST Exemption cannot be transferred to a surviving spouse. WealthCounsel, LLC

Portability • Query: • Must a surviving spouse die before December 31, 2012 to get the benefit of a DSUEA? • Does a DSUEA acquired before Sunset disappear on December 31, 2012? WealthCounsel, LLC

![2010 Division of Revenue Bill [B4-2010]](https://cdn2.slideserve.com/4044262/2010-division-of-revenue-bill-b4-2010-dt.jpg)