Download

1 / 52

560 likes | 1.25k Vues

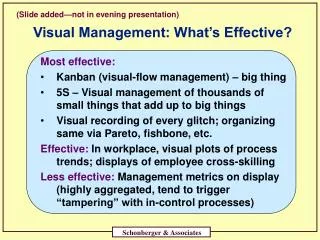

(Slide added—not in evening presentation). Visual Management: What’s Effective?. Most effective: Kanban (visual-flow management) – big thing 5S – Visual management of thousands of small things that add up to big things

E N D

(Slide added—not in evening presentation) Visual Management: What’s Effective? Most effective: • Kanban (visual-flow management) – big thing • 5S – Visual management of thousands of small things that add up to big things • Visual recording of every glitch; organizing same via Pareto, fishbone, etc. Effective: In workplace, visual plots of process trends; displays of employee cross-skilling Less effective: Management metrics on display (highly aggregated, tend to trigger “tampering” with in-control processes) Schonberger & Associates

Inventory Turnover – Paccar Up 2.1% per year for 38 years Schonberger & Associates

Days of Inventory Terex Bought Genie 10/02 Schonberger & Associates

The Confused State of Lean:Comparing Regions, Industries, CompaniesPDM, Puget Sound APICSWednesday, Dec. 12, 2007 Presenter Richard J. Schonberger 177 107th Ave., N.E., #2101 Bellevue, WA 98004 USA – Tel/Fax +425-467-1143 Schonberger & Associates

This presentation includes research and topical materials incorporated into a forthcoming Richard Schonberger book (John Wiley & Sons): Best Practices in Lean Six Sigma Process Improvement: A Deeper Look . . . with Telling Evidence from the Leanness Studies Schonberger & Associates

Topics and Tendencies • Birthplace of lean has grown fat • U.S., hotbed of lean sliding; Europe doing better • Lean bureaucratized: Fat on administration • Long-term lean: Good in A-D OEM’s, not suppliers; good in automotive suppliers, not OEM customers • Long-term lean: Cash & customer allegiance at compound interest • Lean can do worthy service even if firm going bankrupt • Several ways to get lean, not just the “lean core” • Internal lean getting the attention; external lean promises much more • Inability to keep lean going, hold lean gains. Why? Schonberger & Associates

Sample Recent Sectors Score Size Trend 1 Nordic countries .79 66 2 United Kingdom .67 80 3 Southern Europe .66 72 4 Brazil/Canada/Mexico/Israel .66 92 5 United States .59 566 6 Asiana/South Africa .58 106 Global Average .58 1,269 7 Germany/Austria .55 62 8 Benelux/Ireland .49 34 9 Japan .37 191 Sustainable Lean – Best to Worst, by Region# #Positive 10-to-50 year trend, 2 points; same but lapse last 5-7 years, 1 point; negative 10-or-more-year trend, minus ½; 5-or-more-year reversal of long negative trend, plus ½ *Includes companies acquired/merged/dissolved/privatized in last 5 years As of 9/18/07

The “Leanness Studies”: 1260+ global companies rated on long-term (at least 10 years) inventory turnover • Points & Grades: • 2 points (10 or more years up) = A • 1 point (Same but flat or down past 5-7 years) = B • Zero points (No pattern, 10 or more years) = C • 1/2 point (Down 10 or more years) = D or F • + 1/2 point (Good up recovery, 5 or more years = B+, • C+, D+, F+ Schonberger & Associates

Lean/Six Sigma: Bureaucratized Elevated to management programs, lots of . . . • Planning • Organization (e.g., Widget University, Deere Production System) • Projects run by professional staff • Name-dropping, jargon, puffery, foreign terms • Management (high-level) goals & metrics • Numerical benchmarks • Follow the leader the fads • All lead to high cost administration (SG&A) Schonberger & Associates

