Download

1 / 20

200 likes | 363 Vues

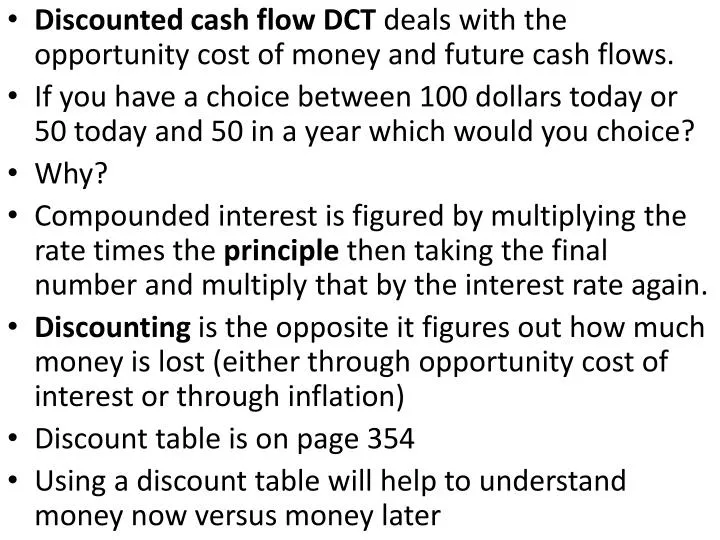

Discounted cash flow DCT deals with the opportunity cost of money and future cash flows. If you have a choice between 100 dollars today or 50 today and 50 in a year which would you choice? Why?

E N D

Discounted cash flow DCT deals with the opportunity cost of money and future cash flows. • If you have a choice between 100 dollars today or 50 today and 50 in a year which would you choice? • Why? • Compounded interest is figured by multiplying the rate times the principle then taking the final number and multiply that by the interest rate again. • Discounting is the opposite it figures out how much money is lost (either through opportunity cost of interest or through inflation) • Discount table is on page 354 • Using a discount table will help to understand money now versus money later

Figure out the present value if the interest rate is 1% and we expect a payment of 45000 in 6 years time. • If the following money is expected on a 3000 dollar investment what would be the NPV for the investment. Discount rate 4% • Year 1 1500 • Year 2 1000 • Year 3 700 • What would be the value of 1000 dollars saved over the course of 3 years? Interest rate of 1.5%. • What is the value of the interest after 3 years

Garth owns a T.V. station in Athens. He is offered payment for a commercial of 700,000 which is more than double what he normally receives but the money will be paid over the course of six years in the following amounts. 10% is the current discount rate in Greece. • Year 1 50000 year 4 100000 • Year 2 50000 Year 5 100000 • Year 3 50000 Year 6 100000 • Year 7 250000 what is the NPV of his collection.

Net Present Value works as an extension of ARR (accounting rate or return). This figures how much money a business will make from an investment after we count the opportunity cost of not putting the money in the bank for interest. • The problems with this method are that interest rates are not always stable. • FOR THE IB TEST (and almost any test) a discount table will be provided. Also make sure to keep in mind to do calculations to two decimal places.

Using the discount table at a rate of 2% figure out the NPV. • Johnson wants to buy a new car Minnesota to help him in his part time job as a taxi driver. The cost of the car will be 20000 and he is expecting the following returns on his investment not including his time. He expects the car to have a residual value of 5000 dollars when he finishes his fourth year of collage. • Year 1 4000 • Year 2 6000 • Year 3 7000 • Year 4 4000

Peter Storm has conducted a financial analysis of the WarmBreezes’ expansion projects. At this stage it would only be possible to fund one of the two proposed projects. Inflation in the Caribbean is a problem and the costs of capital comparatively high at 14%. Peter presents the following figures to Joseph and Manjit for their consideration. Details of cash inflows have only been presented for 6 years as Peter considers that financial information after this date is likely to be highly inaccurate, especially as the Caribbean economies had been unstable in recent times. Predictions are based on an average occupancy rate of 75% for the cottages for the first year, rising to 85% in years 4, 5 and 6. • Peter has decided that the investments will only be considered if they meet the following criteria: • Payback 3.5 YearsAverage Rate of Return 35%Net Present Value $2m • OPTION 1OPTION 2 Commercial centre New cottages$m$mInitial Cost 8.4 4.4Cash inflows at end of: Year 1 1.6 0.8 Year 2 2.8 1.4 Year 3 3.4 2.0 Year 4 3.6 2.4 Year 5 4.0 2.3 Year 6 4.2 2.6 • Present value (PV) of $1 receivable at an annual rate of 14% at the end of: • 1 Year 2 Years 3 Years 4 Years 5 Years 6 Years$0.877 $0.769 $0.675 $0.592 $0.519 $0.456 • (a) Using the information provided, calculate the Payback, Average Rate of Return and Net Present Value, for both Option 1 and Option 2, and state whether the options satisfy Peter’s criteria for investment. • (b) Using the investment appraisal information you have just calculated and additional financial and non-financial information provided in the case study, select an expansion option and justify your choice. • (c) Using relevant examples, consider to what extent external factors may affect the accuracy of the figures presented by Peter Storm.

Budget is a financial plan for revenue and expenditure for a business or department. Helps to give understanding to how to make targets for costs, profits and sales. Also helps to organize a business. • A budget helps an organization or department to better understand their objectives within an organization. If a department cannot stay within their budget then corrective measures will be taken. • A budget needs to be realistic and should be monitored to make sure a department is using it’s resources correctly. • A budget holder is someone in the business or more likely in a department (usually the head of department) who is in charge of managing and keeping expenditures on track.

