Preferred Stock Valuation

400 likes | 577 Vues

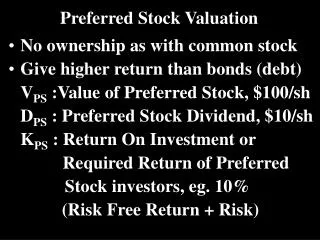

Preferred Stock Valuation. No ownership as with common stock Give higher return than bonds (debt) V PS :Value of Preferred Stock, $100/sh D PS : Preferred Stock Dividend, $10/sh K PS : Return On Investment or Required Return of Preferred Stock investors, eg. 10%

Preferred Stock Valuation

E N D

Presentation Transcript

Preferred Stock Valuation • No ownership as with common stock • Give higher return than bonds (debt) • VPS :Value of Preferred Stock, $100/sh • DPS : Preferred Stock Dividend, $10/sh • KPS : Return On Investment or • Required Return of Preferred • Stock investors, eg. 10% • (Risk Free Return + Risk)

Stocks • Calculation: • ROI = KPS= DPS = 10 =0.1= 10% • VPS 100 • VPS= DPS = 10 =100 • kPS 0.1

Stocks • If require ROI = 12% = Kps • DPS = 10 • VPS= DPs= 10 = 83.3 • kps 0.12

Common Stock Valuation • Pt = Stock price at time t • Dt = Dividend at time t • D0 = Dividend at time t = 0 (just paid) • D1 = Dividend at time t = 1 (1 year • from today) • KS = Return on Investment on Common • Stock

Common Stock Valuation • D1 = D0 ( 1 + g )1 • D2 = D0 ( 1 + g )2 • where g : expected annual growth (or • increase) in dividend (%)

Common Stock Valuation • Example: • Find Dividend (given g = 5%) • D0 = $10 • D1 = 10.5 = 10 (1 + 0.05)1 = D0 (1+g)t • D2 = 11.03 = 10 (1 + 0.05)2 or • 10.5 (1 + 0.05)1

Common Stock Valuation • Example: • FV = ? • 10% • PV = 100 n=1 • FV = PV ( 1 + i )n PV= FV • ; ( 1 + i)n

Common Stock Valuation INPUTS 1 10% -100 0 N I/YR PV PMT FV 110 OUTPUT

Common Stock Valuation • Example: • D1=10 P1 = 100 • i=?% • PV = 100 1 yr • KS = 10 / 100 = 10%

Common Stock Valuation INPUTS 1 100 -10 -100 N I/YR PV PMT FV 10% OUTPUT

Common Stock Valuation • Example: • D1=10 P1 = 100 • KS = 10% • 1 yr • P0= PV = ?

Common Stock Valuation INPUTS 1 10% -10 100 N I/YR PV PMT FV 100 OUTPUT

Common Stock Valuation • P2 • D1 D2 • 1 yr 2 yr • P0 = ? • P0 = D1+ D2+ P2 • (1+k)1 (1+k)2 (1+k)2

Common Stock Valuation • P0= D1+ D2+ D3++ Dn+ Pn • (1+k)1 (1+k)2 (1+k)3 (1+k)n (1+k)n • If n ¥ • Example: Pn = 100/sh = FV, • n = 99 • k = 15% • PV = ?

Common Stock Valuation INPUTS 99 15% 0 -100 N I/YR PV PMT FV 0.00009793 OUTPUT

Common Stock Valuation • P0= D1+ D2+ D3++ Dn+ Pn • (1+k)1 (1+k)2 (1+k)3 (1+k)n (1+k)n • If n ¥, Pn0 • (1+k)n • Therefore, • P0= D1+ D2+ D3++ Dn • (1+k)1 (1+k)2 (1+k)3 (1+k)n

Common Stock Valuation • P0= D1+ D2+ D3++ Dn • (1+k)1 (1+k)2 (1+k)3 (1+k)n • can be written as: • P0= D0(1+g)1+ D0(1+g)2+ D0(1+g)3 • (1+k)1 (1+k)2 (1+k)3 • ++ D0(1+g)n • (1+k)n

Common Stock Valuation • P0=D0[(1+g)1+ (1+g)2+ (1+g)3+ (1+g)n] • (1+k)1 (1+k)2 (1+k)3 (1+k)n • (1+k)P0=D0[1 +(1+g)1+(1+g)2+(1+g)n-1] • (1+g) 1+k 1+k 1+k • (1+k)P0- P0= D0[1- (1+g)n] • 1+g1+k

Common Stock Valuation • If n ¥, and k > g, • (1+g)n0 • 1+k • then, (1+k)P0 - P0= D0 • 1+g • P0[ 1+k - 1] = D0 • 1+g

Common Stock Valuation • P0[ 1+k-1-g ] = D0 • 1+g • P0[ k-g ] = D0 • 1+g • P0 =D0(1+g) =D1 • k-g k-g

