Download

1 / 48

550 likes | 854 Vues

Chapter 2. $. Business Transactions and the Accounting Equation. $. Making Accounting Relevant Every business has assets, liabilities (debts), and owner’s equity. Think about a business in your community. $. $. What possible assets does this business possess?. Chapter 2. $.

E N D

Chapter 2 $ Business Transactions and the Accounting Equation $ Making Accounting Relevant Every business has assets, liabilities (debts), and owner’s equity. Think about a business in your community. $ $ What possible assets does this business possess?

Chapter 2 $ Section 1 Property and Financial Claims • What You’ll Learn • The relationship between property and financial claims. • The meaning of equity as it is used in accounting. • The parts of the accounting equation. • The definition of each part of the accounting equation. $ $ $

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Why It’s Important The accounting equation is the basis for keeping all accounting records in balance. $ • Key Terms • property • property rights • financial claims • credit • creditor • assets $ • investments • equity • owner’s equity • liabilities • accounting equation $

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Property: Ownership and Control Property is anything of value that is owned or controlled. $ $ Property Financial Right Claim Own Yes Yes Control (like rent) Yes No $

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Property: Ownership and Control (con’t.) In accounting, property and financial claims are measured in dollar amounts. $ $ Property = Financial (Cost) (Financial Investments) Bike Lock = Your Claim to the Bike $600 = $600 $

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Property: Ownership and Control (con’t.) When you buy property and agree to pay for it later, you are buying on credit. $ $ Property = Financial Claims Bike Creditor’s Owner’s Lock = Financial Claim + Financial Claim $100 = $40 + $60 $

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Financial Claims in Accounting Assets property or items of value owned by a business Owner’s Equity the owner’s claims to the assets of the business Liabilities creditor’s claims to the assets of the business $ $ $

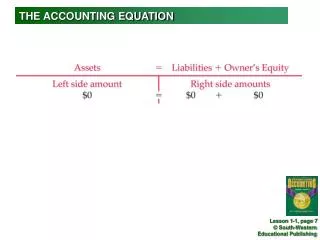

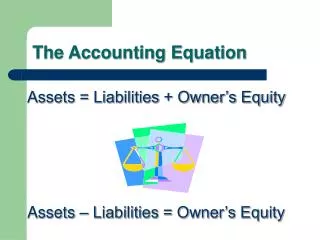

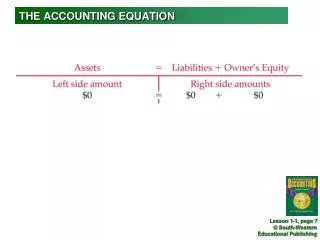

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ The Accounting Equation $ Creditor’s Owner’s Financial Claim Financial Claim Property = + $ $ Assets = Liabilities + Owner’s Equity

Section 1 Property and Financial Claims (con’t.) Chapter 2 $ Check Your Understanding $ What is meant by having a financial claim to property? $ $

Chapter 2 $ Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit $ • What You’ll Learn • How accounts are used in business transactions. • The steps used to analyze business transactions. • How investments by the owner affect the accounting equation. • How a cash payment transaction affects the accounting equation. • How a credit transaction affects the accounting equation. $ $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Why It’s Important You can analyze real-world business transactions by using the accounting equation. $ $ • Key Terms • business transactions • account • accounts receivable • accounts payable • on account $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Business Transactions • An economic event that causes a change — either an increase or a decrease — in assets, liabilities, or owner’s equity. • The increases and decreases caused by business transactions are recorded in specific accounts. • Accounts may be classified as either assets, liabilities, or owner’s equity. $ $ $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Business Transactions (con’t.) $ Assets = Liabilities + Owner’s Equity Cash in Bank Accounts Maria Sanchez, Accounts Receivable Payable Capital Computer Equipment Office Equipment Delivery Equipment $ $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Effects of Business Transactions on the Accounting Equation Analyzing business transactions: $ Business Transaction $ ANALYSISIdentify Classify + / - Balance 1. Identify the accounts affected. 2. Classify the accounts affected. 3. Determine the amount of increase or decrease for each account. 4. Make sure the accounting equation remains in balance. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner Business Transaction 1 $ Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service. $ ANALYSISIdentify 1. Cash transactions are recorded in the account Cash in Bank. Maria Sanchez is investing personal funds in the business. Her investment in the business is recorded in the account called Maria Sanchez, Capital. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 1 (con’t.) $ Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service. $ ANALYSISClassify 2. Cash in Bank is an asset account. Maria Sanchez, Capital is an owner’s equity account. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 1 (con’t.) $ Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service. $ ANALYSIS + / – 3. Cash in Bank is increased by $25,000. Maria Sanchez, Capital is increased by $25,000. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 1 (con’t.) $ Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash in Bank Maria Sanchez, Capital Trans. 1 +$25,000 = 0 + +$25,000

