Download

1 / 0

0 likes | 298 Vues

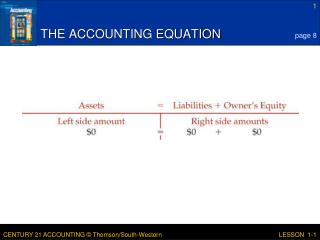

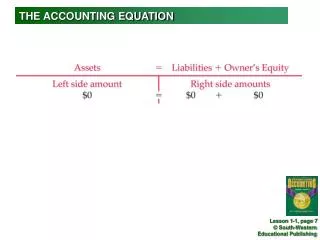

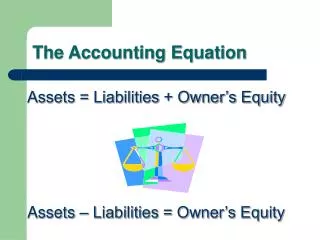

Introduction to the Accounting Environment and Accounting Equation. Chapter. 1. Learning Outcomes. Understand the importance of financial information in business Understand the basic concepts and purpose of financial accounting

E N D