Download

1 / 15

180 likes | 668 Vues

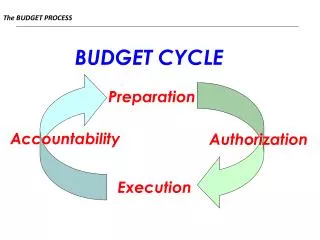

TRANSPARENCY AND ACCOUNTABILTY OF THE BUDGET PROCESS IN ZAMBIA. Presentation at Collaborative Africa Reform Initiative Seminar, 1 st to 3 rd December Pretoria. Contents of the Presentation. This presentation will focus on the following: Budget Classification Prior Reforms ABB Classification

E N D

TRANSPARENCY AND ACCOUNTABILTY OF THE BUDGET PROCESS IN ZAMBIA Presentation at Collaborative Africa Reform Initiative Seminar, 1st to 3rd December Pretoria.

Contents of the Presentation • This presentation will focus on the following: • Budget Classification Prior Reforms • ABB Classification • Improvements associated with ABB classification • Improvements in Budget debates • Political and Stake Holder Involvement in Budget process • Linking Budget implementation through Classification and Chart of Accounts

BUDGET CLASSIFICATION PRIOR TO ABB • Budget structure has been limited to an administrative and broad economic classification. • It lacked functional or programmatic classification and was not linked to policy priorities of government. • The structure hid the detailed activities of the programmes being carried out by the ministries and provinces. • It also followed that the budget presentation was limited to administrative and economic classification and made it difficult for other stakeholders , in particular Members of Parliament (MPs ) and donors, to understand, limiting their decision making.

ABB Classification • Activity Based Budgeting is intended to provide a detailed functional classification as a basis for budget management • Provides the link between resource inputs and specific activities or outputs

Diagramatical Represenation -ABB Policy Framework Strategies & Programmes Output output output output output Activities Activities Activities Input input Input

ABB CONT’D • After piloting for several years (from 1996-t0 2003) GRZ introduced a fully fledged ABB to all MPSAs in the 2004 budget. • It has also been integrated in the funding system and the accounting system.

IMPROVEMENTS ASSOCIATED WITH ABB CLASSIFICATION • Transparency has been achieved • Provided a much more effective framework for translation of policy objectives into the budget instrument • Integration of ABB in the internal control and accounting system has improved the transparency of the budget by highlighting specific activities or functions being carried out by Government including identification of Poverty Reducing Programmes.

IMPROVEMENTS CONT’D • ABB has led to a reduction in misclassification of expenditures that occurred in the old system. (e.g Repatriation and House rentals under the old system were classified as operational cost and not PEs related). • ACCOUNTABILTY • The presentation of the budget in the ABB format has increased the ability of civil society

IMPROVEMENTS CONT’D • In exercising there right to monitor Government policies (operationalised)

IMPROVEMENTS IN BUDGET DEBATES • ABB Classification has led to informative debates and decisions. For example the 2004 budget debate saw a lot of activities cancelled that were said to be misplaced and funds reallocated to the rightful ministries. • Has provided insight for the MPs and other stakeholders on the allocation of resources • Has made the decision making for the MPs simpler.

POLITICAL INVOLVEMENT IN THE BUDGET PROCESS • To make the budget process more transparent, a “green paper” has been introduced for discussions by the Estimates Committee of Parliament, civil society and donors about the broad policy directions Government would pursue. • The “green paper” is published after Cabinet approval of the outcome of the top-down process of preparing the draft macroeconomic and fiscal frameworks and the indicative three-year expenditure ceilings for spending agencies.

STAKEHOLDER INVOLVEMENT • Government also introduced SAGs who were recognized as important stake holder in the budget preparation process. SAGS are simply technical advisory groups constituting stakeholder in various sectors and regions. • At preparation stage these technical groups advise on the sector priority policy actions, programmes and projects and also provide input in the budgetary proposals ( budget framework papers) for the next MTEF period

STAKEHOLDER Cont’d • One of the major roles include: • Review of sector performance and report on implementation and monitoring of PRPs on a quarterly basis ( ABB in place has made it much easier for such monitoring)

Linking Budget implementation through Classification and chart of Accounts • Government has completed a corresponding restructuring of the chart of accounts to that of the ABB. • This has been incorporated in to the computerised Financial Management System. • With such a reform, the accounting reports that are consistent with the budget structure are able to be generated. This is being to monitor budget performance. • With IFMIS (Integrated financial Management Information system) Government hopes to enhance accountability. It is hoped that it will be up and running in 2005.

Conclusion • The improvements in Public expenditure has brought confidence in the cooperating partners. There are moving from specific project support to general budget support. • Stumulate a lot of interest and debate.