Download

1 / 25

270 likes | 572 Vues

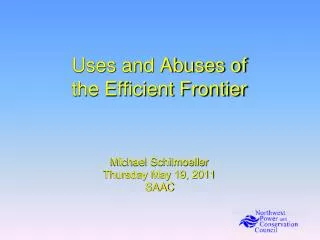

Efficient Portfolio Frontier . St. Deviation. Unique Risk. Market Risk. Number of Securities. Risk Reduction with Diversification. Two-Security Portfolio: Return. r p = W 1 r 1 + W 2 r 2 W 1 = Proportion of funds in Security 1 W 2 = Proportion of funds in Security 2

E N D

St. Deviation Unique Risk Market Risk Number of Securities Risk Reduction with Diversification

Two-Security Portfolio: Return rp = W1r1 +W2r2 W1 = Proportion of funds in Security 1 W2 = Proportion of funds in Security 2 r1 = Expected return on Security 1 r2 = Expected return on Security 2

12 = Variance of Security 1 22 = Variance of Security 2 Cov(r1r2) = Covariance of returns for Security 1 and Security 2 Two-Security Portfolio: Risk p2= w1212 + w2222 + 2W1W2 Cov(r1r2)

Covariance Cov(r1r2) = 12 1,2 = Correlation coefficient of returns 1 = Standard deviation of returns for Security 1 2 = Standard deviation of returns for Security 2

Correlation Coefficients: Possible Values Range of values for 1,2 + 1.0 > 1,2> -1.0 If = 1.0, the securities would be perfectly positively correlated If = - 1.0, the securities would be perfectly negatively correlated

Two-Security Portfolio E(rp) = W1r1 +W2r2 p2= w1212 + w2222 + 2W1W2 Cov(r1r2) p= [w1212 + w2222 + 2W1W2 Cov(r1r2)]1/2

E(r) 13% = -1 = .3 %8 = -1 = 1 St. Dev 12% 20% Two-Security Portfolios withDifferent Correlations

Portfolio Risk/Return Two Securities: Correlation Effects • Relationship depends on correlation coefficient • -1.0 << +1.0 • The smaller the correlation, the greater the risk reduction potential • If= +1.0, no risk reduction is possible

Sec 1 E(r1) = .10 = .15 = .2 12 Sec 2 E(r2) = .14 = .20 2 Minimum-Variance Combination 1 2 - Cov(r1r2) 2 = W1 2 - 2Cov(r1r2) 2 + 2 1 W2 = (1 - W1)

(.2)2 - (.2)(.15)(.2) = W1 (.15)2 + (.2)2 - 2(.2)(.15)(.2) W1 = .6733 W2 = (1 - .6733) = .3267 Minimum-Variance Combination: = .2

Minimum -Variance: Return and Risk with = .2 rp = .6733(.10) + .3267(.14) = .1131 = [(.6733)2(.15)2 + (.3267)2(.2)2 + p 1/2 2(.6733)(.3267)(.2)(.15)(.2)] 1/2 = [.0171] = .1308 p

(.2)2 - (.2)(.15)(.2) = W1 (.15)2 + (.2)2 - 2(.2)(.15)(-.3) W1 = .6087 W2 = (1 - .6087) = .3913 Minimum -Variance Combination: = -.3

Minimum -Variance: Return and Risk with = -.3 rp = .6087(.10) + .3913(.14) = .1157 = [(.6087)2(.15)2 + (.3913)2(.2)2 + p 1/2 2(.6087)(.3913)(.2)(.15)(-.3)] 1/2 = [.0102] = .1009 p

Three-Security Portfolio rp = W1r1 +W2r2 + W3r3 2p = W1212 + W22 + W3232 + 2W1W2 Cov(r1r2) + 2W1W3 Cov(r1r3) + 2W2W3 Cov(r2r3)

In General, For an n-Security Portfolio: rp = Weighted average of the n securities p2 = (Consider all pairwise covariance measures)

Extending Concepts to All Securities • The optimal combinations result in lowest level of risk for a given return • The optimal trade-off is described as the efficient frontier • These portfolios are dominant

E(r) Efficient frontier Individual assets Global minimum variance portfolio Minimum variance frontier St. Dev. The Minimum-Variance Frontierof Risky Assets

U’ U’’ U’’’ E(r) Efficient frontier of risky assets S P Less risk-averse investor Q More risk-averse investor St. Dev Portfolio Selection & Risk Aversion

Estimating the Frontier in Practice • Estimating the expected future returns • Estimating the variance-covariance matrix • Sample period: how long is too short? • Relevance:is the future the same as the past?

Extending to Include Riskless Asset • The optimal combination becomes linear • A single combination of risky and riskless assets will dominate

Portfolio Policies in Practice Objectives Constraints Policies Return Requirements Liquidity Asset Allocation Risk Tolerance Horizon Diversification Regulations Risk Positioning Taxes Tax Positioning Unique Needs Income Generation

Matrix of Objectives Type of Investor Return Requirement Risk Tolerance Individual and Personal Trusts Life Cycle Life Cycle Mutual Funds Variable Variable Pension Funds Assumed actuarial rate Depends on payouts Endowment Funds Determined by income Generally needs and asset growth to conservative maintain real value

Matrix of Objectives (cont’d) Type of Investor Return Requirement Risk Tolerance Life Insurance Spread over cost of Conservative funds and actuarial rates Nonlife Ins. Co. No minimum Conservative Banks Interest Spread Variable

Constraints on Investment Policies • Liquidity • Ease (speed) with which an asset can be sold and created into cash • Investment horizon - planned liquidation date of the investment • Regulations • Prudent man law • Tax considerations • Unique needs