Lean/Six Sigma: Bureaucratized (continued) Less . . . • Work-force involvement & process ownership • Work-force knowledge & commitment • Continuous process data collection • Quick, low-level, low-cost implementations • Innovative approaches • Global best-practice benchmarking(beyond your industry, country) • External (supply/customer pipelines) activity • Results? Schonberger & Associates

Long-term Lean: Compound Effects Schonberger & Associates

Inventory Turnover Up 2.0% per year for 32 years Up 2.7% per year for 26 years B A A Schonberger & Associates

“Lean” and Close Surrogate, Inventory • Lean’s main benefits: • Reduce response time—in all things • Find problems before they fester, before trail of causes grows cold • Halt dependence on age-deteriorating item forecasts • Inventory (catch basin for multitude of ills) Each inventory unit . . . • Lengthens discovery time, fouls causal trail (lean/quick beats lot traceback) • Adds lead time (& carrying costs), loses touch with customer & real demand Schonberger & Associates

Improving the Inventory Trends • Inventory is an echo • Inventory reduction as managed goal fails: • Is easily manipulated • Must be seen as result of process improvements in every corner of the greater enterprise Schonberger & Associates

Besides Dana . . . other major vehicular suppliers in or emergent from bankruptcy: Collins & Aikman, Delphi, Dura Automotive, Eagle-Picher, Federal Mogul, Modine, Tower Automotive Collins & Aikman, Eagle-Picher, Federal Mogul, Modine much better off because of many-year compounded lean benefits (insufficient data for Delphi, Dura, Tower) Schonberger & Associates

Aerospace-Defense OEM’s Schonberger & Associates

Inventory Turnover Turns C+ Up 5.7% per year 14 years C A Schonberger & Associates

Inventory Turnover Game-Changer Modular deliveries from modular, 1st tier suppliers. Unloads millions of parts, reshuffles core competencies for mutual gain C C C Schonberger & Associates

Aerospace-Defense Suppliers Schonberger & Associates

Inventory Turnover Turns D+ C D Schonberger & Associates

Turns Inventory Turnover C D C Schonberger & Associates

Car OEM’s Schonberger & Associates

Inventory Turnover Down 2.7% per year, 16 years Chrysler acquired by Daimler in ’98, sold in ‘07 D Down 3.4% per year, 18 years D C Schonberger & Associates

Inventory Turnover C C C *Overstated – Based on sales, not cost of sales Schonberger & Associates

Inventory Turnover Down 4.0% per year, 13 years D C A Up 2.1% per year, 27 years Schonberger & Associates

Car Assemblers (25 in Leanness Database) Grades: 4 A’s 2 B’s 12 C’s 5 D’s 2 F’s Vehicular Components Producers (91 in Leanness Database*) Grades: 29 A’s 5 B’s 39 C’s 13 D’s 5 F’s *52 in Mergent list of 1000 largest global corporations Schonberger & Associates

Inventory Turnover Up 2.7% per year for 27 years A A Up 3.0% per year for 24 years A Up 3.1% per year for 26 years *Overstated: Based on sales, not cost of sales Schonberger & Associates

Inventory Turnover B C A Up 1.6% per year for 34 years Schonberger & Associates

Inventory Turnover Up 2.1% per year for 30 years B Up 2.7% per year for 26 years A A Schonberger & Associates

54 Motor-Vehicle Companies Rated on Long-Term Leanness Harley-Davidson Paccar-Kenworth Honda Tennant Magna Int’l. Thor Industries General Motors Hindustan Motors JLG Industries Ford Motor Hitachi Zosen Terex Tata Motors Kawasaki Heavy Kubota Iveco Nissan Fiat Renault Porsche Peugeot-Citroen Alvis Isuzu DaimlerChrysler AGCO Volvo Claas KgaA Nacco Industries Mitsubishi Motors Navistar Yamaha Motors Scania Winnebago Trinity Industries Toro Millat Tractors Polaris Komatsu Caterpillar Deere Audi BMW Manitowoc Fleetwood Enterpr. Suzuki Motors Nissan Diesel Daihatsu Motors* Fuji Heavy-Subaru Hino Motors* Volkswagen Toyota Motors Oshkosh Truck Champion Enterpr. Toyota Industries* Schonberger & Associates As of 5-3-07 *Toyota subsidiaries

