FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT. Budgeting and accounting in DOP. Broad outline of a/ cs. Consolidated Fund of India. Revenue. Other than Revenue. Receipts. Expenditure. Capital. Public Debt. Loans & Advances. Receipts. Expenditure. Appropriations to Contingency Fund. Payments. Receipts.

FINANCIAL MANAGEMENT

E N D

Presentation Transcript

FINANCIAL MANAGEMENT Budgeting and accounting in DOP

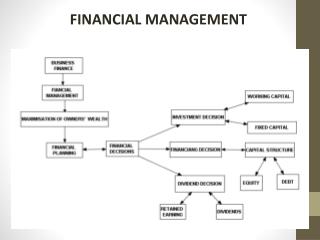

Consolidated Fund of India Revenue Other than Revenue Receipts Expenditure Capital Public Debt Loans & Advances Receipts Expenditure Appropriations to Contingency Fund

Payments Receipts Longevity Constitutional Developmental Classification of Transactions Revenue & Capital Plan & Non Plan Voted & Charged

IMPORTANCE OF BUDGETING • Efficient use of Resources to achieve Government objectives • Induces management/Govt. to think systematically about future. • Provides a medium for communicating the plans of Government /Ruling Party’s policies • A control Instrument

BUDGETING IN GOVT. OF INDIA • A constitutional responsibility of the Executive • A tool of legislative control over public finances • An annual affair • Presented generally on the last day of February • Separate Budget for Ministry of Railways since 1924 • Contains financial statement embodying the estimated receipts and expenditure.

ANNUAL FINANCIAL STATMENT • Budget- A Statement of estimated receipts and expenditure to be laid before Parliament • Shows the receipts and payments under three parts • (i) Consolidated Fund of India • (ii ) Contingency fund of India • (iii) Public Account • Distinction of receipts and payments on Revenue Account & Capital Account • Distinction between Charged expenditure and Voted Expenditure

Voted and Charged Expenditure • The estimates of expenditure embodied in the annual financial statement shall show separately- 1. Charged Expenditure: The sums required to meet expenditure described by this Constitution as expenditure charged upon the Consolidated Fund of India. 2. Voted Expenditure: The sums required to meet the expenditure proposed to be made from the Consolidated Fund of India. - Art. 112 of Constitution of India

Charged Expenditure • Expenditure on and related to -The President of India and his Office - Chairman, Deputy Chairman of the Council of States. - Speakers, Deputy Speaker of House of People. - Judges of Supreme Court & High Court - Comptroller and Auditor General of India • Debt liability of Govt. of India and related charges. • Sums required to satisfy a judgment, decree, award • Any other expenditure declared by Parliament. • Estimates relating to Charged Expenditure not to be submitted to the vote of Parliament. - Art. 112

BUDGET IN PARLIAMENT • Article 112 to 116 deals with the provisions with regard to Union Budget • Article 202 has similar provisions with regard to State Budgets • Supremacy of LokSabha in financial matters Contd..

BUDGET IN PARLIAMENT-contd. • Presentation of Budget with Budget speech • Discussion on the Budget • Cut Motions • Guillotine • Scrutiny by Departmentally related Standing Committee • Appropriation Bill – Article 114 • Vote on Account • Supplementary & Excess Demands for Grants Article 115

DEMAND FOR GRANTS • Expenditure other than “charged expenditure” on Consolidated Fund of India to be submitted in form of Demand for Grants – Article 113 • Generally one demand in respect of each Ministry • Identification of Demand with Demand number • Break-up of expenditure in to plan and non-plan • Demand for Grants is presented at two level • Main Demand & Detailed Demand • Main Demand contains estimates on Major head wise • Detailed Demand based upon full accounts classification

BUDGETARY CONTROL • Responsibility for Control of expenditure • A Grant is valid for the financial year • No expenditure in excess of grant except after obtaining supplementary grant • Monitoring of physical progress of schemes progressive expenditure • Maintenance of liability register • Surrender of Savings

System of Accounts of DOP • Accounts of DOP form part of general accounts of the Government of India; • Accounts of DOP are built on the same general plan of accounts of the Government of India; • DOP Receipts & Expenditure are recorded under various Major Heads-suitably divided & sub divided as per nature of transactions.

