Download

1 / 10

110 likes | 349 Vues

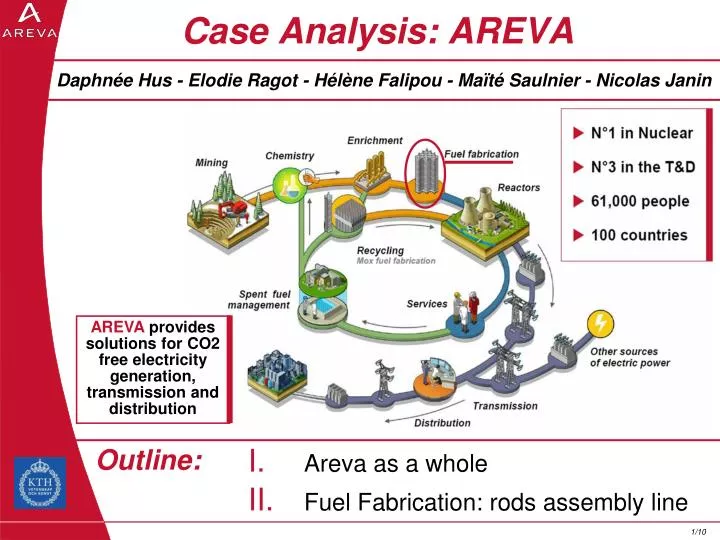

Case Analysis: AREVA. Daphnée Hus - Elodie Ragot - Hélène Falipou - Maïté Saulnier - Nicolas Janin. AREVA provides solutions for CO2 free electricity generation, transmission and distribution. Outline:. Areva as a whole Fuel Fabrication: rods assembly line.

E N D

Case Analysis: AREVA Daphnée Hus - Elodie Ragot - Hélène Falipou - Maïté Saulnier - Nicolas Janin AREVA provides solutions for CO2 free electricity generation, transmission and distribution Outline: • Areva as a whole • Fuel Fabrication: rods assembly line

Income Statement, 1st Semester 2007 I. 1) Overheads • Gross Margin: 1084 M€; • Net Financial Income: 118 M€ Big difference = a lot of Overheads

Simplified balance Sheet, 1st Semester 2007 I. 2) VARIATION: 60 % working capital = net balance of operating uses and sources of funds If WCR>0: uses of funds exceed sources of funds, if WCR<0: sources of funds higher than uses WCR<0 corresponding to a netuse of customer advances and prepayments

Caps Tube Fuel Fuel rod Fuel assembly Research and Development Marketing and sales Design Supply PRODUCTION Distribution Customer service Make to order Internal suppliers Pull production Developing Core process Adaptation to customers’ needs Market decisions: Product-life cycle: • Price setter • Long-run pricing • High quality/High price • Maturity Fuel assembly factory Cost object: II. 1) Skeleton Fuel rods Value Chain: Cost object

Costs II. 2) • Example of product costs: • Direct materials: raw materials (skeleton, caps, tubes, nuclear fuel…) • Direct labour: people who work more than 75% in production (workers of the production process line) • Manufacturing overheads: • Indirect material: paper, gloves to protect workers… • Indirect labour: employees from maintenance of machinery… • Indirect manufacturing expenses: lighting, heating and insurance… • Example of period costs: marketing and sales, accounting… • Variability of costs: • Fixed costs: salary, maintenance… • Variable costs: row materials…

ABC system II. 3) • Costing system • Job-costing : Each fuel assembly has its own characteristics and is unique, • ABC : - More details and focuses on activities and cost drivers - Talks the language of the organization

EU, Normal, Abnormal losses 1 Fuel assembly = 200 rods + 1 skeleton • Equivalent Unit ? II. 4) We can count the number of components integrated at each stage of the process we can determine the cost of a product not yet finished without using the concept of EU • Abnormal losses • Uranium loss • Normal losses • Bad soldering (due to worker´s mistakes), • Tube and cap losses (0,5% of tolerated losses due to suppliers)

Management Control II. 5) Budget limitation • Result Control • Graph results • Information display, where everybody can see the results, the objectives and so on… • Responsibility centre • Profit centre • The fuel assemblies are sold to another branch of AREVA company • Cybernetic control system • Weekly meeting • Feedback from the workers • Continuous improvement policy AN INFORMATION DISPLAY

Budgeting process AREVA NC AREVA NP AREVA T&D REACTORS SECTOR FUEL SECTOR NUCLEAR SERVICES SECTOR FUEL MANUFACTURING BU ZIRCONIUM MANUFACTURING BU DESIGN & SALES BU FBFC Factory A Factory C Factory D Factory B II. 6) EQUIPMENT SECTOR Bottom-up system • Activity based budgeting: • Estimation of the customers’orders for the next year. Estimation of resources needed

Relevant Costs II. 7) • Should a second assembly line be created? • In the fuel assembly factory, old machines are not allowed to be resold after use (remaining radiation) No disposal value