Autos, Crucible of Lean – Best to Worst Trends 1 Harley Up 3.9%, 20 years 3 Honda Up 2.1%, 27 years 10 Ford Up 1.9%, 32 years (down sharply last 4 yrs.) 13 Tata Up 5.5%, 13 years (slump ’98-’03) 17 Nissan Up 2.8%, 11 years (after 20 years down) 23 Isuzu Flat erratically 28 years (up last few years) 26 Volvo Flat 12 years (after 10 bad yrs.; better last 6) 32 Scania Flat 11 years (after 6 good years) 36 Millat Tr. Flat very erratically, 17 years 40 Deere Down 2.8%, 13 years (up last few years) 42 BMW Down 3.4%, 18 years (less decline last 14) 51 VW Down 3.8%, 10 years (after good 16 years) 52 Toyota Down 4.0%, 13 years (after 6 flat years) Schonberger & Associates As of 5-3-07

American Greetings (greeting cards, etc.) Up 3.2% per yr. for 20 yrs. Andrew Corp. (satellite telecom equipment) Up 2.6%, 24 yrs. Applera (life-science instruments, consumables) Up 4.0%, 18 yrs. CCL Industries, Canada (aerosol containers, labels) Up 2.4%, 20 yrs. Cleveland: Brush Engineered Products (2.9, 20);Eaton (2.1, 30); Nordson (3.8, 17); Parker Hannifin (3.4, 17) Gunnebo, Sweden (cash/personal security equipt.) Up 3.1%, 24 yrs. Hitachi Cable, Japan (wire & cable) Up 1.8%, 26 yrs. Illinois Tool Works (diverse industrial products) Up 3.2%, 20 yrs. Kulicke & Soffa (wafer saws, die bonders, etc.) Up 4.4%, 20 yrs. L.S. Starrett (coordinate measuring machines, tools) Up 1.7%, 35 yrs. Messer Griesheim, Germany (metalworking, other) Up 1.9%, 32 yrs. Rolm & Haas (chemicals) Up 1.8%, 20 yrs. SKF, Sweden (bearings) Up 2.5%, 29 yrs. Thomas & Betts (electric connectors, steel towers) Up 2.5%, 30 yrs. Woolworths, Australia (supermarkets, other retail) Up 2.3%, 20 yrs. Xerox (copiers) Up 2.0%, 40 yrs. Unsung Stars of Lean – A Few Examples Schonberger & Associates As of 10-25-07

The “lean core” (basic Toyota system) and other potent ways to get lean Schonberger & Associates

The Lean Core (Partial List) • Physical resources:Plants-in-a-plant/ cells, kanban/pull system, quick setup, small lots/containers, point-of-use tools/materials/equipment • Human resources:Few job classifications, cross-training/job rotation, operator-based quality and maintenance (TPM) • Supplier partnership:Supplier reduction/ certification, external kanban, dock-to-line deliveries Schonberger & Associates

More Pathways to Leanness • Collaboration in pipelines: 2X to 10X greater lean opportunities • Movement of production: To most capable entities (e.g., contract electronic services) • De-proliferation: Ripple effects of DFMA; reduced numbers of product models, customers, suppliers (via intensive 80-20 analysis at ITW) • Process data: Superior to conventional high-level goals & metrics Schonberger & Associates

Still More Lean Avenues • Pipeline Synchronization/Collaboration:Specialty of Dell, Wal-Mart, Zara (Spain), H&M (Sweden), 7-Eleven • Mining Outside Knowledge/Talent/ Experience:Terex acquisition of Genie • 3D Product Design/Planning: In manufacturing, even more in construction • “Big Idea” Business Models: Such as Dell-direct Schonberger & Associates

Inventory Turnover Danaher: Faded lean star? Fluke: Up 3.2% per year, 18 years Acquired by Danaher Schonberger & Associates