Common Stock Valuation • Example: • g = 5%, D0 = 10 • D1 = 10.5 (10 x 1.05) • ks = 18% • What is the value of the stock? • P0 = D1 =10.5 =80.77= PV • k-g 0.18 - 0.05

Common Stock Valuation • If the stock is purchased at $90, K=? • 90 = 10.5 P0 = D1k-g= D1 • k - 0.05 k-gP0 • k = D1+ g • P0 • k = 17% • Dividend/Stock Price = Dividend Yield

Stock Markets and Stock Reporting • I. Stock Markets • A. New York Stock Exchange (NYSE) • B. American Stock Exchange (AMEX) • C. Over-the-counter (OTC) markets • D. Smaller regional markets • II. Stock Market Reporting • 52 Weeks Yld. P-E Sales Net • High Low Stock Div. % Ratio 100s High Low Close Chg. • 1757/8 102 IBM 4.40 3.8 16 27989 1181/4 1151/4 1171/4 +13/4 • Dividend yield = D/P • = $4.40 / $117.25 = 3.8%

Common Stock Valuation • FV = 110 • i=10% • PV = 100 n=1yr • FV = PV ( 1 + i )n

Common Stock Valuation • PV(1+i)n = FV • 100 (1+0.1) = 110 • 100 (1+0.1)2 = 121 • 100 (1+0.1)3 = 133 • FV • PV = (1+i)n Value of Stock

Common Stock Valuation • Discounted Valuation Approach • Know FV • Calculate PV (price you have to pay now) or (value of stock or bond) • Bond debt - interest • Stock - dividend

Common Stock Valuation • Own stock one year: • d1 P1 • 1 year • k% • Po • d1 P1 • Po = (1+k)1 + (1+k)1 • Appraisal Value of Stock

Common Stock Valuation • 2 years: P2 • D1 D2 • 1 k% 2 • P0 • P0 = D1+ D2+ P2 • (1+k)1 (1+k)2 (1+k)2

Common Stock Valuation • P0= D1+ D2+ D3++ Dn+ Pn • (1+k)1 (1+k)2 (1+k)3 (1+k)n (1+k)n • Make Assumptions: • 1)If n ¥Pn • (1+i)n 0 • 2)If D1 = Do(1+g)1 Assume dividend • D2 = Do(1+g)2 rate increases at • Dn = Do(1+g)n g rate.

Common Stock Valuation • Example: • Do = $10 • g = 5% • D1 =10 (1+0.05) • D1 = $10.5

Common Stock Valuation • Equation : • (1+k)P0=D0[1 +(1+g)1+(1+g)2+(1+g)n-1] • (1+g) 1+k 1+k 1+k • P0= D0(1+g)1+ D0(1+g)2+ D0(1+g)3 • (1+k)1 (1+k)2 (1+k)3 • ++ D0(1+g)n • (1+k)n

Common Stock Valuation • Equation : • P0=D0[(1+g)1+ (1+g)2+ (1+g)3+ (1+g)n] • (1+k)1 (1+k)2 (1+k)3 (1+k)n • Equation : • (1+k)P0- P0= D0[1- (1+g)n] • 1+g1+k

Don’t Forget... • k = ROI (%) = Required Return on Investment • g = Dividend Growth

Common Stock Valuation • If n ¥, and k > g, then • (1+g)n0 • 1+k • and, (1+k)P0 - P0= D0 • 1+g • P0[ 1+k - 1] = D0 • 1+g

Common Stock Valuation • P0[ 1+k-(1+g) ] = D0 • 1+g • P0[ k-g ] = D0 • 1+g • P0 =D0(1+g) =D1 • k-g k-g

Common Stock Valuation • P0 =D1 • k-g • Only when n -- ¥ AND k>g • Gordon Model or • Constant Dividend Growth Model • k-g = D1/ Po k = D1/ Po + g

Just a Reminder... • KR = risk free + risk premium • = Rf + b (Rm - Rf) • market return • *use S&P 500 • risk-free index • *use T-Bill Volatility • Rm - Rf = Market Risk Premium

Common Stock Valuation • Example: • Do=Paid Dividend=$5/share • g=Dividend Growth=5% • KR=Required Return=10% • pay for stock now • Do(1+g) $5(1+0.05) • Po= KR - g =0.1 - 0.05 = $105

Common Stock Valuation • Value of Stock = $105 (appraisal value) • Stock Price = $110 • *Don’t buy the stock because the stock is over valued. (too expensive)

Common Stock Valuation • KE = D1/ Po + g =Expected Return • (Po = Stock Price = $110) • Do (1+g) $5(1+0.05) • KE = + g = +0.05 • Po $110 • KE = 9.7% (Expected Return) • KR = 10% (Required Return) • Therefore, do not purchase