Download

1 / 11

110 likes | 258 Vues

IP Global Your Property Investment Partner. Llewelyn James – Senior Consultant. Is the Help to Buy Scheme Fuelling the Next UK Property Bubble ?. Background Funding for Lending July 2012. 70 Billion GBP made available to lenders

E N D

IP GlobalYour Property Investment Partner Llewelyn James – Senior Consultant

Is the Help to Buy Scheme Fuelling the Next UK Property Bubble ? • Background • Funding for Lending July 2012. 70 Billion GBP made available to lenders • Help to Buy Phase 1 April 2013 5% deposit 20% equity loan new build only • Help to Buy Phase 2 Oct 2013 5% deposit 15 % mortgage guarantee older properties as well as new build • RBS Halifax Bank of Scotland Lloyds Santander HSBC all signed up • Two thirds of UK mortgage market 12billion available • 3 year life span Bank of England will review annually

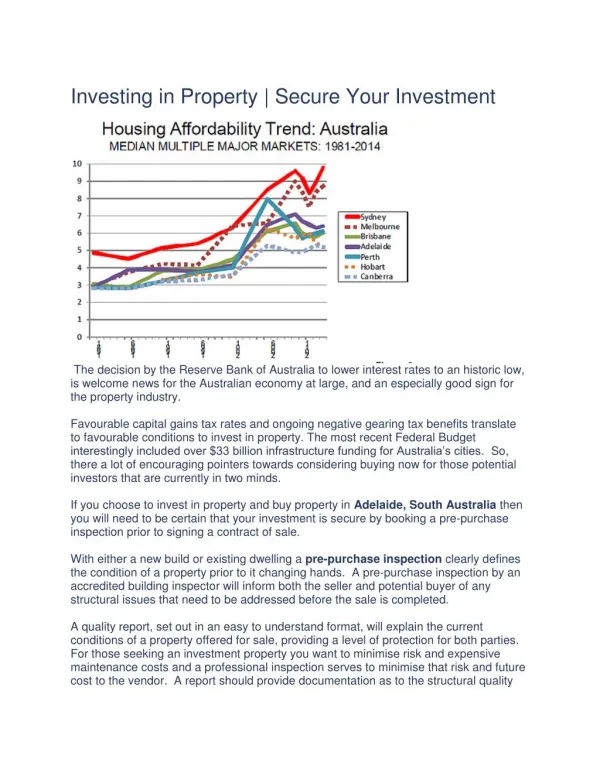

UK Property a Tale of Two Markets • Nationwide HPI: -8% in absolute terms -13% excluding London • Adjusted for inflation over 20% down • Hawthorns 25% below peak of 2007 • Other metrics: 27,000 mortgage products in July 2007 just 2,200 two years later now 5000 • Transaction volumes half the peak • Mortgage approvals 110-120K per month back in 2007 now 50-60K pm • Affordability : 1st time buyers spending 29% of take home pay on mortgage in line with average • Excluding London talk of a housing bubble not just premature but a non starter

What about London ? Global • Nationwide Building Society HPI : 8% above peak but still below peak adjusted for inflation • Only Prime Central London is at an all time high in inflation adjusted terms • Signs of possible bubble? • Return of sealed bids and gazumping in some areas • Definition of a bubble is where the price of an asset bears no relation to it’s intrinsic value • London and particularly prime central London have good fundamentals

London – A Global Economy • Ranked 5th among global cities by GDP per person – First or second in most other rankings.(Economist, 30/07/2012) • “financial services to bounce back in 2014 and together with business services drive the London economy, resulting in total GVA growth between 3% - 4% for the following five years.” (DmitriyGruzinov, Economist at Oxford Economics) • Estimated 374,000 jobs to be created in London between 2013 and 2018 – that’s 1 in 4 jobs across the UK (Xinhua, 01/05/20 • London has been voted the world’s second most important centre for the technology, media and telecommunications centre ahead of LA, Paris, Berlin and Silicon value. (Property Magazine EU, 01/02/2013) Source: Risk.net, momentum investment; DTZ, Oxford Economics; Citibank, Savills, Knight Frank, House of Commons Bulletin August 2012

