Enron Canada 4

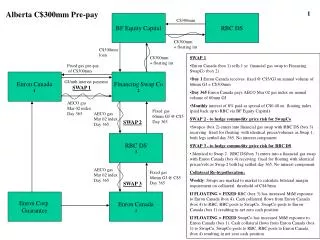

Alberta C$300mm Pre-pay. 1. BF Equity Capital. RBC DS. C$300mm. C$300mm + floating int. C$300mm loan. C$300mm + floating int. SWAP 1 Enron Canada (box 1) sells 1 yr financial gas swap to Financing SwapCo (box 2)

Enron Canada 4

E N D

Presentation Transcript

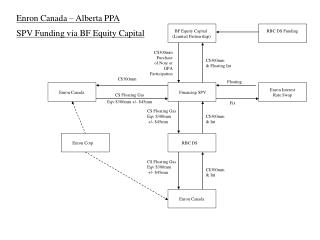

Alberta C$300mm Pre-pay 1 BF Equity Capital RBC DS C$300mm C$300mm + floating int C$300mm loan C$300mm + floating int • SWAP 1 • Enron Canada (box 1) sells 1 yr financial gas swap to Financing SwapCo (box 2) • Day 1 Enron Canada receives fixed @ C$5/GJ on annual volume of 60mm GJ = C$300mm • Day 365 Enron Canada pays AECO Mar 02 gas index on annual volume of 60mm GJ • Monthly interest of 8% paid as spread of C$0.40 on floating index (paid back up to RBC via BF Equity Capital) • SWAP 2 - to hedge commodity price risk for SwapCo • Swapco (box 2) enters into financial gas swap with RBC DS (box 3) receiving fixed for floating with identical prices/volumes as Swap 1, both legs settled day 365. No interest component • SWAP 3 - to hedge commodity price risk for RBC DS • Identical to Swap 2. RBC DS(box 3) enters into a financial gas swap with Enron Canada (box 4) receiving fixed for floating with identical prices/vols as Swap 2 both leg settled day 365. No interest component. • Collateral Re-hypothecation: • Weekly: Swaps are marked to market to calculate bilateral margin requirement on collateral threshold of C$45mm. • If FLOATING < FIXED RBC (box 3) has increased MtM exposure to Enron Canada (box 4). Cash collateral flows from Enron Canada (box 4) to RBC, RBC posts to SwapCo, SwapCo posts to Enron Canada (box 1) resulting in net zero cash position • If FLOATING > FIXED SwapCo has increased MtM exposure to Enron Canada (box 1). Cash collateral flows from Enron Canada (box 1) to SwapCo, SwapCo posts to RBC, RBC posts to Enron Canada (box 4) resulting in net zero cash position Fixed gas pre-pay of C$300mm Enron Canada 1 Financing Swap Co 2 GJ/mth interest payment SWAP 1 AECO gas Mar 02 index Day 365 Fixed gas 60mm GJ @ C$5 Day 365 AECO gas Mar 02 index Day 365 SWAP 2 RBC DS 3 AECO gas Mar 02 index Day 365 Fixed gas 60mm GJ @ C$5 Day 365 SWAP 3 Enron Corp Guarantee Enron Canada 4

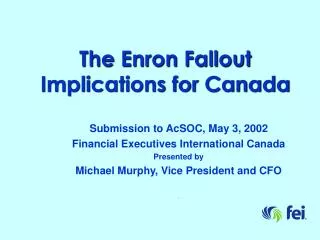

Alberta C$300mm Pre-pay 2 BF Equity Capital RBC DS C$300mm Day 365 Contract Settlement AECO Mar 02 Index = C$6/GJ vs Fixed @ C$5/GJ Annual volume: 60,000,000 GJ C$300mm + floating int C$300mm loan C$300mm + floating int • Day 365 Contract Settlement MAR 02 Index = $6/GJ • SWAP 1 • Day 1 Enron Canada receives pre-pay = C$300mm (funded by RBC DS through BF Equity Capital • Day 365 Settlement Enron Canada pays Swapco $360mm • Monthly interest of 8% paid as spread of C$0.40 on floating index (paid back up to RBC via BF Equity Capital) • SWAP 2 • Day 365 Settlement Swapco (box 2) re-pays C$300mm up to BF Equity Capital • Day 365 Net financial settlement of C$60mm from Swapco (box 2) to RBCDS (box 3) • SWAP 3 • Day 365 Net financial settlement of C$60mm from RBC DS (box 3) to Enron Canada (box 4) • Collateral Re-hypothecation: • Weekly: Swaps are MtM to calculate bilateral margin requirement on collateral threshold of C$45mm. • Eg If FLOATING = C$6/GJ at Feb 01 • SwapCo has MtM exposure to Enron Canada (box 1) of C$60mm • C$15mm cash collateral posted by Enron Canada (box 1) to SwapCo, SwapCo posts C$15mm to RBC, RBC posts $15mm to Enron Canada (box 4) resulting in net zero cash position for Enron Canada Fixed gas pre-pay of C$300mm = C$5/GJ Enron Canada 1 Financing Swap Co 2 GJ/mth interest payment SWAP 1 Day 365 C$360mm Day 365 C$360mm Fixed gas Day 365 C$300mm SWAP 2 RBC DS 3 Fixed gas Day 365 C$300mm Day 365 C$360mm SWAP 3 Enron Corp Guarantee Enron Canada 4

Alberta C$300mm Pre-pay 3 BF Equity Capital RBC DS C$300mm Day 365 Contract Settlement AECO Mar 02 Index = C$4/GJ vs Fixed @ C$5/GJ Annual volume: 60,000,000 GJ C$300mm + floating int C$300mm loan C$300mm + floating int • Day 365 Contract Settlement MAR 02 Index = $4/GJ • SWAP 1 • Day 1 Enron Canada receives pre-pay = C$300mm (funded by RBC DS through BF Equity Capital • Day 365 Settlement Enron Canada pays Swapco $240mm • Monthly interest of 8% paid as spread of C$0.40 on floating index (paid back up to RBC via BF Equity Capital) • SWAP 2 • Day 365 Net financial settlement of C$60mm received by Swapco (box 2) from RBCDS (box 3) • Day 365 Settlement Swapco (box 2) re-pays C$300mm (C$240mm + C$60mm) up to BF Equity Capital • SWAP 3 • Day 365 Net financial settlement of C$60mm received by RBC DS (box 3)from Enron Canada (box 4) • Collateral Re-hypothecation: • Weekly: Swaps are MtM to calculate bilateral margin requirement on collateral threshold of C$45mm. • Eg If FLOATING = C$4/GJ at Feb 01 • RBC DS (box 3) has MtM exposure to Enron Canada (box 4) of C$60mm • C$15mm cash collateral posted by Enron Canada (box 4) to RBC DS, RBC DS posts C$15mm to SwapCo, SwapCo posts $15mm to Enron Canada (box 1) resulting in net zero cash position for Enron Canada. Fixed gas pre-pay of C$300mm = C$5/GJ Enron Canada 1 Financing Swap Co 2 GJ/mth interest payment SWAP 1 Day 365 C$240mm Day 365 C$240mm Fixed gas Day 365 C$300mm SWAP 2 RBC DS 3 Fixed gas Day 365 C$300mm Day 365 C$240mm SWAP 3 Enron Corp Guarantee Enron Canada 4