Download

1 / 26

300 likes | 764 Vues

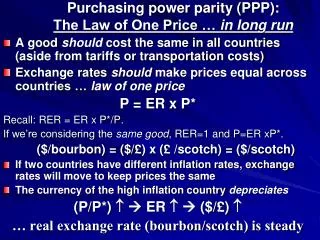

VI. Purchasing Power Parity. Read Chapter 4, pp. 102‑111 1. The Law of One Price (LOP) LOP Conditions for LOP to hold 2. Purchasing Power Parity (PPP) Absolute PPP Relative PPP Empirical evidence Real Interest Rate Parity and international Fisher effect 3. Real Exchange Rate

E N D

VI. Purchasing Power Parity Read Chapter 4, pp. 102‑111 1. The Law of One Price (LOP) LOP Conditions for LOP to hold 2. Purchasing Power Parity (PPP) Absolute PPP Relative PPP Empirical evidence Real Interest Rate Parity and international Fisher effect 3. Real Exchange Rate Definition Effective exchange rates Exchange rate pass-through

Overview: International Parity Conditions 0 • Some fundamental questions that managers of MNEs, international portfolio investors, importers, exporters and government officials must deal with every day are: • What are the determinants of exchange rates? • Are changes in exchange rates predictable? • The economic theories that link exchange rates, price levels, and interest rates together are called international parity conditions. • These international parity conditions form the core of the financial theory that is unique to international finance. • We look at the relation between exchange and price levels.

1. The Law of One Price (LOP) 0 1.1. The Law of One Price (LOP) • LOP: Commodity arbitrage should equalize the prices of a same good in two countries, when measured in the same currency (except for transportation costs). • So, for spot rate St measured as ($/£), Pt = St P£t Pt: $-price of an iPod in Canada P£t: £-price of an iPod in U.K.

1.1. The Law of One Price (LOP) 0 • Example: Pt = $100, P£t = £50. Q1: What is spot rate at which the LOP holds? St(LOP) = $100/£50 = $2/£. Q2: What happens if St moves to $1/£? St P£t = ($1/£)(£50) = $50, while Pt=$100. Arbitragers buy in U.K. and sell in Canada. Then St Pt£ goes up (e.g. $75) and Pt goes down (e.g. $75): At this point, there is no incentives for further arbitrage. ║

1.2 Conditions for LOP 0 • Homogeneity of the good • No barriers to trade (tariffs, import duties and quotas.) • No transportation costs.

2. Purchasing power parity (PPP) 0 2.1 Absolute purchasing power parity • Arbitrage in price levels leads to absolute PPP. The price level refers to an weighted average price of all goods and services in the economy. Pt: price level in Canada measured in $ P£t: price level in U.K. measured in £. • Then arbitrage ensures, Pt = St P£t. 2.2 Relative purchasing power parity Interpret Pt as price index.

2.2 Relative purchasing power parity 0 Q: SPPP? (200/100) = (150/100) [St+1/3.00]. St+1= $4.00/£.

2.2 Relative purchasing power parity 0 • Recall that inflation rates are defined as Rewrite the relative version of the PPP, using π and π*:

P PPP line Exhibit 4.2 Purchasing Power Parity (PPP) 0 Percent change in the spot exchange rate for foreign currency 4 3 2 1 -6 -5 -4 -3 -2 -1 1 2 3 4 5 6 -1 Percent difference in expected rates of inflation (foreign relative to home country) -2 -3 -4

2.2 Relative purchasing power parity • Relative PPP describes the linkage among domestic and foreign inflation, and exchange rates. • The percentage change in the exchange rate is approximately equal to the difference between domestic and foreign inflation. • In other words, the depreciation or appreciation of the exchange rate offsets the difference in inflation rates. • Justification for the PPP: Imagine a high inflation in Canada but no change in spot exchange rate. Then imports will become more competitive, and exports less competitive, leading to a deficit on current account, and exerting downward pressure on dollar.

2.2 Relative purchasing power parity • Example: Suppose π$(Canada)=5% p.a., and π£(U.K.)=2% p.a. Then the £ is expected to appreciate roughly by 3% p.a. This relation holds fairly well for high inflation countries. • Example: In early 1980s, Israel began running high inflation. First 2 quarter of 1984: πIsrael = 197.2% p.a. π$ = 4.2% p.a. (St+1 - St)/St = - 192.8% p.a. ║

2.3 Empirical evidence 2.3 Empirical evidence Q: Is St = Pt/P*t ? A: No. • Reasons: • Different basket of goods for price indexes. • Non-traded goods. • Barriers to trade • Transportation costs • Long adjustment time • PPP is still useful as • a long-run benchmark exchange rate • a basis to make a more meaningful international comparisons of economic data.

2.3 Empirical evidence • GDP in 2002 measured in market and PPP exchange rate (column 3 is based on market, and column 5 based on PPP exchange rate.)