Pipelines/Collaboration: Greatest Lean Opportunities Schonberger & Associates

Lean Inside vs. Lean in the Pipelines • Inside: “Lean core” • Perfected mostly at Toyota in 1960s • Gets 90% of companies’ effort • Easy stuff: You own it, see it, measure it • Pipelines: Tight supply/customer chains • Typical manufacturer: 2X to 10X more opportunity to improve than inside • Much supply-chain talk, little progress • Hard stuff; “hot potato,” no one responsible; phony metrics Schonberger & Associates

Lean Supply-Chain Accounting(Re Inter-Company Inventory/Lead-Time) Problem. In numbers-driven companies inventory accounting often main obstacle to lean supply chains. What to do . . . • Gamesmanship. Recognize accounting-based game—getting inventory on other party’s books—just hides the problem • Impacts. Reveal high cost & non-cost impacts of that hiding • Metric. Employ joint inventory to halt the gamesmanship Schonberger & Associates

Lean efforts in logistics pipelines benefit greatly when piggy-backed upon strong lean achievements inside. That is, lean inside provides an anchor of demand predictability and stability for pursuit of lean outside. Inter-Company LeanBuilding on a “lean core” foundation Schonberger & Associates

Lean Inside Lean Supply ChainExample: Graco, Minneapolis (sprayers, compressors) Phase 1. Became among world’s best in “lean core” Phase 2. Closed many branch warehouses • Benefits (expected): large inventory reductions • Greater benefits (unexpected): • Relying on Graco’s quick response (same-day ship for orders in by noon), distributors slashed their inventories • Frequent orders smoothed/leaned out Graco’s production, purchasing, administration, etc. Schonberger & Associates

Why Does Lean Fade? Are There Antidotes? Schonberger & Associates

Lean’s Soft Underbelly • Many smallish practices; no “Big Idea”:Hard to keep all up-and-running; easy to cherry-pick • Focused on wastes:Doesn’t resonate with sales/marketing, finance, senior execs, owners/investors, the public, customers • Needs rivers of process data:Gets trickling streams • Easily bogged down:In analysis (and popular analysis tools) with over-reliance on projects Schonberger & Associates

Operational Tools (Lean Core) Cells/product-focused units Quick changeover Kanban (queue limitation) Cross-training/job rotation 5S/visual workplace Takt-time scheduling One-piece flow Fail-safing Total productive maintenance Supplier partnership Analysis Tools 6 sigma (statistical analysis) projects Kaizen events Value-stream mapping Spaghetti charts Value-add/non-value-add analysis Popular Lean/6-Sigma Tools Schonberger & Associates

Lean’s Native and Potential Strengths • Native: Simple, common-sense, quick-acting, low cost, all-stakeholder beneficiaries Schonberger & Associates

Tapping Lean’s Full Potential • Re-focus: On universal customer wants/ deliverables: ever better quality, quicker response, greater flexibility, higher value • Data recording: Of every process glitch or hiccup—job of all employees • Workteam-based continuous improvement: In parity with dis-continuous project-team improvement • Look outside your industry: E.g., leading-edge retailers, and 3P distributors • Highest-potential gains: External pipelines Schonberger & Associates

“Big-Idea” Business Models Highly Favorable to Lean • Dell-Direct:Spawned many innovations for synchronization of suppliers, customers, Dell • Every-day low prices (EDLP):In its cause, Wal-Mart became global innovator in logistics, IT • 80-20 in all things: ITW cuts to good customers, suppliers, products, parts, plants, machines . . . • Unique business models(easy to understand, hard to deny, flywheel-like momentum, all-stakeholder beneficiaries): They crown Dell, Wal-Mart, ITW as new, global kings of lean Schonberger & Associates

Inventory Turnover – Dell Inc. 79 5.8%, 17 years Schonberger & Associates

Inventory Turnover Turns Wal-Mart: Up 2.8% per year for 16 years A A Illinois Tool: Up 3.2% per year for 20 years Schonberger & Associates