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner (con’t.) Business Transaction 2 $ The owner, Maria Sanchez, took two telephones valued at $200 each (total $400) from her home and transferred them to the business as Office Equipment. $ ANALYSISIdentify 1. The business received two telephones. Since a telephone is office equipment, the account Office Equipment is affected. Maria Sanchez invested a personal asset in the business, so the account Maria Sanchez, Capital is affected. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 2 (con’t.) $ The owner, Maria Sanchez, took two telephones valued at $200 each (total $400) from her home and transferred them to the business as Office Equipment. $ ANALYSISClassify 2. Office Equipment is an asset account. Maria Sanchez, Capital is an owner’s equity account. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 2 (con’t.) $ The owner, Maria Sanchez, took two telephones valued at $200 each (total $400) from her home and transferred them to the business as Office Equipment. $ ANALYSIS + / – 3. Office Equipment is increased by $400. Maria Sanchez, Capital is increased by $400. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Investments by the Owner(con’t.) Business Transaction 2 (con’t.) The owner, Maria Sanchez, took two telephones valued at $200 each (total $400) from her home and transferred them to the business as Office Equipment. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Office Maria Sanchez, in Bank Equip. Capital Prev. Bal.$25,000 0 0 $25,000 Trans. 2+400 +400 Balance $25,000 + $400 = 0 + $25,400 $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Cash Payment Transactions Business Transaction 3 $ Roadrunner issued a $3,000 check to purchase a computer system. ANALYSISIdentify 1. The Computer Equipment account is used to record transactions involving any type of computer equipment. The business paid cash for the computer system, so the account Cash in Bankis affected. (Payments made by check are treated as cash payments and are recorded in the Cash in Bank account.) $ $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Cash Payment Transactions (con’t.) Business Transaction 3 (con’t.) $ Roadrunner issued a $3,000 check to purchase a computer system. $ ANALYSISClassify 2. Computer Equipment and Cash in Bank are both asset accounts. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Cash Payment Transactions (con’t.) Business Transaction 3 (con’t.) $ Roadrunner issued a $3,000 check to purchase a computer system. $ ANALYSIS + / – 3. Computer Equipment is increased by $3,000. Cash in Bank is decreased by $3,000. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Cash Payment Transactions (con’t.) Business Transaction 3 (con’t.) Roadrunner issued a $3,000 check to purchase a computer system. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Computer Office Maria Sanchez, in Bank Equip. Equip. Capital Prev. Bal.$25,000 0 $400 0 $25,400 Trans. 3– 3,000+3,000 Balance$22,000 + $3,000 + $400 = 0 + $25,400 $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Credit Transactions Business Transaction 4 $ Roadrunner bought a used truck on account from North Shore Auto for $12,000. ANALYSISIdentify 1. Roadrunner purchased a truck to be used as a delivery vehicle, so the account, Delivery Equipment is affected. The business promised to pay for the truck at a later time. This promise to pay is a liability; therefore, the Accounts Payable is affected. $ $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Credit Transactions (con’t.) Business Transaction 4 (con’t.) $ Roadrunner bought a used truck on account from North Shore Auto for $12,000. $ ANALYSISClassify 2. Delivery Equipment is an asset account. Accounts Payable is a liability account. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Credit Transactions (con’t.) Business Transaction 4 (con’t.) $ Roadrunner bought a used truck on account from North Shore Auto for $12,000. $ ANALYSIS + / – 3. Delivery Equipment is increased by $12,000. Accounts Payable is also increased by $12,000. $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Credit Transactions (con’t.) Business Transaction 4 (con’t.) Roadrunner bought a used truck on account from North Shore Auto for $12,000. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Computer Office Delivery Accounts Maria Sanchez, in Bank Equip. Equip. Equip. Payable Capital Prev. Bal.$25,000 +3,000 $400 0 0 $25,400 Trans. 4– +12,000 +12,000 Balance $22,000 + $3,000 + $400 +$12,000 = $12,000 + $25,400 $

Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit (con’t.) Chapter 2 $ Check Your Understanding $ When a business transaction occurs, what is the role of the accountant or accounting clerk? $ $

