Download

1 / 56

560 likes | 657 Vues

Income Statements and Budgets. chapter 14. Income Statement Disclaimer. The National Restaurant Association’s Uniform System of Accounts for Restaurants describes an industry standard format for income statements, so businesses can compare their data to other businesses

E N D

Income Statements and Budgets • chapter 14

Income Statement Disclaimer • The National Restaurant Association’s Uniform System of Accounts for Restaurants describes an industry standard format for income statements, so businesses can compare their data to other businesses • The income statement format described here is NOT the NRA approach, but a similar, simplified version that is easier to learn and that makes a transition to the NRA format easier as well. • The NRA version is described in the appendix.

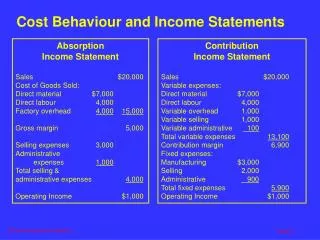

Income Statement Format • Can be written to cover any time period • Common Size Income Statement lists dollars and percents for each line item and category • Percents express each line item as a percent of sales, except for the subheadings under “Cost of Sales”

Income Statement Format (cont.) • Always start with a “Sales” category, which is subdivided into “food” and “beverage” sales • Percents for food and beverage sales show the sales mix between food and beverage • Total sales always equals 100%

Income Statement Format (cont.) • Subcategories under “cost of sales” use different percent bases (not based on total sales)

Income Statement Format (cont.) Fixed Costs includes 3 major categories:

Income Statement Graphic Formula • % column is calculated using the graphic below • For food cost and beverage cost, “sales” is the corresponding food sales or beverage sales; all other items use “total sales” for sales. Cost Sales x %

Example 14a On income statement, “marketing” is listed as $7,000. Total sales are $380,000. What percent should be written next to “marketing”? • % = Cost ÷ Sales • = $7,000 ÷ $380,000 • = 1.8%

Example 14b Income statement lists food sales as $114,600. Manager wants to run a 30.4% food cost. What should food cost be in dollars? • Food Cost = Food Sales X % • = $114,600 X 0.304 • = $34,838

Comparing Income Statements and Budgets • Income statements and budgets look similar • Same line item names and common size format • Income statements use real data from history • Budget is forward-looking plan • Both are often compared side-by-side • Two approaches to compare them: common size analysis and comparative analysis Income Statements Budgets vs.

Common Size Analysis • Calculate difference between the two percent columns on each budget/income statement line item. • Variance = income statement percent – budget percent. (Or, if comparing 2 income statements, the new statement’s percent – older statement’s percent) • Note: Since total sales are always 100%, their variance will always be zero. Look at sales dollars separately.

Variances • Management determines acceptable variance range in advance. • Management must decide what to do about unacceptable variances • Options include: • controlling costs • boosting revenue through marketing • or adjusting the budget • If figures beat expectations without sacrificing business standards, changing the budget may be appropriate

Comparative Analysis • Calculate the difference (variance) in dollars between the line items in two periods as follows: variance = newer dollars – older (or budget) dollars • Convert the dollar difference into a percent change as follows: Dollar variance = % Earlier time period (or budget) dollars

Comparative Analysis (cont.) • Great for determining trends • Identifies how well dollar figures align with the budgeted dollar figures • Does not highlight problems that occur when managers fail to adjust their expenses to reflect shifts in revenue

Why Comparative vs. Common Size Analysis? • Comparative provides dollar differences as well as percent variances • Comparative highlights differences in small value line items better • Comparative shows trends for future budgeting • Common Size better highlights changes management should have made when revenue misses its target • Best to perform both types of analysis Common Size Comparative vs.

Creating a Budget • Budget must be realistic to have any value • Goals of a budget: • Predict revenue and expenses accurately • Set aggressive targets for managers to hit • Accuracy gives managers a road map to use • Aggressive targets push everyone to be a little more efficient

Why Front-Line Workers Should Care about Profits • Greater profits lead to stable company and better job security • Large profits can lead to expansion, raises, and promotions • With profits, owner may invest in facility to improve working conditions

Historical Data • Usually comes from POS • Include: • check average • customer counts • expense patterns and trends (in $ and %) • income statements over multiple years Historical Data is the starting point for the next budget.

Internal and External Variables Internal come from outside the business. • new equipment • menu changes Internal and External Variables are used to identify changes from prior trends. • External • come from outside the business. • new competitor • closure of local business • spikes in food prices External learned from trade publications, professional associations, news reports, customers and purveyors

Setting Budget Goals • Management team sets goals for revenue growth and expense percents • Must be realistic, achievable, and based somewhat on historical data and internal/external variables • Do not have to match forecasts exactly

Example 14c Total sales on income statement were $700,000. Management wants 5% increase in sales next year. What is next year’s total sales budget? • New amt = old amt. X (1 + % change) • = $700,000 X (1 + 0.05) • = $735,000

Example 14d Management says “marketing” should be 4.9% of sales. If total sales are budgeted at $735,000, what is marketing budget? • Cost = Sales X % • = $735,000 X 0.049 • = $36,015

Example 14e This year, repairs and maintenance is $17,300. Management wants to cut this line item by 8%. What is next year’s budget for repairs and maintenance? • New Cost = Old Cost X (1 + % change) • = $17,300 X (1 + (-0.08)) • = $17,300 X 0.92 • = $15,916

Example 14f • Monthly = $4,800 + $800 + $630 = $6,230 • Annual = $6,230 X 12 months = $74,760 For next year, management knows rent will remain $4,800 per month. Property taxes are increasing to $800 per month. Property insurance will be $630 per month. If these are the only components of occupancy cost, what is the monthly and annual budget for next year’s occupancy cost line?

Planning for Profit If entering all sales and expense dollars, based on forecasts and management goals, into budget spreadsheet does not generate desired profit, management must adjust the expense lines to try to hit the profit target– unless the profit goal is unrealistic.

Planning for Profit (cont.) • Changes to initial budget must be feasible for managers to achieve, or they will never materialize • Every change must come with a plan of action describing how the change will be managed in the real-world

Dividing a Budget into Smaller Time Frames • Easier to adjust daily work habits, schedules, and purchases to align with a budget if the budget is done in a smaller time frame • Using only annual budgets, managers may not catch problems until it is too late • Business fluctuates seasonally, so managers cannot just divide annual budget by 12 or 52 to get monthly or weekly versions

Dividing a Budget into Smaller Time Frames Historical data reveals the percent of annual revenue that is brought in each month, week, or day. Historical patterns are usually consistent from year to year.

Creating a Monthly Revenue Budget • List last year’s historical revenue per month and total annual revenue • Calculate percent revenue each month represents. Monthly sales % = Annual sales Using next year’s annual sales forecast, calculate each month’s sales as: Annual Sales X % for a given month (from step 2)

Example 14g In August last year, sales were $33,300. Annual sales were $358,000. If next year’s sales budget is $380,000, what should August’s sales budget be? • $33,300 ÷ $358,000 = 0.093 or 9.3% (August %) • $380,000 X 0.093 = $35,340 (August sales)

Calculating Monthly Budget • Management may adjust monthly percents slightly based on internal or external variables • From monthly sales, calculate monthly expenses: • Keep variable costs the same % of sales • Write fixed costs based on their payment schedule; may be evenly divided by month.

Calculating Monthly Budget (cont.) • For semi-variable costs, separate the fixed and variable components. • Divide fixed components evenly over the year; keep variable components the same percent of sales. • With labor, factor in any planned pay increases • For expenses with an irregular payment schedule (e.g., repairs and maintenance), schedule the payments for the appropriate months.