Residential London Real Estate • Ranked fifth among global cities by GDP per person – first or second in most other rankings (Economist, 30/07/2012) • Estimated 374,000 jobs to be provided between 2013 and 2018 – that’s 1 in 4 jobs across the UK (Xinhua, 01/05/2013) • Transforming from a financial services economy to a multi-industry economy. Industries such as media, technology as well as business consultancy and accountancy are fuelling this change (money-marketuk, 12/01/2013) • DmitriyGruzinov, Economist at Oxford Economics, added: “… looking ahead we forecast financial services to bounce back in 2014 and together with business services drive the London economy, resulting in total GVA growth between 3 percent and 4 percent for the following five years." • Limited Supply: Current expected new stock delivery is 13,300 units per annum over the next five years – 35% below the Mayor’s target (Savills) • 35% of deals closed in cash higher than in 2007 much in Prime central London (Financial Times) • Since 2007 total international cash invested into London’s residential markets has topped GBP18 billion (property week 03/05/2013) • Increasing Demand: Over the past 18 months international buyers account for 34% of sales by volume and 49% by value (property week 03/05/2013) • Central London prices forecast to grow 31% to 2018 (knight Frank)

No bubble but what about the future? • Help to Buy is just getting going • 2 Key factors : Supply & Demand • How much uptake how many new buyers will enter the market • First phase of Help to Buy linked to supply to what extend will the rise in prices motivate developers to increase supply • 2nd Phase is not, so potentially more inflationary • UK housing supply inelastic and hasn’t built enough homes to satisfy demand since 1950’s • On the other lenders have promised no relaxation of income multiples or a return to self certification mortgages.

In Conclusion • To early to assess the full impact of Help to Buy • With only 12 Billion provided for the 2nd phase if there is a big take up the funds could run out before the scheme comes to an end • Help to Buy alone is unlikely to precipitate a full blown bubble • Confident as a consequence of the scheme UK house prices will rise over the next few years • Savills forecast of 18% price growth in the UK house market to the end of 2017 • Now is as a good a time as any to gain exposure to the UK property market just as the 2nd phase of Help to Buy gets underway

Disclaimer You acknowledge that: (i) the information contained in this document and such other material issued in connection therewith (the “Content”) are provided for information purposes only and will not be regarded as advice on securities or collective investment schemes or other financial or investment advice; (ii) the Content is not intended for the purpose of advice, dealing or trading in securities or collective investment schemes; (iii) the Content may include certain information taken from property surveys, stock exchanges and other sources from around the world; (iv) the Content is provided on an “as is” basis and by way of a summary and we do not guarantee the accuracy, completeness, or timeliness of the Content; (v) the Content may be subject to the terms and conditions of other agreements to which we are a party; (vi) none of the information contained in the Content constitutes a solicitation, offer, opinion, or recommendation by us to buy or sell any security, or provision of legal, tax, accounting, or investment advice or services regarding the profitability or suitability of any security or investment; (vii) you should not rely on the Content as the sole means of making any investment decision relating thereto and you should seek professional, independent and specific advice on any such investment decision; (viii) the property market is volatile and illiquid and property prices and rental yields may fluctuate widely or be affected by a broad range of risk factors; (ix) all plans and specifications in the Content are intended as a guide only and are subject to such variations, modifications and amendments as may be required by the relevant authorities or the relevant developer’s consultants or architects; (x) all renderings and illustrations in the Content are artists’ impressions only and all measurements are approximate subject to final survey and confirmation; (xi) the Content is not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be contrary to law or regulation; and (xii) the Content has not been authorised or approved by the Securities and Futures Commission of Hong Kong or any regulatory body of competent authority whether in Hong Kong or elsewhere. Accordingly, you assume all responsibility and risk for reliance upon and the use of the Content and, we, our agents, directors, officers, employees, representatives, successors, and assigns expressly disclaim any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) the use of the Content, (ii) reliance on any information contained in the Content, (iii) any error, omission or inaccuracy in any such information including, without limitation, financial data, forecasts, analysis and trends, or (iv) any action or non-performance resulting from the foregoing. This exclusion clause shall take effect to the fullest extent permitted by applicable laws. Professional Advice Any statement contained in the Content is made on a general basis and we have not given any consideration to nor have we made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You are advised to make your own assessment of the relevance, accuracy and adequacy of the information contained in the Content and conduct independent investigations as may be necessary or appropriate for the purpose of such assessment including the investment risks involved. You should consult an appropriate professional advisor for legal, tax, accounting, or investment advice specific to your situation, as to whether any governmental or other consents are required or if any formalities should be observed for the purposes of making such investments as are mentioned in the Content. If you are unsure about the meaning of any of the information contained in the Content, please consult your financial or other professional advisor. Third Party References References to third party publications are provided for your information only. The content of these publications are issued by third parties. As such, we are not responsible for the accuracy of information contained in those publications, nor shall we be held liable for any loss or damage arising from or related to their use.