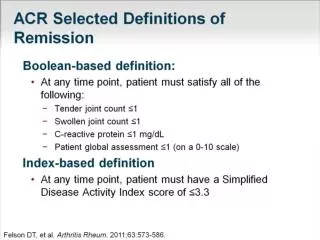

TUITION REMISSION POLICY

90 likes | 250 Vues

TUITION REMISSION POLICY. February 2009. Human Resources. Introduction Tuition Remission General Policy Human Resources Responsibilities Determine Eligibility Tuition Remission Fees Process of Tuition Remission Form Verify Dependent Health Coverage

TUITION REMISSION POLICY

E N D

Presentation Transcript

TUITION REMISSION POLICY February 2009

Human Resources • Introduction • Tuition Remission General Policy • Human Resources Responsibilities • Determine Eligibility • Tuition Remission Fees • Process of Tuition Remission Form Verify Dependent Health Coverage Presenter: Tiffany Smith, Human Resources Assistant

Financial Aid • Office of Financial Aid Responsibilities • Financial Aid Timelines • January 1st – Begin to Apply for Financial Aid • March 2nd – FAFSA Deadline • May 1st – Financial Aid Award Letters • May & June – Make Appointment with Financial Aid Office • May & June – Tuition Remission Requests for Traditional Undergraduate Students Due to Human Resources • July & August – Receive Revised Award Letters • Financial Aid Application Process • Eligibility Criteria for Cal Grants • Examples of Financial Aid Programs Presenter: Jason Neal, Associate Director Financial Aid

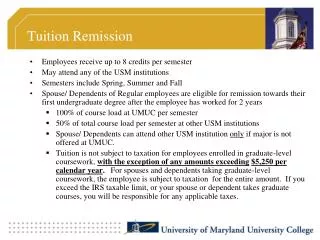

Student Accounts • Student Accounts Responsibilities • Student Account Records in Banner • Timing of Tuition Remission Posting • On-line Access to Review Banner Record • Book Vouchers Program • Eligibility Requirements • General Process • Example of Tuition Remission Presenter: Andrea Pluth, Student Accounts Systems Specialist

Tuition Remission Example: Tuition and Fees: $13455.00 Lab Fee: +$100.00 ________________________________________________________________________________________________________________ Total Due: $13,555.00 Tuition Remission: <13,215.00> Pell Grant: <$1000.00> __________________________________________________________________________________________________________________ Balance: <$660.00> This amount is available to the student for a book voucher

PAYROLL DEPARTMENT • Taxability of Tuition Benefits • The University of La Verne’s Tuition Remission Program intends to comply with the tax provisions of the Internal Revenue Code (IRC) Sections 127 and 117(d). Under Section 117(d), undergraduate tuition reduction provided to the employee, the employee's spouse or dependents as defined under IRC Section 132(h) is excluded in full from gross income. Under Section 127, payments received by an employee for tuition for coursework is excludable from gross income up to $5250. This includes graduate tuition remission, but only to the maximum of $5250. These exclusions apply as long as the benefit does not discriminate in favor of highly compensated employees. Graduate tuition remission for the spouse or dependents remains taxable as no exclusion is provided under either Section 117(d) or Section 127. • Eligible employees are encouraged to obtain counseling from their personal tax consultant. • Presenter: Ani Kechichian, Payroll Manager

Questions & Answers • Important References • General Policy: www.ulv.edu/hr/s16.pdf • Tuition Remission Request Form: www.ulv.edu/hr/tuition.pdf • This presentation and related handouts will be published at www.ulv.edu/hr.