Chapter 2 Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner $ $ • What You’ll Learn • How revenue transactions affect the accounting equation. • How expense transactions affect the accounting equation. • How withdrawals by the owner affect the accounting equation. $ $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Why It’s Important The experience you gain by analyzing revenue, expense, and withdrawal transactions will help you analyze transactions in real-world situations. $ $ • Key Terms • revenue • expense • withdrawal $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Revenue and Expense Transactions $ • Income earned from the sale of goods or services is revenue. • An expense is the price paid for goods or services used to operate a business. $ $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Revenue Transaction Business Transaction 8 $ Roadrunner received a check for $1,200 from a customer, Sims Corporation, for delivery services. ANALYSISIdentify 1. Roadrunner received cash, so Cash in Bank is affected. The payment received is revenue. Revenue increases owner’s equity, so Maria Sanchez, Capital is also affected. $ $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Revenue Transaction (con’t.) Business Transaction 8 (con’t.) $ Roadrunner received a check for $1,200 from a customer, Sims Corporation, for delivery services. $ ANALYSISClassify 2. Cash in Bank is an asset account. Maria Sanchez, Capital is an owner’s equity account. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Revenue Transaction (con’t.) Business Transaction 8 (con’t.) $ Roadrunner received a check for $1,200 from a customer, Sims Corporation, for delivery services. $ ANALYSIS + / – 3. Cash in Bank is increased by $1,200. Maria Sanchez, Capital is also increased by $1,200. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Revenue Transaction (con’t.) Business Transaction 8 (con’t.) Roadrunner received a check for $1,200 from a customer, Sims Corporation, for delivery services. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Accounts Computer Office Delivery Accounts Maria Sanchez, in Bank Receivable Equip. Equip. Equip. Payable Capital Prev. Bal. $21,850 $0 $3,000 $200 $12,000 $11,650 $25,400 Trans. 8+1,200 +1,200 Balance$23,050 + $0 + $3,000 + $200 + $12,000 = $11,650 + $26,600 $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Expense Transaction Business Transaction 9 $ Roadrunner wrote a check for $700 to pay the rent for the month. $ ANALYSISIdentify 1. Roadrunner pays rent for use of building space. Rent is an expense. Expenses decrease owner’s equity, so the account Maria Sanchez, Capital is affected. The business is paying cash for the use of the building, so Cash in Bankis affected. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Expense Transaction (con’t.) Business Transaction 9 (con’t.) $ Roadrunner wrote a check for $700 to pay the rent for the month. $ ANALYSISClassify 2. Maria Sanchez, Capital is an owner’s equity account. Cash in Bank is an asset account. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Expense Transaction (con’t.) Business Transaction 9 (con’t.) $ Roadrunner wrote a check for $700 to pay the rent for the month. $ ANALYSIS + / – 3. Maria Sanchez, Capital is decreased by $700. Cash in Bank is decreased by $700. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Expense Transaction (con’t.) Business Transaction 9 (con’t.) Roadrunner wrote a check for $700 to pay the rent for the month. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Accounts Computer Office Delivery Accounts Maria Sanchez, in Bank Receivable Equip. Equip. Equip. Payable Capital Prev. Bal. $23,050 $0 $3,000 $200 $12,000 $11,650 $26,600 Trans. 8– 700 – 700 Balance$22,350 + $0 + $3,000 + $200 + $12,000 = $11,650 + $25,900 $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Withdrawals by the Owner If a business earns revenue, the owner will take cash or other assets from the business for personal use. This transaction is called a withdrawal. $ $ $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Withdrawals by the Owner (con’t.) Business Transaction 10 $ Maria Sanchez withdrew $500 from the business for her personal use. $ ANALYSISIdentify 1. A withdrawal decreases the owner’s claim to the assets of the business, so Maria Sanchez, Capital is affected. Cash is paid out, so the Cash in Bank account is affected. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Withdrawals by the Owner (con’t.) Business Transaction 10 (con’t.) $ Maria Sanchez withdrew $500 from the business for her personal use. $ ANALYSISClassify 2. Maria Sanchez, Capital is an owner’s equity account. Cash in Bank is an asset account. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Withdrawals by the Owner (con’t.) Business Transaction 10 (con’t.) $ Maria Sanchez withdrew $500 from the business for her personal use. $ ANALYSIS + / – 3. Maria Sanchez, Capital is decreased by $500. Cash in Bank is decreased by $500. $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Withdrawals by the Owner (con’t.) Business Transaction 10 (con’t.) Maria Sanchez withdrew $500 from the business for her personal use. $ ANALYSISBalance 4. The accounting equation remains in balance. $ Assets = Liabilities + Owner’s Equity Cash Accounts Computer Office Delivery Accounts Maria Sanchez, in Bank Receivable Equip. Equip. Equip. Payable Capital Prev. Bal. $22,350 $0 $3,000 $200 $12,000 $11,650 $25,900 Trans. 8– 500 – 500 Balance$21,850 + $0 + $3,000 + $200 + $12,000 = $11,650 + $25,400 $

Section 3 Transactions That Affect Revenue, Expense, and Withdrawals by the Owner (con’t.) Chapter 2 $ Check Your Understanding $ 1.What effect does revenue have on a business? $ 2.What effect do withdrawals have on a business? $