Download

1 / 5

60 likes | 192 Vues

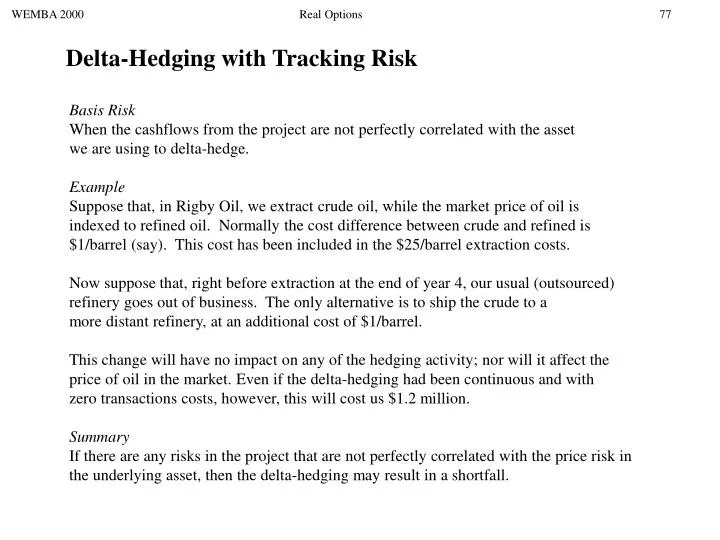

WEMBA 2000 Real Options 77. Delta-Hedging with Tracking Risk. Basis Risk When the cashflows from the project are not perfectly correlated with the asset we are using to delta-hedge. Example Suppose that, in Rigby Oil, we extract crude oil, while the market price of oil is

E N D

WEMBA 2000 Real Options 77 Delta-Hedging with Tracking Risk Basis Risk When the cashflows from the project are not perfectly correlated with the asset we are using to delta-hedge. Example Suppose that, in Rigby Oil, we extract crude oil, while the market price of oil is indexed to refined oil. Normally the cost difference between crude and refined is $1/barrel (say). This cost has been included in the $25/barrel extraction costs. Now suppose that, right before extraction at the end of year 4, our usual (outsourced) refinery goes out of business. The only alternative is to ship the crude to a more distant refinery, at an additional cost of $1/barrel. This change will have no impact on any of the hedging activity; nor will it affect the price of oil in the market. Even if the delta-hedging had been continuous and with zero transactions costs, however, this will cost us $1.2 million. Summary If there are any risks in the project that are not perfectly correlated with the price risk in the underlying asset, then the delta-hedging may result in a shortfall.

WEMBA 2000 Real Options 78 Sell delta * 1.2 barrels = $26.88 less trans. 0.5% = -0.134 Reserve $14.8 (Call option value) Date Price Delta T=0 28 0.8 T=1 41.77 0.91 T=2 62.32 0.98 T=3 92.96 1.00 T=4 138.68 1.00 Invest remainder: $11.95 at 6.3% Re-hedge: sell further 0.13 barrels for $5.51 less trans. 0.5% = -0.0276 $12.70 at year end = $18.19 Invest at 6.3% + Re-hedge: sell further 0.084 barrels for $5.23 less trans. 0.5% = -0.026 = $24.54 Invest at 6.3% $19.33 at year end + = $28.30 Invest at 6.3% Re-hedge: sell further 0.024 barrels for $2.23 less trans. 0.5% = -0.011 $26.08 at year end + Buy back 1.2 barrels for - $166.42 less trans. 0.5% = -0.83 $30.08 at year end = - $137.17 + Exercise Option: (138.68 - 25)*1.2 = $136.41

WEMBA 2000 Real Options 79 Delta-Hedging with Transactions Costs Rigby Oil Without Transactions Costs With Transactions Costs $320,000 excess from delta-hedging $762,000 shortfall from delta-hedging How do we minimize the transactions costs? Hedge "within a band"! With transactions costs and hedging within a band $9,560,000 excess!

WEMBA 2000 Real Options 80 Sell delta * 1.2 barrels = $26.88 less trans 0.5% = -0.134 Reserve $14.8 (Call option value) "Real" Hedge Date Price Delta Position T=0 28 0.8 0.8 T=1 41.77 0.91 0.81 T=2 62.32 0.98 0.88 T=3 92.96 1.00 0.90 T=4 138.68 1.00 0.90 Invest remainder: $11.95 at 6.3% Re-hedge: sell further 0.01 * 1.2 barrels for $0.5 less trans. 0.5% = -0.003 $12.7 at year end = $13.20 Invest at 6.3% + Re-hedge: sell further 0.07 * 1.2 barrels for $5.23 less trans. 0.5% = -0.026 = $19.23 Invest at 6.3% $14.02 at year end + = $22.29 Invest at 6.3% Re-hedge: sell further 0.02 * 1.2 barrels for $1.86 less trans. 0.5% = -0.009 $20.44 at year end + $23.70 at year end Buy back 0.9*1.2 = -$149.8 less trans. 0.5% = -0.749 = - $126.85 + Exercise Option: (138.68 - 25)*1.2 = $136.41

WEMBA 2000 Real Options 81 "Within-Band" Delta-Hedging with Transactions Costs Alternative Price movement scenarios: Excess/Shortfall no trans.costs trans. costs costs & band $320,000 -$758,000 $9,660,000 - $1,720,000 -$2,060,000 -$4,503,000 Scenario 1: S = 28 : 41.77 : 62.32 : 92.96 : 138.68 = 0.8 : 0.91 : 0.98 : 1.00 : 1.00 'band-hedge' = 0.8 : 0.81 : 0.88 : 0.90 : 0.90 Scenario 2: S = 28 : 41.77 : 28.00 : 18.77 : 28.00 = 0.8 : 0.91 : 0.76 : 0.36 : 1.00 'band-hedge' = 0.8 : 0.81 : 0.81 : 0.46 : 0.46 OOPS!! So, should we forget "hedging within the band"? Or is there something we could do differently?