Types of budgets • Sales budget – planned volume and money from sales • Staffing budget – number and cost of labor for a business or department • Production budget – helps to understand capacity utilization by watching costs of stock as well as the stock level. Also used to keep an eye on overhead costs • Marketing budgets – how will money be spent on either above or below the line promotions. • Zero budgeting – all departments have a budget of 0 and need to justify and money they ask for. Is good that makes watching expenditures easy but requires a huge amount of time on administration and causes bureaucracy. • Flexible budgets – Allows business or more likely departments to change their budgets when a change in demand is happening All budgets in a business will be put in the master budget which is run by the CFO of a business.

When the following are done a business should run much more efficiently. • Planning and guidance • With a well planned budget then a business or department will know if they are making their spending and trading objectives Key questions a business asks during the planning stages of a budget. • How much should a business spend on marketing in the coming year • How many workers are needed/how much will they cost • How much money is set aside as a contingency fund?

Coordination – • Different departments will be allocated different amounts of money depending on the nature of the department and the business as a whole. (marketing departments of a cleaning service may receive a larger budget then the production department) • Department goals need to be interconnected so a business can run smoothly. If the marketing department tries to boost sales above what production can do then the business image will suffer. • Budgets will help everyone to understand what money they will be allocated.

Control • A budget will help different departments from overspending causing liquidity and cash flow problems. • Many businesses will allow a budget holder to regulate the spending in their department (NOT MICROMANAGE). This helps to have money spent where it is really needed. • If the department cannot meet their budget requirements then corrective measures can be made.

Motivational • Having the budget holder make their own budget will help to motivate the manager. Also the manager will more than likely involve his/her staff in the budget process. • This will give non-financial motivation encourage team-working and improve employee-employer relations. All resulting in higher productivity. • Because departments and sub departments are expected to meet their budget needs rewards and punishments can be given out which will increase accountability.

Setting a budget – (many different ways to set a budget) • Available finance – the more money a business has the more potential each budget holder can get • Historical data – Many budgets will be set according to what happened the year before. If the economy looks positive then more money may be allocated. • Organizational objectives – during times of expansion budgets for marketing and production will need to be raised. • Benchmarking – Setting a budget that is close to a competitor. • Negotiations – many times budgets are set between the senior managers and the budget holders

Limitations of budgeting • Any quantitative factor will have the problems of the unforeseen making the best budgets useless. • Managers will always overestimate their budgets which can cause waste. • If a budget holder does not spend all that they thought they would then the management will usually just reduce their budget for the next year. (no reason to try and save money) • In some cases senior managers give out budgets without checking with budget holders about what they need. • Low budgets can lead to: poor raw materials, job cuts or losses, bad credit from suppliers which can all lead to a drop in quality and corporate image. • Making implementing and monitoring budgets takes time • Budget holders compete for the limited resources which can be wasteful • Qualitative factors of a business are ignored: CSR, employee training/nonfinancial motivation and the changing environment of the business world • Budgeting should not be used as a management tool some critics say because that make things too inflexible.

Variance analysis • Budgetary control is about taking corrective measures to make sure that budgeted performance equals actual performance. • When the actual outcome does not match the budget for a business or department a Variance is created. • Variance = Actual outcome – Budgeted outcome • Budget holders are expected to monitor the variance in their departments. If they have a variance either positive or negative they will be asked for an explanation. • Many things can cause a variance that is not a budget holders fault: costs of (fuel, labor, raw materials …) while other such as inefficiency cannot.

Two types of variance: • Favorable variance – different ways this can happen but the overall thing is if the variance is good for the company it is favorable. (Can happen from a department spending less or a business selling more) • Adverse variance (Unfavorable variance) - different ways this can happen but the overall thing is if the variance is bad for the company it is adverse. (Can happen from a department spending more or a business selling less) • Variance can be expressed as a percentage (take the little number divide by the big one) • DO NOT USE VARIANCE AS POSITVE OR NEGATIVE ONLY FAVORABLE OR ADVERSE

Budgeting and Business Strategy • Budgets help managers understand their costs and objectives. Controlling their own budgets gives motivation to managers to keep them in line. • Authoritarian or Theory X style managers will tend to have a zero budget process so that the senior managers can control all aspects of the money. • Democratic, Laissez faire or theory Y style managers will usually trust managers and employees to make their own budgets which can be motivational.

SMART budgeting – budgets should be • Specific – Budgets should be in with the objectives of the company and have exact figures • Measurable – It is important to be able to hold a budget holder accountable for their success and failure • Agreed – Budgets should be set with all participates being involved. • Realistic – only if a budget is set properly can it motivate managers to make it happen. Underfunding means will make output harder overfunding may make people not work as hard and become complacent • Time constrained – Budgets have a time constraint by nature (some businesses let departments carry surpluses forward while others do not

Some budgets are set in stone and can be a problem for a business to react to internal and external changes. Opportunities may be lost or a crisis might not be dealt with very well. • Budgets can be set wrongly if sales forecasts are made on unrealistic numbers. Garbage in Garbage out. • Budgets give senior managers an extreme amount of power that can be exploited for personal gain. • In the end Budgets are an extremely important tool for any business and they should used to motivate and make a business as efficient as possible.