Download

1 / 24

240 likes | 471 Vues

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD. Algunas cosas son obvias y es por ello han que hay que tenerlas siempre presentes

E N D

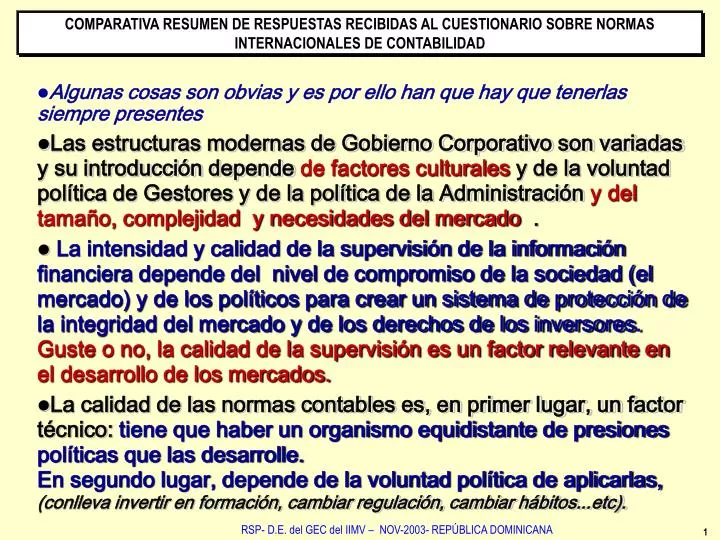

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD • Algunas cosas son obvias y es por ello han que hay que tenerlas siempre presentes • Las estructuras modernas de Gobierno Corporativo son variadas y su introducción depende de factores culturales y de la voluntad política de Gestores y de la política de la Administración y del tamaño, complejidad y necesidades del mercado . • La intensidad y calidad de la supervisión de la información financiera depende del nivel de compromiso de la sociedad (el mercado) y de los políticos para crear un sistema de protección de la integridad del mercado y de los derechos de los inversores.Guste o no, la calidad de la supervisión es un factor relevante en el desarrollo de los mercados. • La calidad de las normas contables es, en primer lugar, un factor técnico: tiene que haber un organismo equidistante de presiones políticas que las desarrolle. En segundo lugar, depende de la voluntad política de aplicarlas,(conlleva invertir en formación, cambiar regulación, cambiar hábitos...etc). RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 1

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD • ¿Cuantas barreras a la entrada y salida de capitales en nuestro mercado queremos tener?. • Guste o no, la contabilidad es una barrera más. • Cuanto menos comprensibles sean para otros los estados financieros de una determinada jurisdicción mayor la desincentivación a los flujos de capitales hacia esa jurisdicción. • La calidad de la contabilidad afecta a la calidad de la información financiera y de ésta dependen, junto a otros factores, la integridad del mercado y la confianza de los inversores e intermediarios en el mismo; por ende ello afecta al Coste del Capital Externo. La autarquía es irreal en un mundo global. RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 2

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 3

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD 134 272 Equivalencias NCA-NCE 177 Equivalencias NIC-NCA Equivalencias NIC-NCE NIC NCE NCA RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 4

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 5

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD Argentina Bolivia Comunes Chile España Perú Brasil Mapa Equivalencias de cada jurisdicción con NICs Mapa Equivalencias Inter-jurisdicciones RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 6

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD BASES DE DATOS BASES DE DATOS Argentina Mapa Equivalencias de cada jurisdicción con NICs diferencias Bolivia Brasil Mapa Equivalencias Inter-jurisdicciones Chile España Perú RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 7

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 8

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 9

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 10

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 11

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 12

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 13

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 14

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 15

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 16

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 17

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 18

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 19

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 20

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 21

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 22

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 23

COMPARATIVA RESUMEN DE RESPUESTAS RECIBIDAS AL CUESTIONARIO SOBRE NORMAS INTERNACIONALES DE CONTABILIDAD Equivalencias NCA-NCE Equivalencias NIC-NCA Equivalencias NIC-NCE NIC NCE NCA RSP- D.E. del GEC del IIMV – NOV-2003- REPÚBLICA DOMINICANA 24