2.4 Real interest parity and international Fisher effect [Beginning of optional material] Q: How are interest rates in foreign money markets related to dollar interest rates? We will first look at the "Uncovered Interest Parity" (UIP). Uncovered Interest Parity Recall covered interest parity: (1+i$)=(1+i£)(Ft/St) Replace Ft with EtSt+1 to get the uncovered interest parity: (1+i$) = (1+i£)(EtSt+1/St)

2.4 Real interest parity and international Fisher effect Example: An investor with $1 million . i£ : 9.0% p.a. i$ : 4.5% p.a. Spot: $1.6689/£ Expected spot rate: $1.6000/£ (1) Investor can invest $1 m at dollar interest rate and earn, (1 + i$)($1 m) = (1.045)($1 m) = $1.045m (2) Or, convert $1m into £ at the spot market, receiving, $1 m*/($1.6689/£) = £0.5992 m. (3) Then invest these proceeds in a £ deposit to receive: (1 + i£) * £0.5992 m = 1.09 * £0.5992 = £0.6531 m His expected return in dollars is: (1/St)*(1+i£)*Et St+1 = £0.6531m*($l.60/£) = $1.045 m Note that the expected returns are the same regardless of the currency invested.

2.4 Real interest parity and international Fisher effect • The relation equalizing expected returns is called the Uncovered Interest Parity (UIP): (1 + i$) = (1 + i£) (EtSt+1/St) • UIP: The return in $ deposits is the same as the expected return on £ deposits (e.g. i£+ expected capital loss on holding £). • Investors are willing to hold dollar bonds with yield lower than £ bonds, because dollars are expected to appreciate. • The UIP says that approximate link between interest rates (absent capital controls) is given by i$ - i£ E(e), where e (EtSt+1 –St)/St • This is also known as the international Fisher effect.

2.4 Real interest parity and international Fisher effect • Conditions Underlying Uncovered Interest Parity: a. No Capital Controls b. No Default Risk c. No Political Risk • These are also the conditions underlying Covered Interest Parity (CIP). However, for UIP, we also must add: d. No Risk Aversion.

Implication of PPP and UIP combined: Combining PPP and UIP • Recall UIP: (1 + i$) = (1 + i£)(EtSt+1/St) or i$ - i£ E(e) • Relative PPP: or π$ - π£ E(e), where e Et(St+1-St)/St Now combine UIP and PPP: i$ - i£ π$ - π£, or i$ - π$ i£- π£, But by Fisher relation, the last equation is equal to Et(r$) Et(r£), where r denotes real interest rate. It says that the expected real interest rate is the same across countries. [End of optional material]

3. Real exchange rate • How can we measure the relative competitiveness of a country's goods? • Example: Competitiveness in Canada's timber Relative competitiveness of Canada's timber depends on a) the change in price level in two countries and b) the change in exchange rates The price of Canadian timber: $2 per unit in Canada. at $2/£: selling price in U.K. is £1. at $1/£: selling price in U.K. is £1/2.

3.1 Definition: real exchange rate • The real exchange rate for $ [the currency in numerator], q, is defined as Assume Pt = P£,tSt, P$,t+1= price of a hamburger in Canada. Pt+1=$4, St+1 = $2/£, P£,t+1 = £2.50: With $Pt+1: you can buy 1 hamburger in Canada, but you can buy q = 0.8 hamburgers in U.K.

3.1 Definition: real exchange rate • If q < 1 then it means that • the inflation at home has been less than inflation abroad, after adjusting for the change in the exchange rates. • there has been an improvement in export competitiveness • Alternative interpretation • Suppose the annual inflation rate is 5% in Canada, and 3% in UK. PPP relation predicts that $ will depreciate about 2% against £. • If $ indeed depreciates 2%, the PPP holds, and the real exchange rate, q, is equal to one.

3.1 Definition: real exchange rate • If U$ indeed depreciates 6%, the $ depreciates by more than the inflation differential, and the real exchange rate, q, is equal to 0.96, strengthening the Canadian competitiveness in export market. • Real exchange rate, q, measures the extent to which the actual exchange rates deviate from PPP. Whether PPP holds or not has an important implications for international trade. • Real exchange rate is an useful tool in predicting upward or downward pressure on a country balance of payments and exchange rate.

Example: Swiss firm selling product in Canada: Q. Has Canada gained or lost competitiveness in this example? Relative Price in year t: P/(P*t St) = $120/$100 = 1.2 Case 1: no change in $ price: Pt+1/( P*t+1 St+1) = $120/$80 = 1.5. q=1.25 in year t+1. In this case, the Canadian firm lost competitiveness. Case 2: decrease in $ price Pt+1/( P*t+1 St+1) = $96/$80 = 1.2. q=1 in year t+1

Exhibit 4.3 IMF’s Real Effective Exchange Rate Indexes for the United States & Japan (1995 = 100) 0 180 160 United States Japan 140 120 100 80 60 40 20 0 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 Source: International Financial Statistics, International Monetary Fund, monthly, 1995=100.

3.2 Effective exchange rates • What happens to the competitiveness of Canada in international trade if dollar appreciates with respect to some trading partner's currencies, but depreciates with respect to others? • We look at the trade-volume-weighted average of real (nominal) exchange rates, called the real (nominal) effective exchange rates. • An increase in the real effective exchange rates signifies a loss in average competitiveness in international trade.

Exchange rate pass-through • Pass-through is the measure of response of imported and exported product prices to exchange rate changes. Suppose a BMW cost $70,000 in Canada and €70,000 in Germany, and spot rate of $1.00/€. • Assume the euro appreciates 20% to $1.20/€. If the price of the BMW in Canada rises only by 7.14% (rather than by 20%) to $75,000, then the degree of pass-through is partial: • degree of pass-through = 7.14%/20% = 35.7%. • The remaining 64.3% of the exchange rate change has been absorbed by the BMW.