Download

1 / 6

60 likes | 145 Vues

Explore promising short-selling opportunities in Hong Kong developer stocks and the potential in Thailand's market. Discover the overlooked strengths of Southeast Asia and the transformative trends in China for optimal investment strategies.

E N D

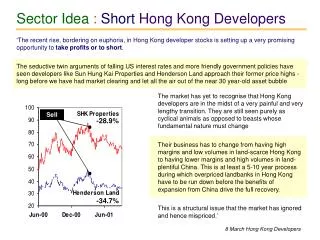

Sector Idea: Short Hong Kong Developers ‘The recent rise, bordering on euphoria, in Hong Kong developer stocks is setting up a very promising opportunity to take profits or to short. The seductive twin arguments of falling US interest rates and more friendly government policies have seen developers like Sun Hung Kai Properties and Henderson Land approach their former price highs - long before we have had market clearing and let all the air out of the near 30 year-old asset bubble The market has yet to recognise that Hong Kong developers are in the midst of a very painful and very lengthy transition. They are still seen purely as cyclical animals as opposed to beasts whose fundamental nature must change Their business has to change from having high margins and low volumes in land-scarce Hong Kong to having lower margins and high volumes in land-plentiful China. This is at least a 5-10 year process during which overpriced landbanks in Hong Kong have to be run down before the benefits of expansion from China drive the full recovery. This is a structural issue that the market has ignored and hence mispriced.’ Sell -28.9% -34.7% 8 March Hong Kong Developers

Market Idea: Thailand ‘About To Come Right’ Dollar Adjusted Indices • '7-Year Bear Market Ending' • '5-Year Bull Market Ahead' • 'Solid Positives Ignored' • Misconceptions • - Economy Stalling - Reform - Earnings - Market and Value - Politics • Thailand's Strengths SET STI Hang Seng Source: Reuters September 2000

Big Idea: Overweight Southeast Asia • Overweight Southeast Asia - we are not joking - for its relatively defensive qualities until the US recovery is in sight. • Domestic resilience, supported by recovering natural resource-based incomes and by much higher local content in Southeast Asian exports, is likely to see the region in the second half again outperform Northeast Asia. Index Targets: 2001-2003 Below Below Below 16 Aug 01 End 01 End 02 End 03 % Chg % Chg % Chg High High High 19.5 (59.0) 57.2 (46.0) 88.7 (35.2) Thailand 318 380 500 600 9.4 (57.9) 28.3 (50.7) 43.4 (44.9) Philippines 1,325 1,450 1,700 1,900 10.1 (35.2) 26.1 (25.8) 37.6 (19.0) Indonesia 436 480 550 600 22.0 (37.1) 37.2 (29.2) 37.2 (29.2) Malaysia 656 800 900 900 Source : Research-Works estimates 2 Aug Overweight SE Asia

2001’s Unexpected Outperformer Asia Stockmarket Relative Performance 130 110 3 90 Korea,Taiwan 70 Safe Havens ASEAN 4 Jan-01 Jul-01 Source: CEIC Big Idea: Overweight Southeast Asia Getting Exports In Perspective • Why Overweight Southeast Asia? : Defensive • Political events are giving Southeast Asians a sense that after four very difficult years they have a second chance to recover from the Asian Crisis and its after effects. % of Exports Natural Resources * % of Exports Natural Resources * % of Exports * 0 20 40 60 80 100 • Seek relative safety of exporters with higher local content : natural resource-rich SE Asian economies • SE Asia's commodities with +90% local content show signs of ending 10-15 year declines : palm oil up 50%, coconut oil up 30% : major income sources in Malaysia, Indonesia, Philippines. • Tourism a consistent hard dollar earner, beneficiary of improving social stability 0 20 40 60 80 100 Indonesia Indonesia 78.8 78.8 Thailand 64.7 Thailand 64.7 Malaysia Malaysia 55.1 55.1 Singapore Philippines 50.9 Philippines 50.9 Singapore 26.2 26.2 Korea Korea 11.2 11.2 Taiwan Taiwan 4.4 4.4 * Adjusted for local content and value-added in exports * Adjusted for local content and value-added in exports 2 Aug Overweight SE Asia

Big Idea: China • ‘The most important long term decisionthat fund managers can make this year is to spend much more time getting to know China. Not only is it nearly 30% of regional market cap but 13 China Mega Trends will support some of Asia's best performance. Investors' perceptions lag reality or are fogged by out-dated experience. No longer can China be ignored.’ First Time Since 1949… • Mega Trends will change China beyond recognition: Historic Moment In 2002 • Private Sector Dominance: overtakes state in 2002 • Private Property: critical to private sector-led economy • Housing Reform: creates instant wealthMortgage Market Developing: 20% of urban new loans • Consumerism Taking Off: $500 bn market larger than Korea, Taiwan, Hong Kong and Singapore combined • New Mindsets: post Cultural Revolution generation • End of Deflation: investment, consumption boosted • More Taiwans: Taiwan companies pouring capital and people into Mainland at an accelerating rate % Share of Industrial Output 80 70 Private Sector 60 50 50 40 TVE 30 20 State Enterprises 10 0 80 90 94 98 02E Research-Works Forecast Source: 2000 China Statistical Yearbook 15 May China – The Most Important Decision

Macro Idea: Asian Currencies Broad Dollar Index • ‘The recent weakness of Asian currencies, with everything in thrall to the strong US dollar, strikes us as a misconception about what lies ahead over the rest of 2001’ • ‘Don't assume strong US dollar is permanent’ • ‘US imbalances unlikely to be ignored forever’ • ‘Only 20-30% US dollar fall can rebalance trade’ • ‘China could surprise: more flexibility, appreciation’ Dollar Weakness Ahead 19 April Asian Currencies