Accounts and Budgeting • Primary Accounting Unit • Role of PO & RMS Accountant and APM (Accounts) in HPO • Importance of Accounts Branch in HPO • Linkages with other branches in the HPO • Role of Accounts Section of HRO / RMS Division • Role of Accountant in the Divisional Office

Relevant Texts • Delegation of Financial Powers Rules • General Financial Rules/ P&T FHB Volume I and Volume II. • List of Major and Minor Heads of Account as prescribed in Appendix –V of Postal Accounts Manual Vol. I. • Schedule of Financial Powers in the Department • Instructions / Orders issued then and there

Accounts Classification • To identify basic similarities in Government operations • To organise individual transactions into relatively homogeneous categories • To provide meaningful information on the nature, composition and impact of these transactions

Accounting in DoP • BO – • BO Accounts –BO Daily Account to SO. • BO Slips from SO to BOs • SO – • SO Accounts – BO Summary at SO- SO Daily A/c to HO • SO Slips from HO to SOs • HO • Treasurer’s Cash Book- HO Summary-SO Summary at HO - HO Cash Book – Monthly HO Cash Account. • Cash and Stamp balances, CSD Supply of Stamps - Cash in Transit - Postmaster’s Balance Sheet, • Banking transactions- Treasury Pass Book-Register of Cheques received and cleared- Register of Cheque Books received

Accounting in DoP -Contd.. • HPO Monthly Cash Account, Schedules, Vouchers • HRO –Cash Book- Cash Abstract containing details viz. Pay and allowance, Permanent Advance for contingencies, Permanent Advance for Postage Stamps and Misc. receipts. • Account Current of MMS and Civil Division • Other DDOs- RMS, MMS,PSD, CSD, CO,RO, Disp., PTC • Classified Abstracts – Detail Book- Transfer Entries – Consolidation – Combined Transfer and Ledger Entries- Circle Abstract. • General Abstract for entire department at Directorate • CGA (Finance Ministry) for entire Country.

Functional Classification • A 6 tier - 15 digit classification structure: Function Major Head (4) Sub Function Sub major head (2) Programme Minor Head (3) Scheme Sub- head (2) Sub Scheme Detailed Head (2) Item of Expenditure Object Head (2)

An example Major Head – 3201 – Postal Services Sub Major Head – 02 – Operation Minor Head– 003 – Training Sub Head – 01 – Operational Training Detailed/Object heads (01) Salaries (02) Wages (03) Overtime Allowances (04) Pensionery Charges (06) Medical Treatment (11) Travelling Expenses (13) Office Expenses (14) Rent, Rates & Taxes (21) Supplies & Materials (26) Adv. Sales & Publicity. (28) Payments for prof. Service (50) Other Charges (64) Write off / losses

Major Heads of Account mostly relevant to DoP • 1201 - Revenue Receipts. • 3201 - Revenue Expenditure • 5201 - Capital Expenditure. • 0049 - Interest Receipts • 2016 - Audit • 2029 - Interest Payments • 2071 - Pension and other Retirement Benefits • 7610 - Loans to Government Employees • 8001 - National Savings Deposits • 8002 - National Savings Certificates • 8009 - State Provident Funds • 8446 - Postal Deposits • 8553 - Postal Advances • 8661 - Suspense Accounts • 8781 - Money Orders

Object Heads at Divisional Level 01. Salaries[3201-01-101-03-01-01 for Postal Division] 02. Wages 03. Overtime Allowance 06. Medical Treatment 11. Domestic Travel Expenses 13. Office Expenses [3201-01-101-03-01-13] 14. Rent, Rates & Taxes 26. Advertising and Publicity 27. Minor Works [3201-01-101-03-01-27] 28. Professional Services 50. Other Charges

(01) Salaries • Include • Pay • Allowances in all forms except OTA, Medical, TA • LTC payments including Leave encashment • Remuneration to Examiners, Invigilators • Incentives to Postal Staff • Honorarium payments • Bonus to Employees • All arrears of Pay & related allowances

Ceiling items • Ceiling items: • Overtime Allowance • Domestic Travel Expenses • Office Expenses

(02) Wages, (03) OTA, (06) Medical Treatment • Wages – includes wages of part time contingent staff, casual labourers and short duty staff . • OTA – Amount paid to a Non-Gazetted Government Servant for performing official duties beyond office hours in addition to his working hours • Medical Treatment – includes all indoor and outdoor treatment, all reimbursement of medical bills

Domestic Travel Expenses • Covers • All expenses on account of travel on duty in India including regular conveyance allowance and fixed travelling allowance • Also, TA/DA to non-official members on account of travel in India • But, excludes LTC which is part of Salaries

(13) Office Expenses • Include- • All day to day contingent expenditure for running an Office • Purchase of furniture, Office machines and equipments • Telephone, Electricity and Water charges • Stationery and Printing of forms • POL expenses on vehicles for Office Use.

(50) Other Charges • Include- • Conveyance, Packing and Freight Charges • Maintenance of gardens • Cost of plastic covers for Pass Books • Cost of Tyres & Tubes, Petrol, Oil, Grease • Establishment and other charges paid to other Government/ Department for Police Guards etc. • Other miscellaneous charges

(28) Professional Services • PS – Professional Services [or] PPSS – Payment for Professional and Special Services includes: • Charges for legal services • Consultancy fees, • Remuneration to outside Examiners, Invigilators etc., • All other types of remunerations for professional services like payment to Guest Lecture, Payment to Police Guards in CSDs, • Payment of Haulage charges to Railways, • Payment of Airway charges, • Payment for conveyance of mails through Buses etc

(14) Rent, Rates & Taxes • RRT covers • Rent paid to rented buildings • Service charges (Not Property tax) paid to Municipalities etc. • Lease charges for land

(21) Supplies & Materials • This head is to accommodate expenditure incurred on supplies obtained by the Postal Stores Depots on behalf of the various Postal Units. Eg: Uniforms, Letter Boxes, Stationery, • It does not accommodate expenditure relating to the purchases made locally by the Postal / RMS Divisions for their own Office or Offices under their control. Such expenditure is to be charged under OE or OC.

(26) Advertising and Publicity(27) Minor Works/ Maintenance • Advertising and Publicity includes the expenditure incurred on printing of publicity materials, expenditure on exhibitions & fairs. • Minor Works/ Maintenance includes the expenditure on AMC, Small civil or electrical work undertaken for the departmental buildings within the powers of Divisional Head etc.

Budgeting - “A” Statement • Correct booking of expenditure by HPOs is necessary for exercising budgetary control at Divisional Office by the SSPOs. • Monthly Statement called “A” Statement containing the bill wise classification of expenditure is prepared by the APM [Accounts] of HPO and sent to Divisional Office.

Budgeting - “B” Statement • Based on this “A” Statements of HPOs in a Division, Monthly Budget Statement called “B” Statement is prepared by the Accountant of Divisional Office for submission to R.O. • “B” Statement contains the head wise allotment, Proportionate allotment up to the month of account, Expenditure during the month and Progressive Expenditure • Perusal and review of “B” Statement by the Divisional Head will give better idea about the availability of fund, requirement of funds at a particular head of account etc.

Revised Estimate – Budget Estimate • Preparation of Revised Estimate [RE] and Budget Estimate [BE] is due in September – October of each year. • Revised Estimate is the estimate for remaining 7 months [September to March] of the current Financial Year taking in to account the actual expenditure of first 5 month [ April to August]. • Budget Estimate is the estimate for 12 months of the next financial year. • Estimation of both RE & BE should be realistic.

Factors for assessment of fund requirements and preparation of Revised Estimate / Budget Estimate ?

Assessing fund requirement • Assessment for preparation of Revised Estimate and Budget Estimate is based on: • Number / cadre of persons retired / transferred out of the establishment • Number/ cadre of persons newly recruited or transferred in to the establishment • The effect on increments/ new allowances/ new orders, if any • Specific changes compared to the last financial year, which may be resulting in reduction in expenditure [or] increase in expenditure. • Calculation of amount required for paying the pending bills of TA, Medical, OTA bills • Amount required for other liabilities like orders placed on DG S&D etc. • Specific / additional requirement for the current financial year and the ensuing financial year.

Budgeting • Allotment of funds to Divisional Office is done by CO/ RO • Only Divisional Offices are dealing with the budgeting issues and not the HPOs [Except in the Gazetted GPOs / HPOs, to which separate allotment is given by the CO / RO] • Divisional Head is therefore having the responsibility of correct budgeting for all the units under the Division

Budgeting • Proper and timely utilization of allotted funds is necessary so as to avoid • Rush of expenditure • Irregularity in the procedures to be followed resulting in objections by the higher authorities and the Audit Parties. • Utilization of funds on non-priority items [or] issues, which may create additional problems. • Budget Register is to be maintained and review of allotment vs. expenditure done periodically (especially in Ceiling Items).

Anticipated Final Grant • Preparation of Anticipated Final Grant [AFG] Statement is due in the month of February. • This Estimate is prepared taking in to account the progressive expenditure for the first 10 months of financial year [April to January]. • AFG Statement is prepared so as to accurately work out the actual requirements, to surrender the excess allotment, if any and to demand absolutely necessary additional funds, if any.

Anticipated Final Grant • Only additional allotments [Final Grant], if any, will be communicated for meeting the expenditure at the fag end of the financial year, with reference to the AFG demand. • When there is no allotment, expenditure should not be resorted to, at any point of time. • Divisional Head is responsible for any savings on / excess expenditure over the funds allotted. • Such position will invite objections later date.

Some of the Plan activities • Project Arrow , MNOP • Heritage Building, New Building, Boundary wall • Promotion Publicity and Brand visibility • Training activities • Creating Training Facilities • Infrastructure Equipment to BOs • Promotion of Philately & Operations • Procurement of Equipment for speed post intra-circle hubs as part of Mail Network Optimization Project